Charts

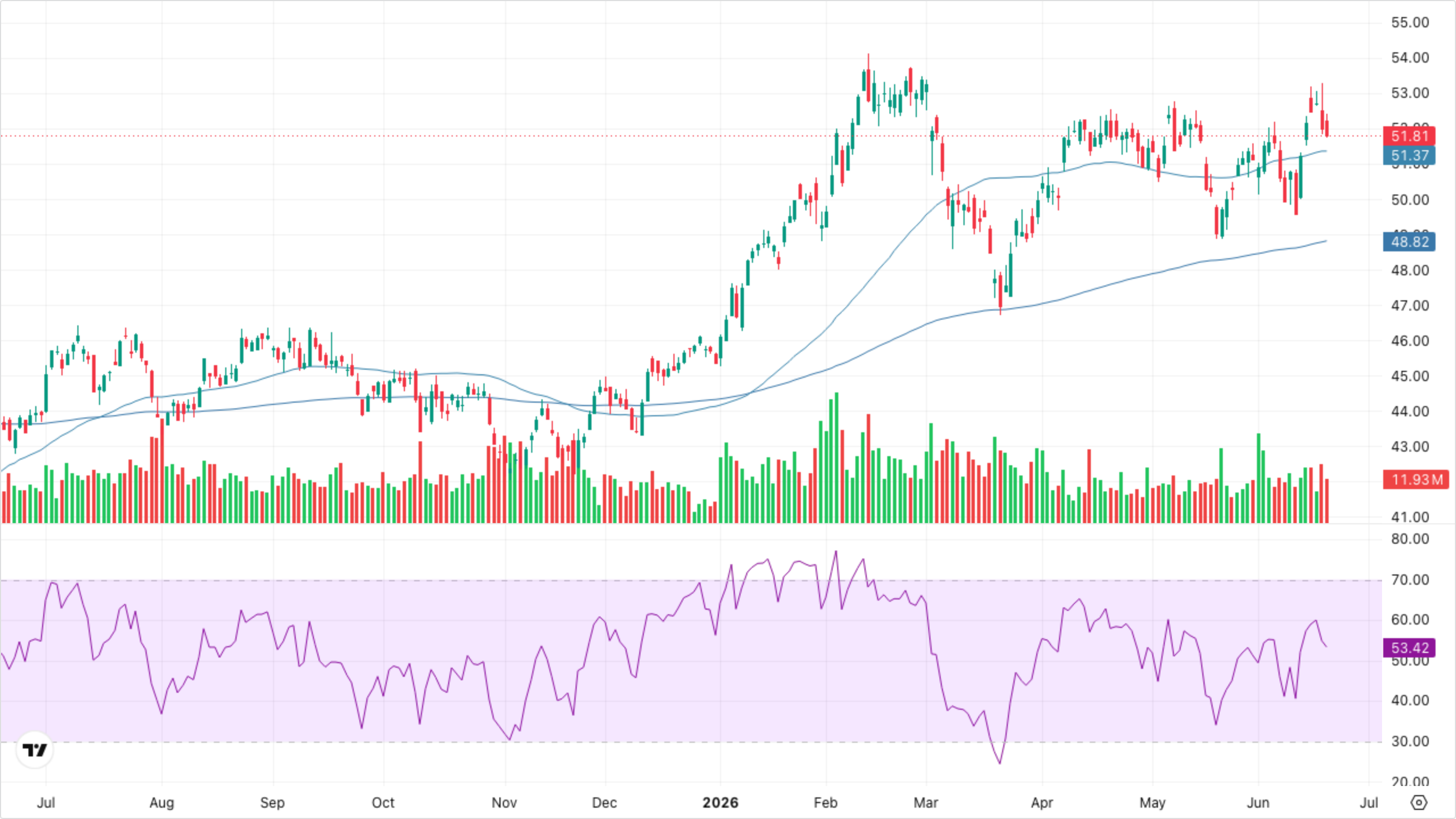

VT (Global Equity)

Trading at the upper band of the recent range, well above both SMA 50 and EMA 200, with RSI mid-50s — uptrend intact but momentum more contained than the US-only indices.

SPY (S&P 500)

Pushing back toward the cycle high after a quick reset; price holding above SMA 50 with the 50/200 spread widening. RSI in the mid-50s leaves room before overbought — volume on today's bar is the heaviest in weeks.

QQQ (Nasdaq-100)

Strongest of the bunch — sharp expansion bar with the 50-day curling up, RSI pushing back into the upper 50s. Volume is expanding into the breakout attempt, a constructive signal.

VIXY (VIX Short-Term Futures)

Carving fresh cycle lows below both SMA 50 and EMA 200; the downtrend in implied vol carry remains the dominant signal even as spot VIX flickers higher intraday.