Reflation with stagflation undertones — commodities lead, defensives bid.

The tape is sending a layered message into the open. Equity indices are essentially flat at record territory (SPX 7602.04, +0.03%), but underneath the surface the rotation tells a different story. Industrial metals are ripping — copper +1.88%, silver +1.07%, gold +0.33% to $4499.58 — while WTI crude trades $91.84 with Iran tensions keeping the bid alive. That commodity complex is the textbook signature of a reflationary impulse.

But the defensive bid is just as loud. Utilities (XLU) lead all sectors at +1.04%, staples are mixed, and Communications (-1.26%) and Healthcare (-1.09%) are the standout laggards — an odd pairing that suggests positioning rather than pure macro. The 10Y at 4.45% with the 2s10s at +41bp says the curve isn't pricing recession, but it's not pricing easy disinflation either. The dollar at 99.14 is on the back foot, which is fueling the commodity story.

Net read: growth is holding (Russell 2000 +0.53% pre-open is the cleanest cyclical tell), but the inflation impulse from oil and metals is the dominant signal. This is closer to the Rising Growth + Rising Inflation quadrant than Goldilocks, with stagflation as the risk case if growth data wobbles.

TL;DR

📈 Records held overnight — SPX 7602.04 (+0.03%), NDX 30576.64 (+0.21%), Russell 2000 +0.53% leads small caps.

🛢️ Oil sticky at $91.84 WTI, modest -0.67% pullback but holding the Iran-risk premium.

💵 Dollar soft — DXY 99.14 (-0.04%), USD/JPY 159.86 keeps the carry trade alive.

🏥 Defensive split — Utilities +1.04% lead, but Healthcare -1.09% and Comms -1.26% are notable drags.

Watchlist

Economic Calendar

Watch list for today (US): ISM Services PMI and the JOLTS Job Openings release are the headline data points. Both feed directly into the regime question — a hot Services print would reinforce the reflation read, while a JOLTS miss would re-introduce the stagflation risk by signaling softening labor demand alongside sticky goods inflation. Fed speaker calendar is light; the next FOMC decision is June 16–17 under new Chair Kevin Warsh, with markets pricing roughly a 65% probability of a hold.

Market News

Charts

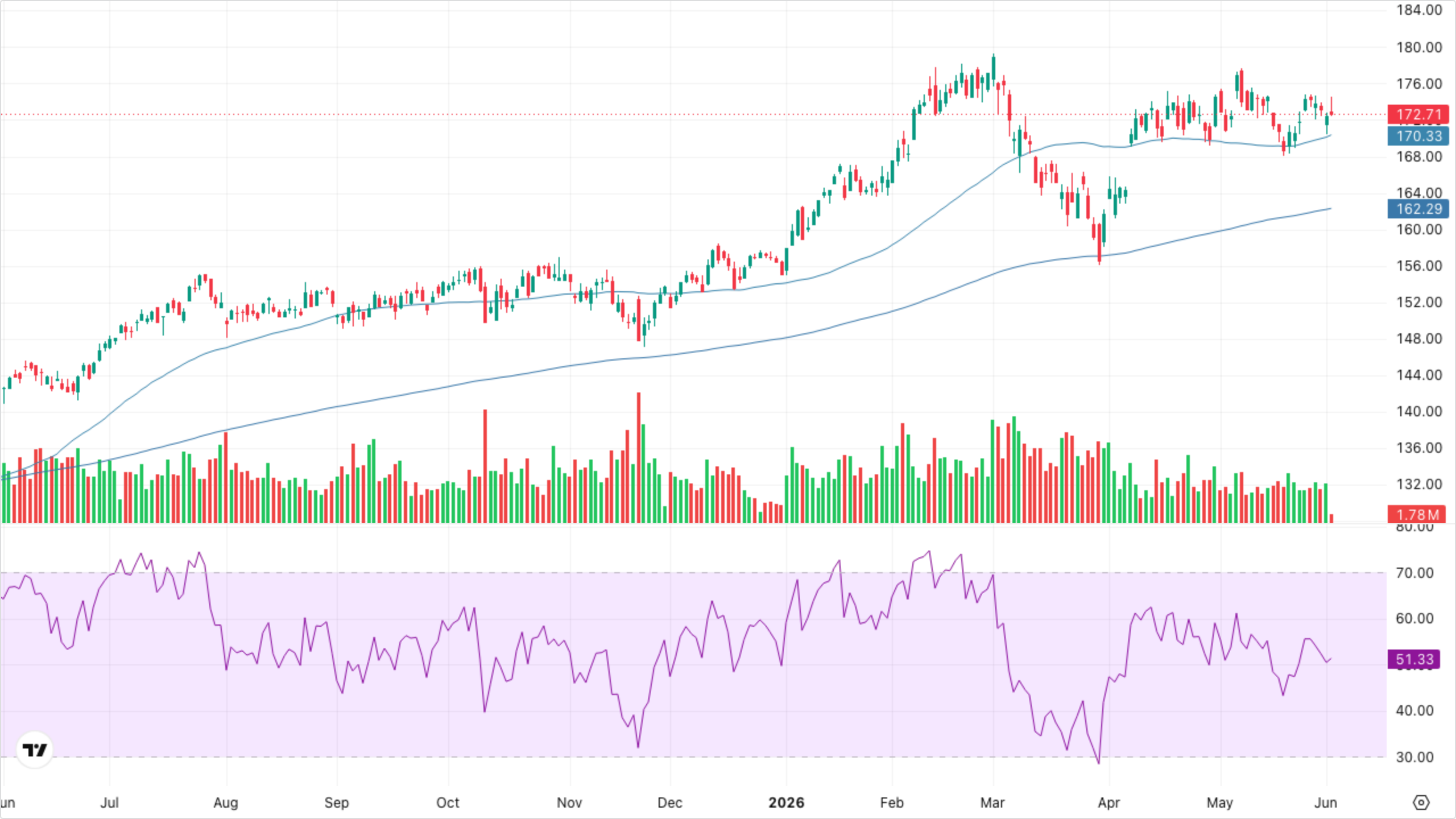

VT (Global Equity)

Sharp recovery from April lows has resumed the primary uptrend — VT is now well clear of both SMA 50 and EMA 200, with the moving averages widening to the upside. RSI in the upper-60s is firm but not yet stretched.

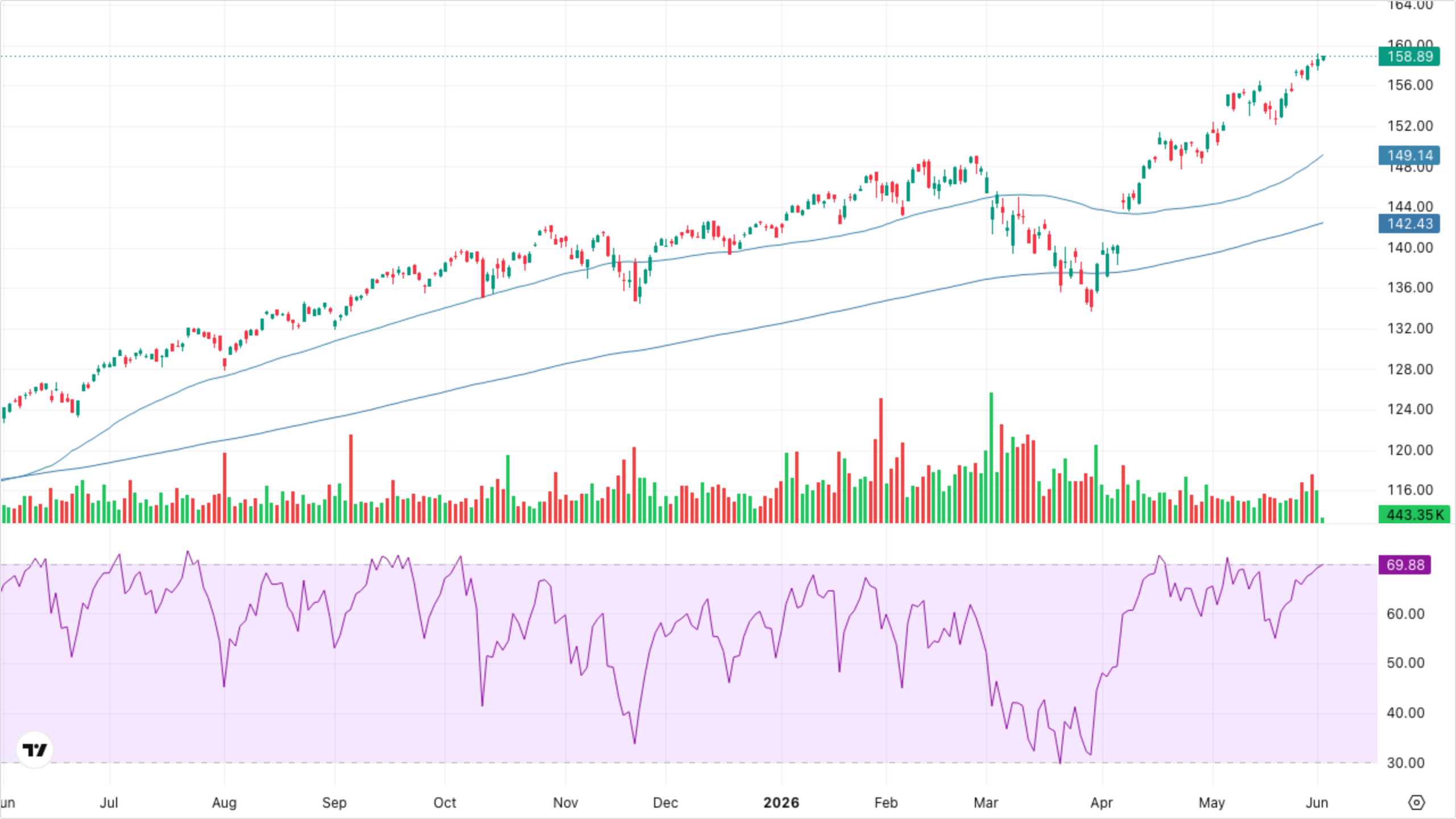

SPY (S&P 500)

Vertical rally off the April low has pushed SPY to fresh highs, sitting cleanly above SMA 50 and EMA 200. RSI is the watch item — pushing into the mid-70s flags overbought conditions; any pullback that resets RSI without breaking the SMA 50 would be constructive.

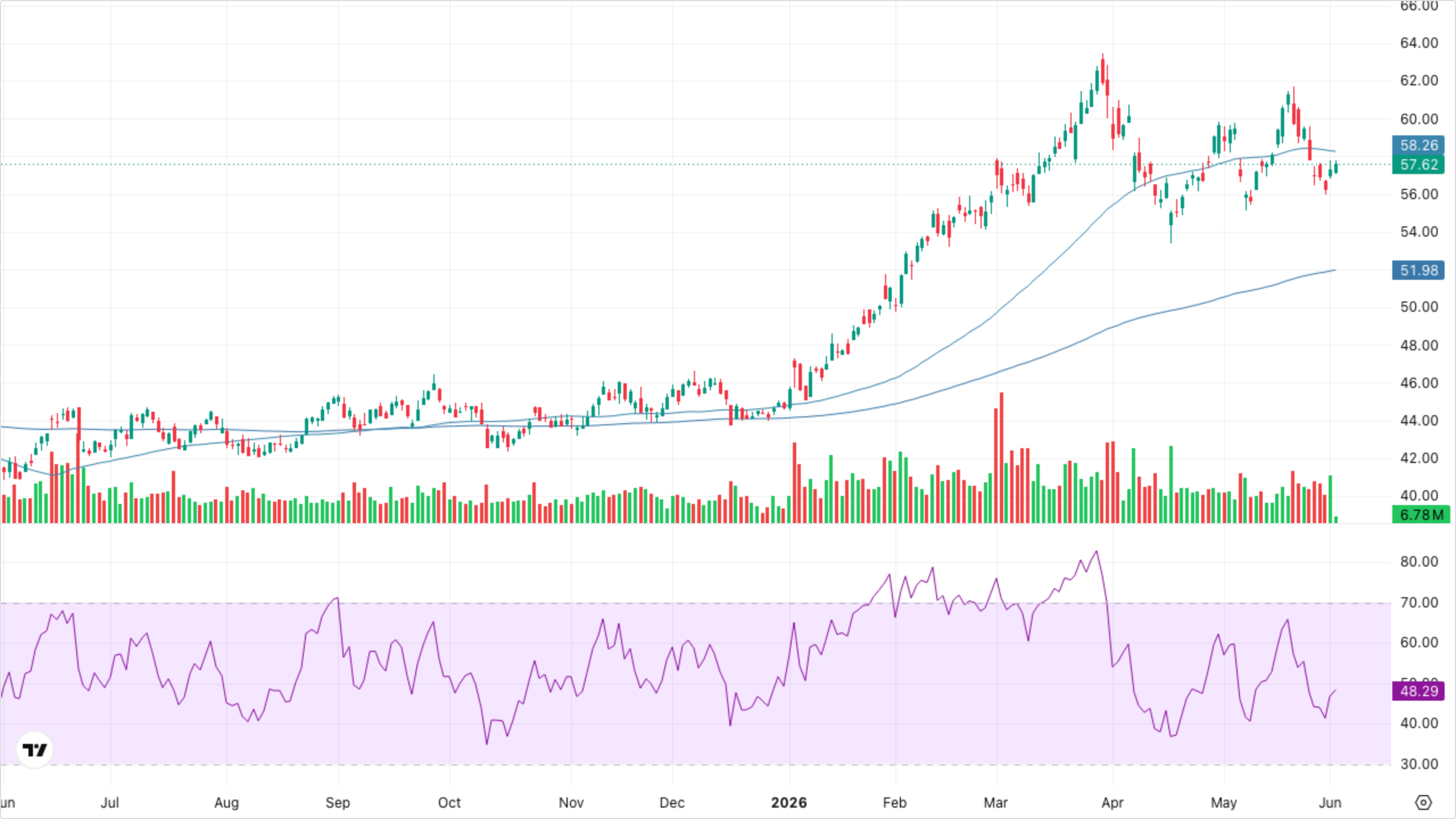

QQQ (Nasdaq-100)

QQQ leads SPY on the recovery — the gap above SMA 50 is wider, confirming tech leadership in the move. RSI near 79 is the most overbought signal on the dashboard; volume has been contracting on the latest leg, a minor non-confirmation worth watching.

VIXY (VIX Short-Term Futures)

VIXY remains in a clean downtrend, pressing fresh local lows below both moving averages — the contango drag continues to grind shorts. No bullish divergence yet; complacency in vol is the dominant signal.

Sector Quadrants

Goldilocks — Growth + Disinflation

Risk-on leaders when growth is strong and inflation fades

XLK — Technology

XLY — Discretionary

XLC — Comms

Reflation — Growth + Inflation

Cyclicals that benefit from rising prices and activity

XLE — Energy

XLB — Materials

XLI — Industrials

Stagflation — Contraction + Inflation

Defensives that hold up when growth stalls but prices stay hot

XLP — Staples

XLV — Health Care

XLU — Utilities

Deflation — Contraction + Disinflation

Rate-sensitive sectors that benefit from falling yields

XLRE — Real Estate

XLF — Financials

Reflation quadrant is doing the heaviest lifting this morning — XLE +0.58%, XLB +0.55%, XLI +0.61%, all consistent with the copper/silver bid. Utilities (+1.04%) crossing over from the stagflation bucket is the cleanest tell of dual demand: investors want both inflation hedges and duration-defensive exposure. Goldilocks is split — XLK +0.49% holds the tape up, but XLY -0.51% and XLC -1.26% are dragging. Net read: leadership is shifting away from pure growth toward cyclicals + defensives, which confirms the reflation-with-stagflation-undertones regime call.

Cross-Asset Narrative

Rates & Curve: The 2s10s spread sits at +41bp (10Y 4.45%, 2Y 4.04%) — modest steepening territory, with the long end holding firm despite the soft 30Y (-0.18%). The curve is not pricing imminent cuts; with the next FOMC June 16–17 under new Chair Warsh and a 65% hold probability, the front end is anchored. Yields aren't the story this morning.

Inflation pulse: Loud. Silver +1.07%, copper +1.88%, gold $4499.58 — that's a coordinated industrial-and-monetary metals bid. Crude $91.84 holding the Iran premium adds the energy leg. This is the inflation signal of the day, and it's the cleanest reflation tell on the board.

Risk appetite: VIX 16.05 (-0.06%), VIXY -0.84% — vol complacency intact. DXY 99.14 weak. No flight-to-safety in the volatility complex, but the gold bid suggests some hedging continues alongside risk-on.

Equity regime: Russell 2000 +0.53% leading the majors is the clearest tell — small caps outperforming on a flat-tape session is a classic reflation footprint. Within sectors, the rotation is from Comms/Discretionary into Industrials/Materials/Utilities.

Global: USD/JPY 159.86 — the carry trade remains intact, no BoJ-driven stress. EUR/USD 1.16, modest USD weakness. Asia/Europe behavior is being driven by the same Iran-tension / commodity-bid axis as the US tape.

The weight of evidence points to Rising Growth + Rising Inflation (Reflation), with stagflation as the risk case if today's ISM Services or JOLTS print soft.

What to Watch

📊 If ISM Services PMI prints above consensus then reflation thesis confirms — strong services activity alongside hot commodities cements the rising-growth, rising-inflation quadrant call.

💼 If JOLTS Job Openings miss materially then stagflation risk re-emerges — softening labor demand alongside oil $91+ flips the regime read toward the stagflation risk case.

🛢️ If WTI breaks above $93 on Iran escalation then the inflation leg dominates — energy sector outperformance accelerates, breakevens widen, and the 10Y likely tests 4.50%.

📉 If 10Y yield breaks above 4.50% then duration-sensitive names roll over — watch XLRE, XLU, and long-duration tech; a yield-led correction would be the first crack in the tape.

⚡ If VIX breaks above 18 on an intraday spike then the risk-on regime is under threat — current 16.05 reading is complacent; a quick re-rate would force de-risking into the FOMC window.