Today closed the book on the quarter with a textbook growth-plus-disinflation print: the Nasdaq 100 ripped +1.68% to 30,276, the S&P 500 added +0.79% to 7,499, and beneath the surface every defensive corner — Staples -1.54%, Utilities -1.48%, Real Estate -1.98% — was sold. When cyclical growth leaders are bought while bond-proxies are hit and gold, silver, copper and oil-adjacent commodities all soften together, the market is voting for the Goldilocks quadrant, not stagflation and not deflation.

The internals reinforce that read. VIXY fell -1.89% to 21.29, DXY was essentially unchanged at 101.30, and the mega-cap tech complex did the heavy lifting — a classic pattern when the pain trade is "no landing but no re-inflation either." The Dow lagging at just +0.26% while the Nasdaq doubled the S&P's gain tells you this was growth-quality leadership, not a broad reflation impulse. Small caps (Russell 2000 +0.46%) participated but did not lead, which is consistent with a quadrant call that favors quality-growth over deep cyclicals.

The one caveat worth flagging: this reads as a month-end and quarter-end rebalance that leaned hard into what already worked. Fresh confirmation tomorrow — either a follow-through in tech breadth or a bounce in defensives — will decide whether Goldilocks is a durable regime call or a calendar artifact.

TL;DR

💻 Nasdaq 100 led the tape at +1.68% to 30,276.35 as mega-cap growth carried the quarter-end bid.

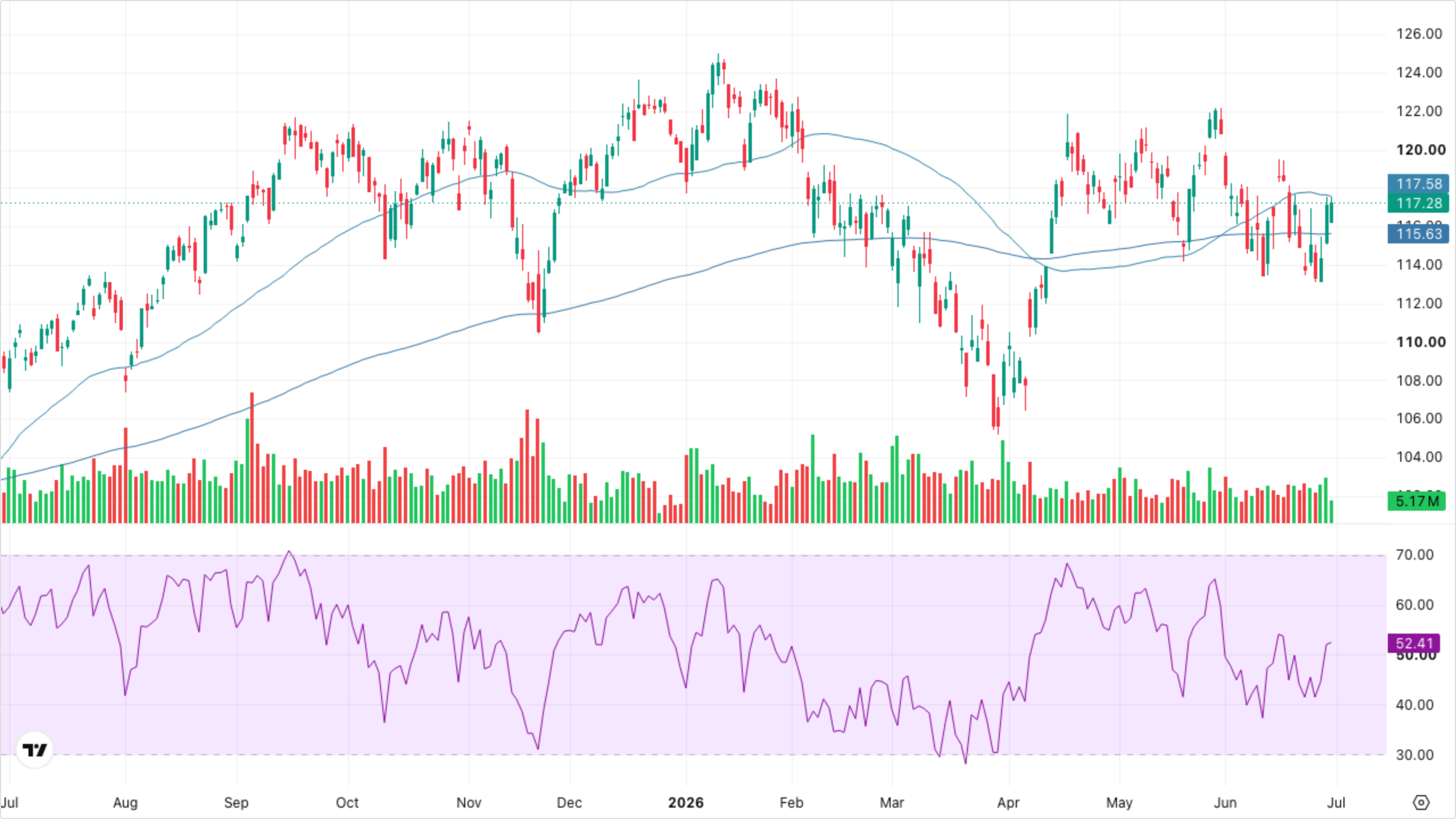

📈 S&P 500 closed at 7,499.35, +0.79%, with an intraday range of 7,438 to 7,508.

🧊 VIXY faded -1.89% to 21.29 — vol suppressed into month-end, no hedging demand into the print.

🛡️ Defensives were the funding source: XLRE -1.98%, XLP -1.54%, XLU -1.48% — bond-proxies unwound.

Trading firmly above both SMA 50 and EMA 200 with the trend intact after the April drawdown fully reversed. RSI in the mid-50s — room to run without being extended.

SPY (S&P 500)

Riding the SMA 50 higher after a sharp reclaim; the moving averages are diverging bullishly with EMA 200 well below price. RSI just under 55 — reset after the recent thrust, not overbought.

QQQ (Nasdaq-100)

Sharpest slope of the four — a near-vertical recovery off the April low with price extending above SMA 50. RSI near 57 leaves room, though the gap between price and EMA 200 is now wide.

VIXY (VIX Short-Term Futures)

Persistent downtrend — price sits well below both moving averages, which are still sloping down. No sign of a hedging bid; the term structure is doing its usual carry-decay job.

Sector Quadrants

Goldilocks — Growth + Disinflation

Risk-on leaders when growth is strong and inflation fades

XLK — Technology

XLY — Discretionary

XLC — Comms

Reflation — Growth + Inflation

Cyclicals that benefit from rising prices and activity

XLE — Energy

XLB — Materials

XLI — Industrials

Stagflation — Contraction + Inflation

Defensives that hold up when growth stalls but prices stay hot

XLP — Staples

XLV — Health Care

XLU — Utilities

Deflation — Contraction + Disinflation

Rate-sensitive sectors that benefit from falling yields

XLRE — Real Estate

XLF — Financials

The Goldilocks quadrant (tech, discretionary, comms) is doing the leading — XLK sits well above its SMA 50 with a healthy but not stretched RSI, consistent with today's Nasdaq-led tape. The Stagflation quadrant is being sold outright (XLP -1.54%, XLU -1.48%) and Deflation-quadrant XLRE was the worst sector at -1.98%, which is unusual given falling commodities — that mix suggests the rates-sensitivity is being overshadowed by a genuine "risk-on rotation out of bond proxies" rather than any change in the yield backdrop. Regime confirmation, not contradiction.

Cross-Asset Narrative

Rates & curve: Live snapshot yields were not populated for this print, so we let the price action speak: bond-proxy sectors (Utilities, Real Estate, Staples) were sold hard, which typically implies either yields drifted higher into the close or investors simply rotated capital toward growth-quality regardless of the curve. Watch the 10Y open tomorrow — if yields are actually lower, then today's XLRE beating is pure sector rotation and even more Goldilocks-flavored than it looks.

Inflation pulse: The commodity complex sagged in unison — gold -0.68% to 3,980.43, silver -1.29% to 57.76, copper -1.63% to 6.15. When precious metals, industrial metals, and (implicitly) inflation hedges all decline while equities rally, the market is pricing softer inflation expectations. This is the "disinflation" half of Goldilocks getting confirmation.

Risk appetite: VIXY down -1.89% to 21.29 with a session low of 20.28 — no one is paying up for downside protection into the new quarter. DXY essentially flat at 101.30 removes any FX-driven headwind for risk assets. The combination is textbook risk-on.

Equity regime: Growth crushed value today. Nasdaq 100 +1.68% vs Dow +0.26% is a 142 bp spread — that's a meaningful growth-over-value rotation, and small caps at +0.46% confirm this isn't a broad reflation; it's specifically a quality-growth bid.

Global: USD/JPY at 162.67 continues to sit near the pain zone; USD/CNY firmed marginally to 6.79. EUR/USD unchanged near 1.14. No FX flashpoints tonight.

The weight of evidence points to Goldilocks — growth with fading inflation.

What to Watch

📊 ISM Manufacturing PMI (tomorrow AM) — if the print holds above 50 with softer prices-paid, Goldilocks strengthens; a sub-50 read with sticky prices flips the call toward stagflation.

📉 10Y Treasury open — if yields drift lower alongside today's equity rip, that's the cleanest possible Goldilocks confirmation. Yields spiking above their recent range while equities hold would raise a "reflation, not disinflation" flag.

🧊 VIX behavior on the first day of the new quarter — if VIXY holds below 22 with no hedging bid, complacency compounds; a sudden spike above 24 with equities still up would suggest tail-risk positioning ahead of a known catalyst.

🏦 Any Fed speakers — commentary that leans dovish on prices while acknowledging resilient growth reinforces the quadrant. Any hawkish "we need to keep policy tight because activity is too hot" language is what unwinds the trade.

🛡️ Defensives bounce or continued sell? — if XLU, XLP, XLRE stabilize tomorrow, today was a rebalance shakeout. If they keep bleeding, the rotation out of bond-proxies is durable and Goldilocks has legs into July.