Reflation is grinding its way back onto the tape.

Under the surface of a flat S&P print, the composition of today's early tape is unmistakably cyclical. The Dow is up 1.14% while the Nasdaq 100 sits 1.61% lower — a >275bp spread that only opens up when capital is actively rotating out of long-duration growth and into cash-flow-heavy, inflation-sensitive names. Materials (+1.94%), Financials (+1.53%) and Energy (+0.78%) are leading; Consumer Discretionary (-0.82%) is the drag alongside tech. That is the textbook signature of the Rising Growth + Rising Inflation quadrant.

The commodity complex is corroborating: gold +1.08% to 4167.22, silver +1.85% to 62.10, copper +0.79% to 6.22, WTI +0.32% to 68.67. Precious and industrial metals rallying together — while the long end sells off (30Y +0.22% to 4.99, back on the 5-handle intraday high of 5.03) — argues that the marginal buyer is pricing in nominal growth, not deflation. The copper/gold ratio remains structurally depressed at ~0.0015, so this is a nascent shift, not a confirmed regime break. But the ingredients for reflation — weaker dollar bias (DXY 100.82, flat), rising real assets, curve resteepening at the long end — are all in place. Goldilocks is under pressure at the margin; the tape is telegraphing the pivot.

Sector Quadrants

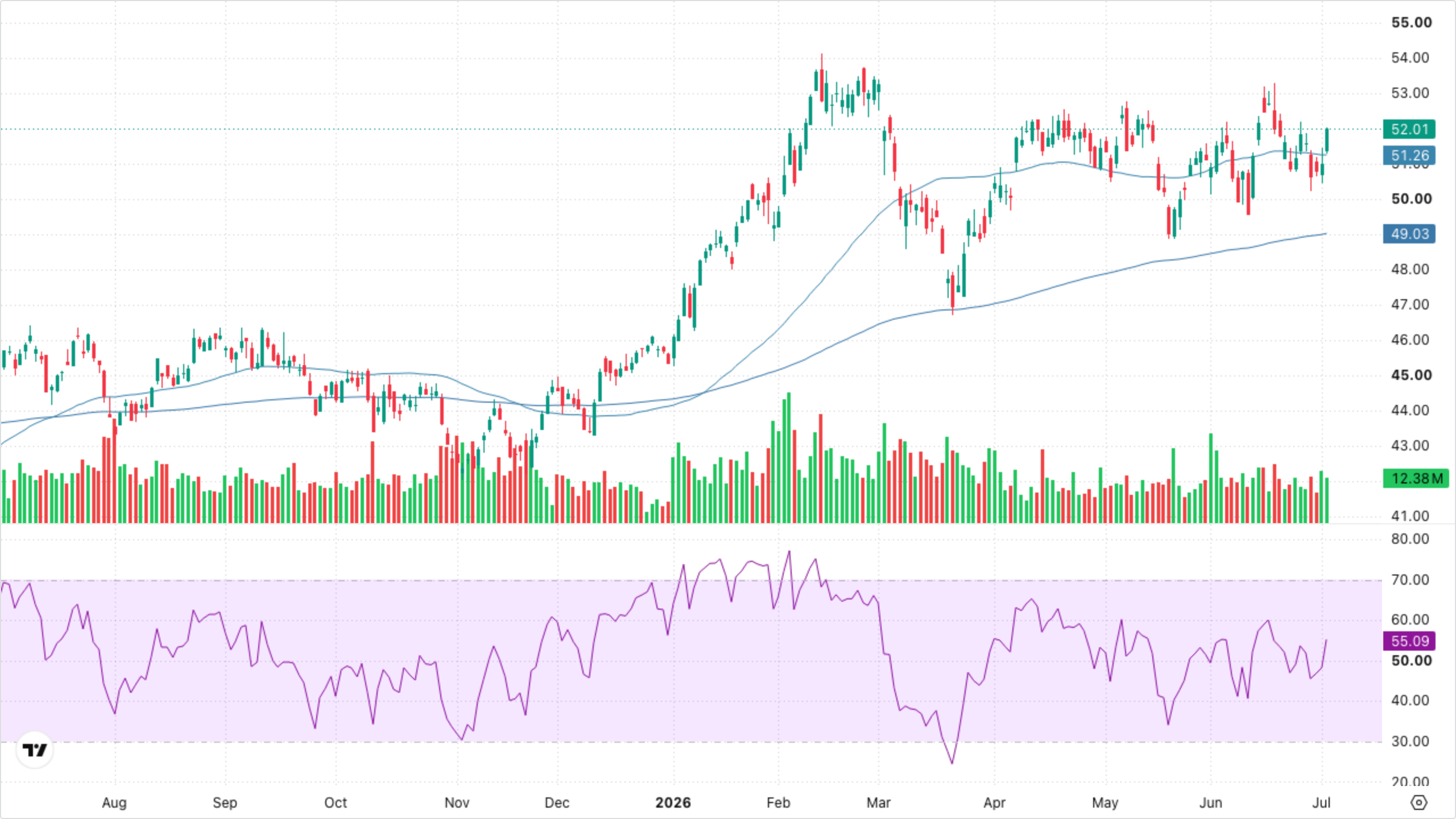

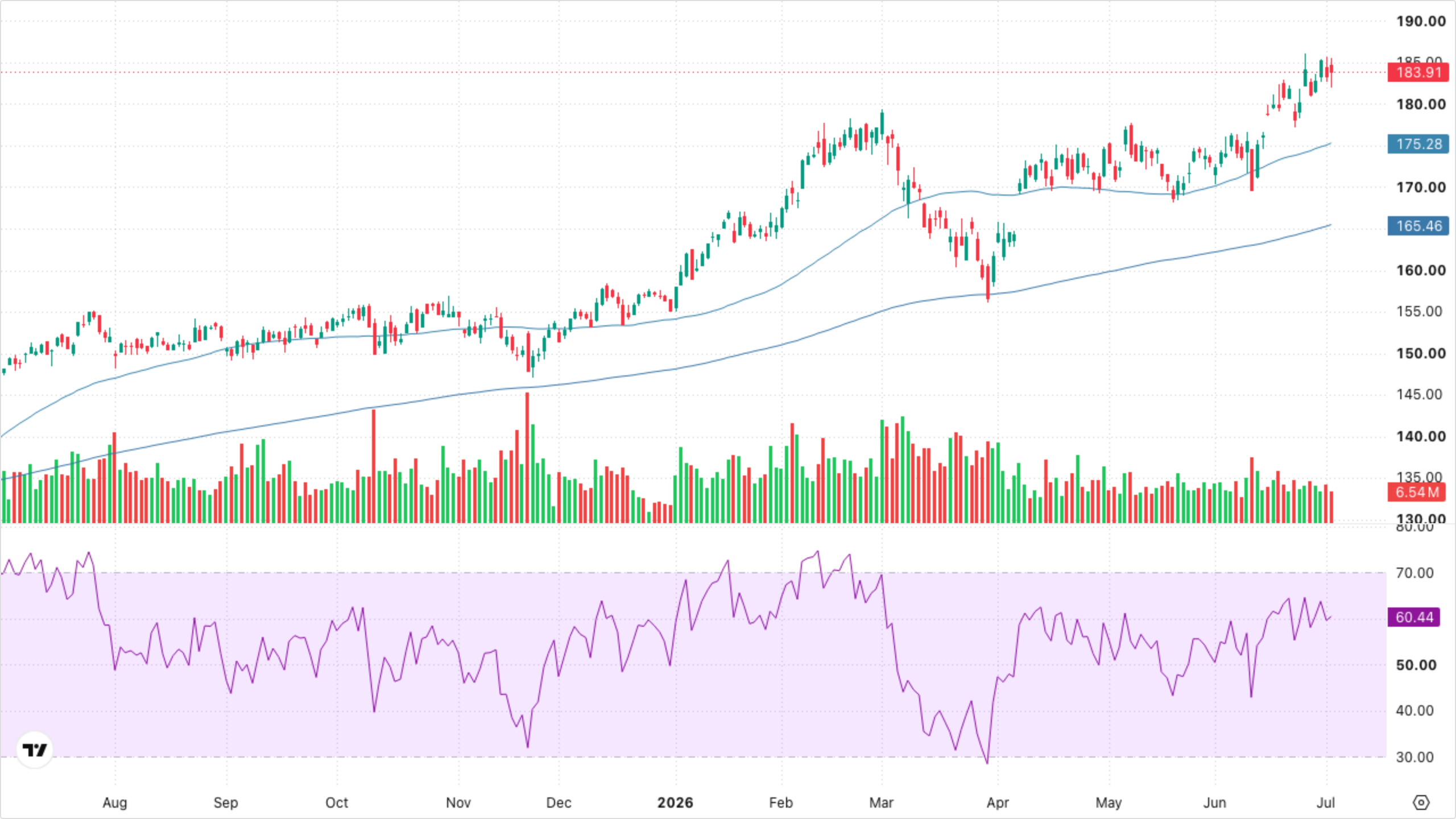

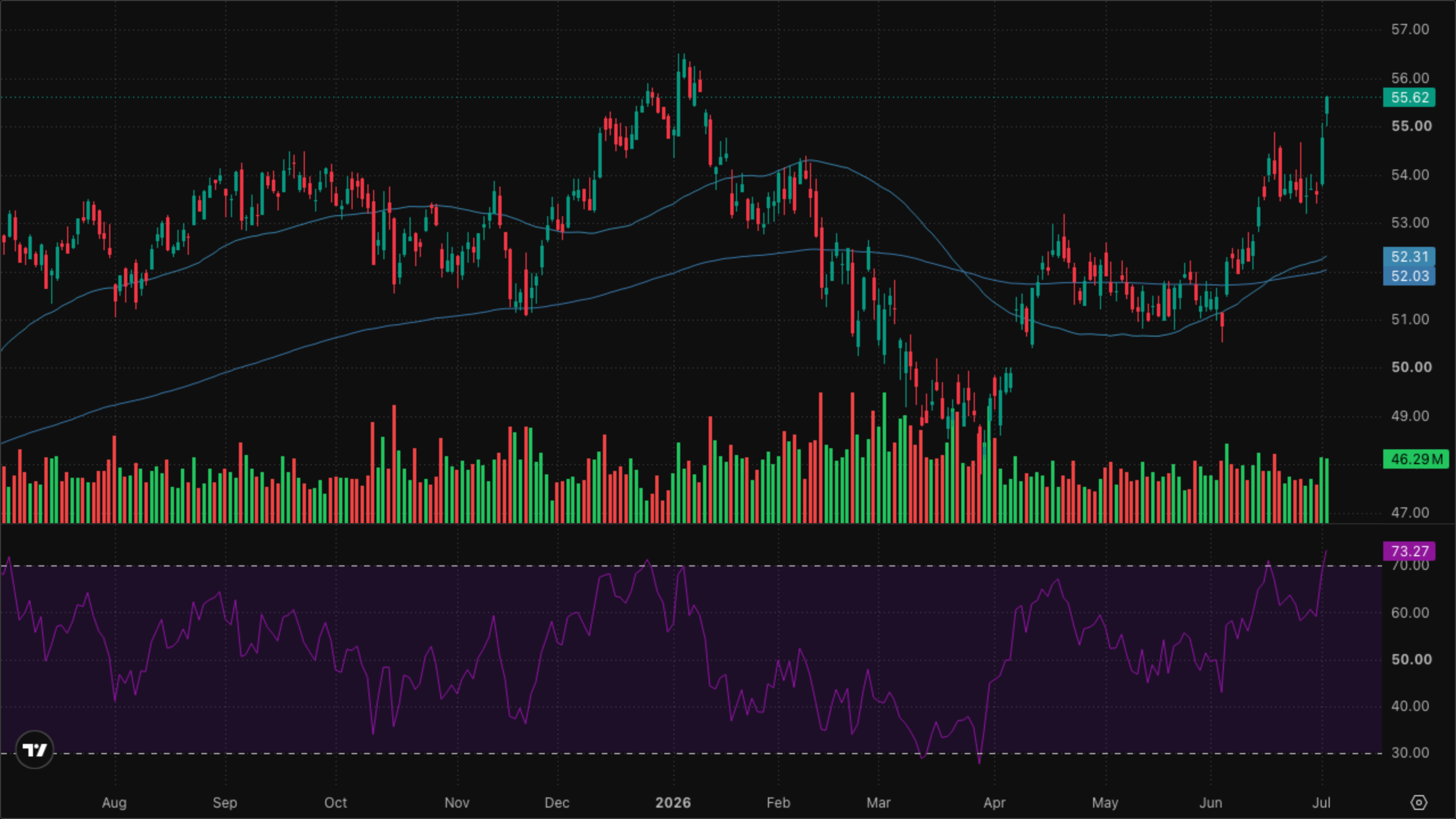

The Reflation quadrant is doing the heavy lifting: XLB (+1.94%) is breaking clean above its SMA 50 with an RSI push toward the mid-60s, XLE (+0.78%) is trying to reclaim its SMA 50 after months of chop, and XLI is consolidating near recent highs. Financials (+1.53%) — the curve-steepener trade — spiked through resistance with a decisive volume candle. The Goldilocks quadrant, especially XLY, is where the outflow is coming from. That's a real regime signal, not noise.

Cross-Asset Narrative

Rates & curve: 10Y at 4.49 is roughly flat but the 30Y (+0.22% to 4.99, session high 5.03) is doing the work — the long end refuses to catch a bid even as tech sells off. That is a classic bear steepener signature and it argues the marginal fixed-income buyer is repricing term-premium/growth-inflation, not recession odds.

Inflation pulse: Gold +1.08% to 4167.22, silver +1.85% to 62.10, copper +0.79% to 6.22, WTI +0.32% to 68.67. Precious, industrial, and energy commodities all bid together is a rare alignment — it's the cleanest reflationary print the tape has offered in weeks.

Risk appetite: VIX -1.43% to 15.91, DXY -0.02% to 100.82. This is not risk-off. Vol is being sold into the rotation, and the dollar is passively lower — both consistent with the market absorbing the growth trade rather than fleeing it.

Equity regime: The Dow/Nasdaq spread of ~275bp is the tell. Value is trouncing growth, cyclicals are trouncing tech, and the S&P's flat print masks a violent internal repositioning.

Global: USD/JPY at 161.24 remains near recent highs — no yen strength to worry about. USD/CNY at 6.78 is a touch softer (-0.13%), consistent with copper's bid.

The weight of evidence points to Rising Growth + Rising Inflation (Reflation).