The day's tape was a textbook Quadrant 2 print: mega-cap tech and discretionary ripped, defensives and inflation hedges bled, and the VIX got taken out behind the woodshed. XLK +2.37% and XLY +2.40% led the SPX to a +1.18% close at 7440.44, while the Nasdaq 100 outperformed by a full 100bp at +2.25%. Gold cratered -1.47% to 3956.64, silver dropped -1.88%, and materials gave back -1.82% — the exact rotation profile of risk seekers reaching for duration and growth at the expense of the inflation trade.

The wart on this otherwise clean Goldilocks print is the Russell 2000 closed effectively flat at +0.01%, refusing to join the party. Small caps not confirming a tech-led rally is a familiar 2025–26 pattern, but it's worth flagging: this remains a narrow regime expression, not a broad cyclical expansion. Yields barely moved (10Y at 4.37%, -0.4bp), so the bid for growth was not a duration-rally story — it was risk appetite returning after the prior session's defensive crouch. Quadrant call holds, with a footnote that breadth still needs to confirm.

TL;DR

📈 Nasdaq 100 +2.25% to 29,774.75 — mega-cap tech reasserts leadership; SPY +1.65% to 741.00.

🧊 VIX -4.02% to 17.66, VIXY -4.07% — risk shake-out reversed in a single session.

🪙 Gold -1.47% to 3,956.64 and silver -1.88% — precious metals unwind the safety bid.

⚒️ Materials -1.82% the worst sector; energy -0.48% as crude went nowhere (+0.01%).

🦗 Russell 2000 +0.01% — small caps refuse to confirm the tech rip.

Since Last Update

No prior session block was appended; the deltas above reference today's intraday change from the snapshot.

Watchlist

Economic Calendar

Market News

Charts

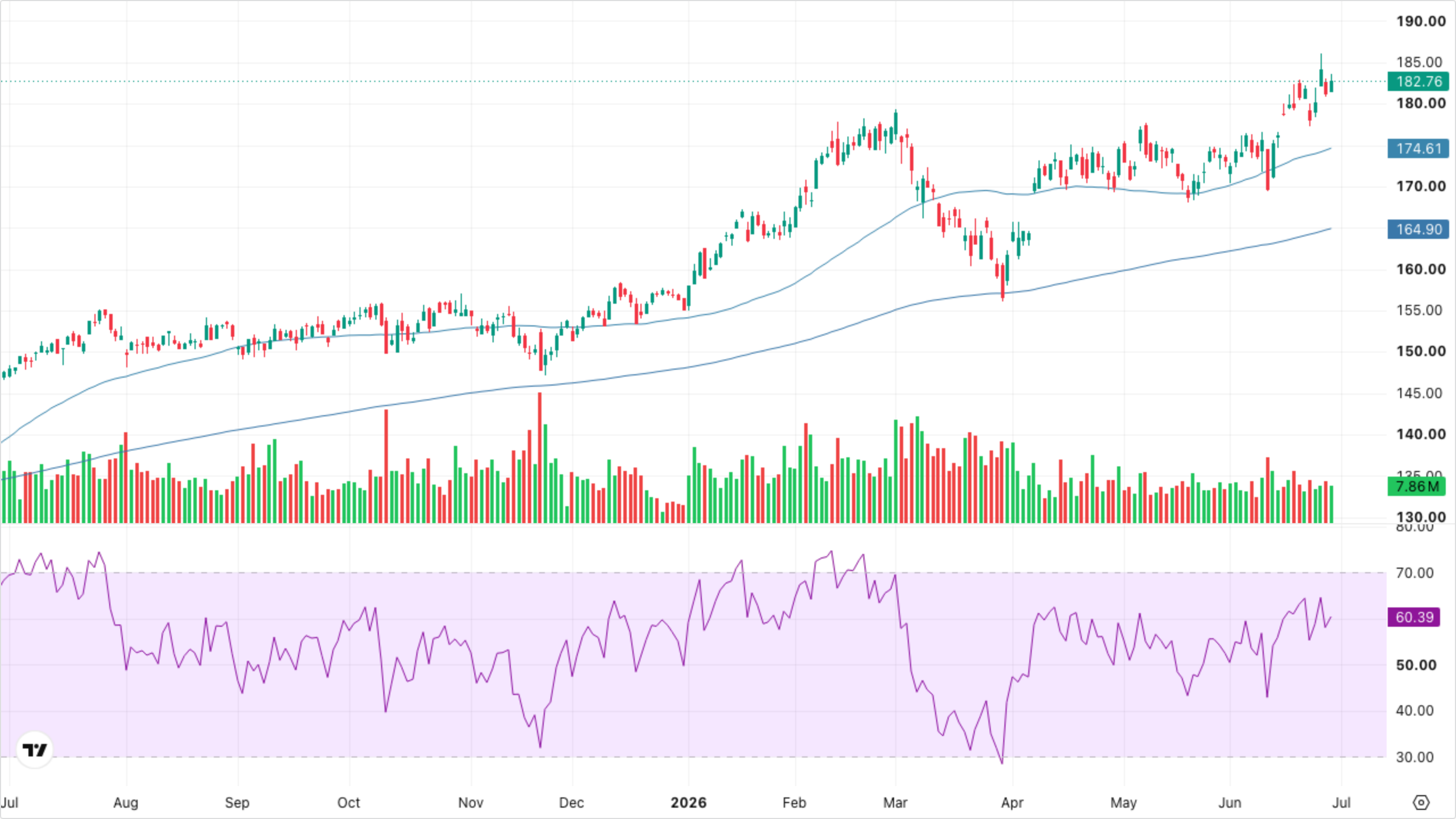

VT (Global Equity)

Holding above the rising SMA 50 with EMA 200 sloping up underneath; today's bounce arrested a two-week pullback. RSI rebounded off the midline near 52 — neutral, with room to extend.

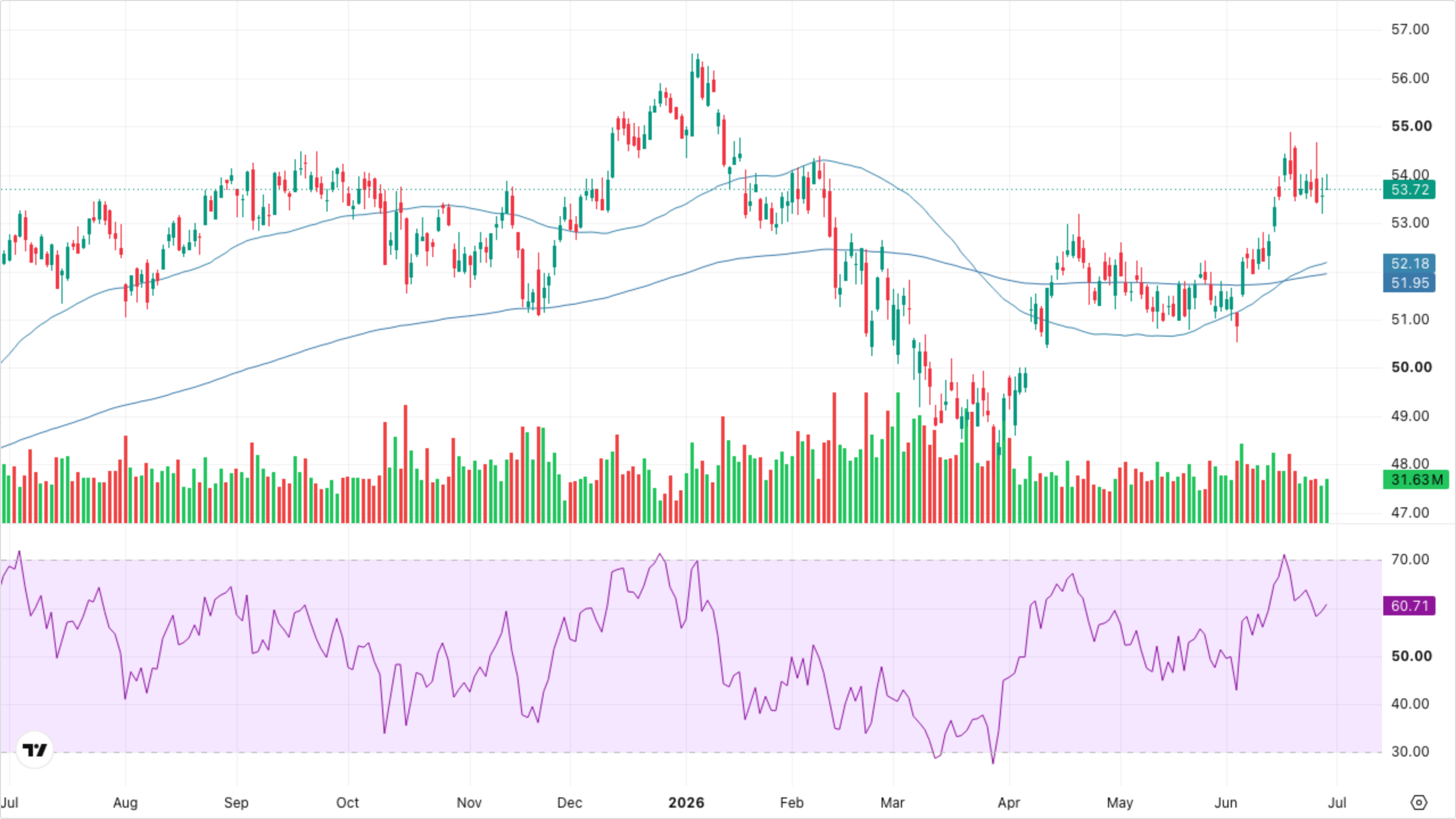

SPY (S&P 500)

Sharp reclaim of the SMA 50 after testing it on the prior session; trend structure (price > SMA 50 > EMA 200, both rising) intact. RSI back above 50 on expanding volume — bullish confirmation.

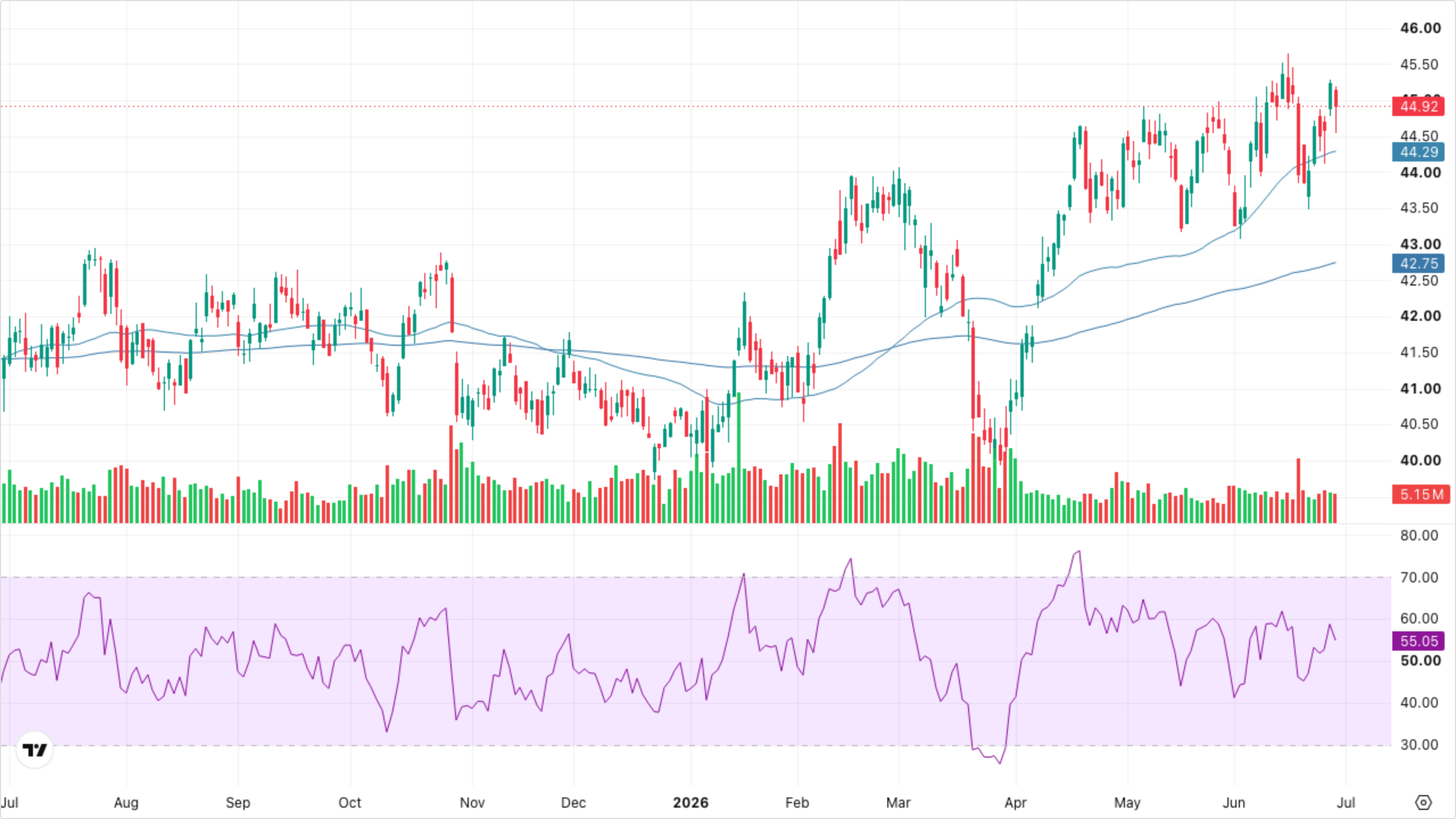

QQQ (Nasdaq-100)

Even stronger reversal than SPY — outsized green candle on heavy volume reclaiming the SMA 50 cleanly. Leadership concentration is back; the slope of the EMA 200 remains decisively positive.

VIXY (VIX Short-Term Futures)

Downtrend resumes after a brief spike attempt — VIXY remains pinned below both moving averages, which are still sloping down. Vol regime continues to compress.

Sector Quadrants

Goldilocks — Growth + Disinflation

Risk-on leaders when growth is strong and inflation fades

XLK — Technology

XLY — Discretionary

XLC — Comms

Reflation — Growth + Inflation

Cyclicals that benefit from rising prices and activity

XLE — Energy

XLB — Materials

XLI — Industrials

Stagflation — Contraction + Inflation

Defensives that hold up when growth stalls but prices stay hot

XLP — Staples

XLV — Health Care

XLU — Utilities

Deflation — Contraction + Disinflation

Rate-sensitive sectors that benefit from falling yields

XLRE — Real Estate

XLF — Financials

The Goldilocks quadrant is doing all the work today — XLK and XLY each up ~2.4%, with XLC adding +1.60%. Reflation is mixed but skewed bearish (XLB -1.82%, XLE -0.48%, only XLI green at +0.86%), and the stagflation defensives (XLP, XLV, XLU all red) are exactly the funding source you'd expect when the market is leaning hard into growth. The contradictory note is XLRE -0.71% despite flat yields — a duration name slipping on a low-vol risk-on day suggests rotation is the dominant force, not rate signals.

Cross-Asset Narrative

Rates & curve: Essentially unchanged. 2Y 4.10%, 10Y 4.37%, 30Y 4.86% all flat on the day, with 2s10s holding at +27bp. The curve gave equities permission to rally without contributing a tailwind — neither a duration unwind nor a flight-to-safety bid. That's the cleanest possible backdrop for risk to dictate.

Inflation pulse: The day's most decisive signal. Gold -1.47%, silver -1.88%, copper -0.28%, with WTI flat (+0.01%). When equities rip and precious metals get hit while crude does nothing, the market is pricing less inflation risk and more real growth. That's a textbook Goldilocks data point.

Risk appetite: VIX -4.02% to 17.66 is a meaningful re-entry into the low-vol regime; DXY +0.16% to 101.28 firmer but contained. No flight-to-safety here — the dollar is mildly bid on what looks like rate-spread mechanics, not stress.

Equity regime: Large-cap growth dominated; small caps stalled (R2K flat). XLK/XLY +2.4% vs XLB -1.82% is a textbook growth-over-value rotation. The IWM non-confirmation is the only meaningful crack in an otherwise pristine Goldilocks tape.

Global: USD/JPY +0.11% to 162.11, EUR/USD -0.16%, USD/CNY -0.06% — quiet. No new yen-stress impulse; PBoC fixing range steady.

The weight of evidence points to Goldilocks (Quadrant 2).

What to Watch

📊 If Tuesday's ISM Manufacturing prints > 50 with cooling prices-paid, Goldilocks gets a fundamental confirmation; a hot prices-paid sub-index would re-open the reflation trade.

🦗 If IWM finally joins the rally and clears recent range highs, breadth confirms the regime; another non-participation day says this is still a narrow mega-cap story.

🪙 If gold loses 3,900 support, the safety bid is truly broken — bullish for Quadrant 2 risk; a sharp reversal back over 4,000 would suggest today's selloff was just position-trimming, not regime change.

🏦 If 10Y breaks below 4.30%, duration tailwind kicks in for XLRE/XLU; a break above 4.45% on no new data would re-introduce a valuation headwind for the tech leadership.

🌡️ If VIX takes out 16 handle, the vol regime fully resets and dealer gamma turns suppressive — supportive of further melt-up; a snap back over 20 would invalidate today's risk-on print.