Charts

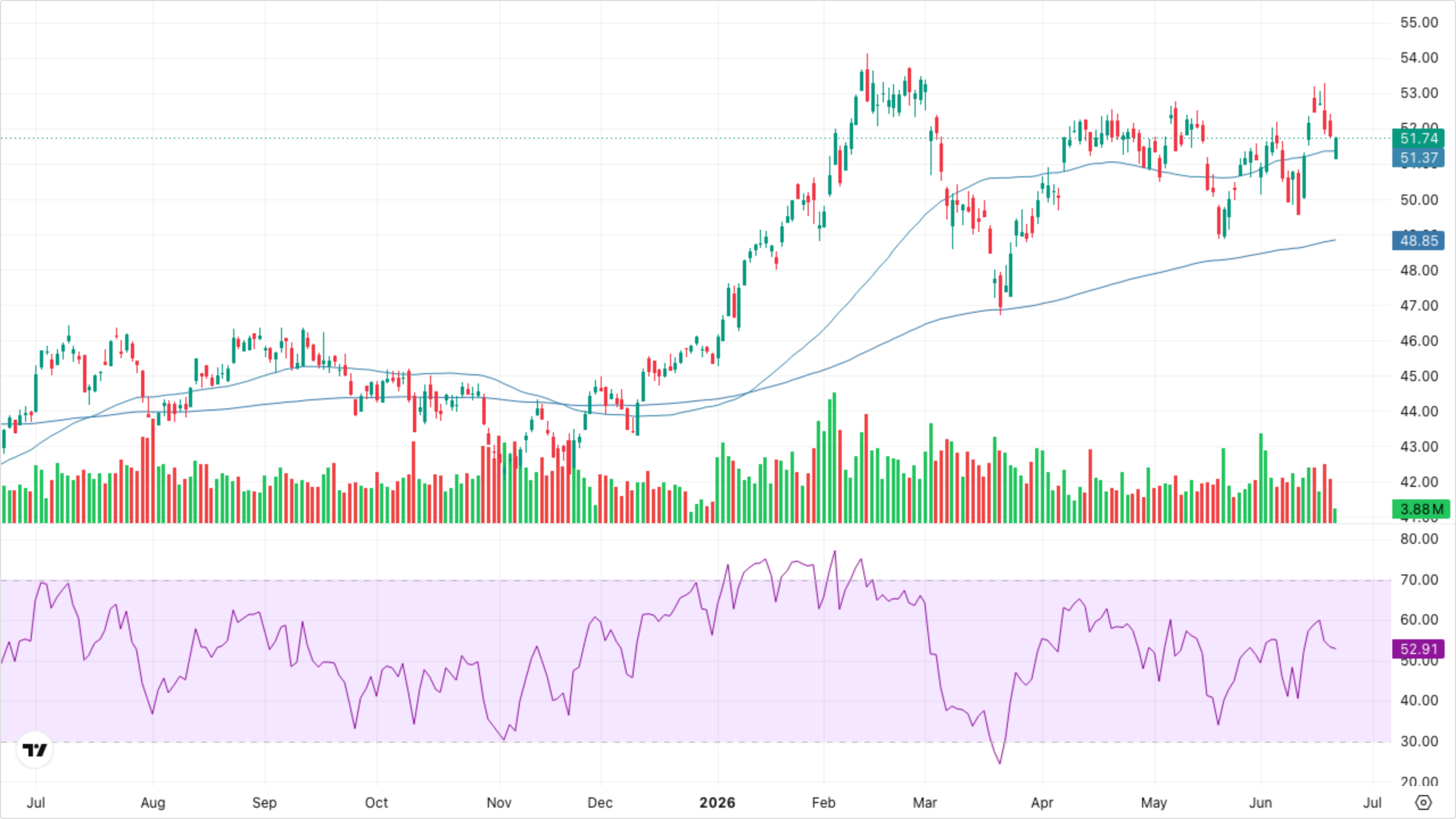

VT (Global Equity)

Trading above SMA 50 and well above the rising EMA 200, uptrend intact. RSI rolled from overbought back to the mid-50s — a healthy reset rather than a break.

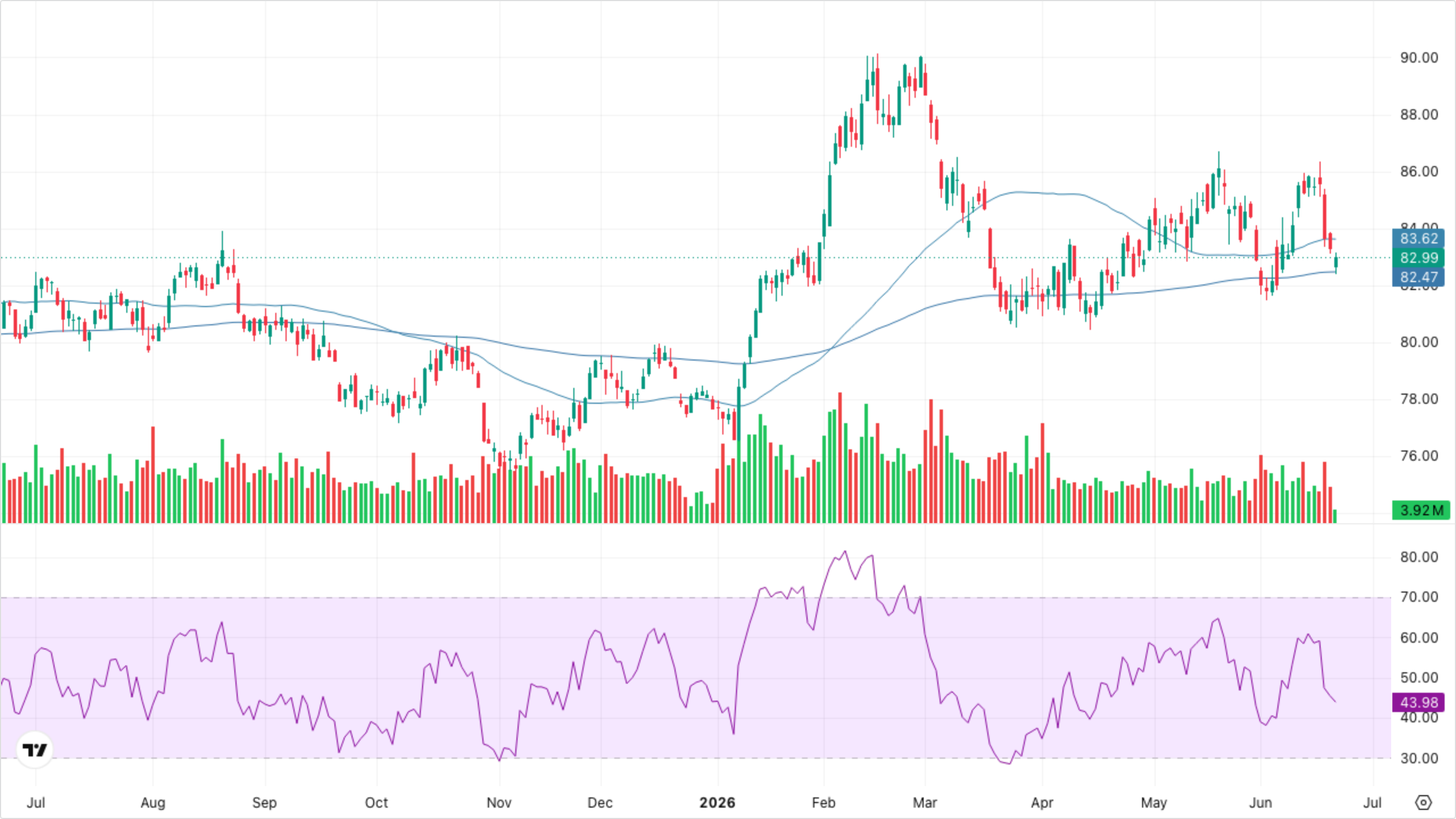

SPY (S&P 500)

Price perched just below recent highs and still above SMA 50; the EMA 200 sits well underneath. RSI cooling from overbought into the low-50s on declining volume — pause, not reversal.

QQQ (Nasdaq-100)

Held the breakout zone after a hot run; SMA 50 climbing fast below price. RSI fading from the high-60s — first sign of momentum giving back after the May–June surge.

VIXY (VIX Short-Term Futures)

Still tracking a multi-month downtrend, price below both moving averages. The recent April spike is well behind; the spot VIX bid hasn't yet shown up in the futures product.