Goldilocks holds, with a reflation tilt.

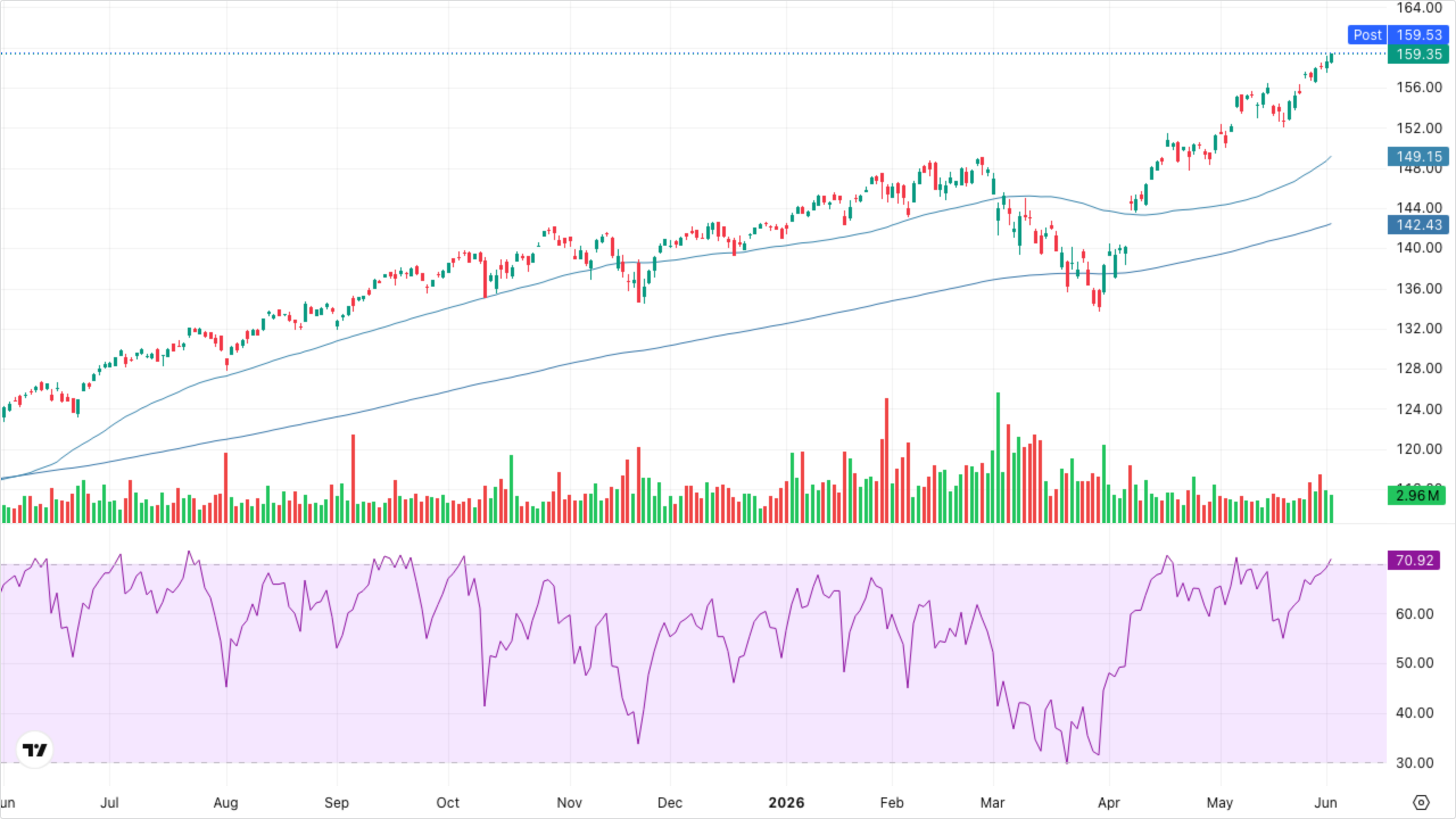

The S&P 500 punched through 7,600 for the first time ever while the Russell 2000 led the tape +0.90% — a breadth signature consistent with growth-on, not late-cycle defense. Yields stayed pinned (10Y unchanged at 4.45%, near three-week lows) even as WTI pushed to $94.20 on Iran headlines. That combination — stable rates, firm equities, small-cap leadership, cyclicals (XLE, XLB, XLI) bid alongside tech — keeps the Goldilocks call intact, though the energy/materials strength is adding a reflation flavor that bears watching if oil continues to trend.

Cross-Asset Narrative

Rates & Curve

10Y yield unchanged at 4.45% (intraday range 4.42–4.46), 30Y -1bp to 4.96%. With WTI bid on Iran headlines, bonds shrugging is the tell — the market is pricing this as a geopolitical risk premium, not a durable inflation impulse. Yields sitting near three-week lows keeps the discount-rate tailwind intact for duration-sensitive equity.

Inflation Pulse

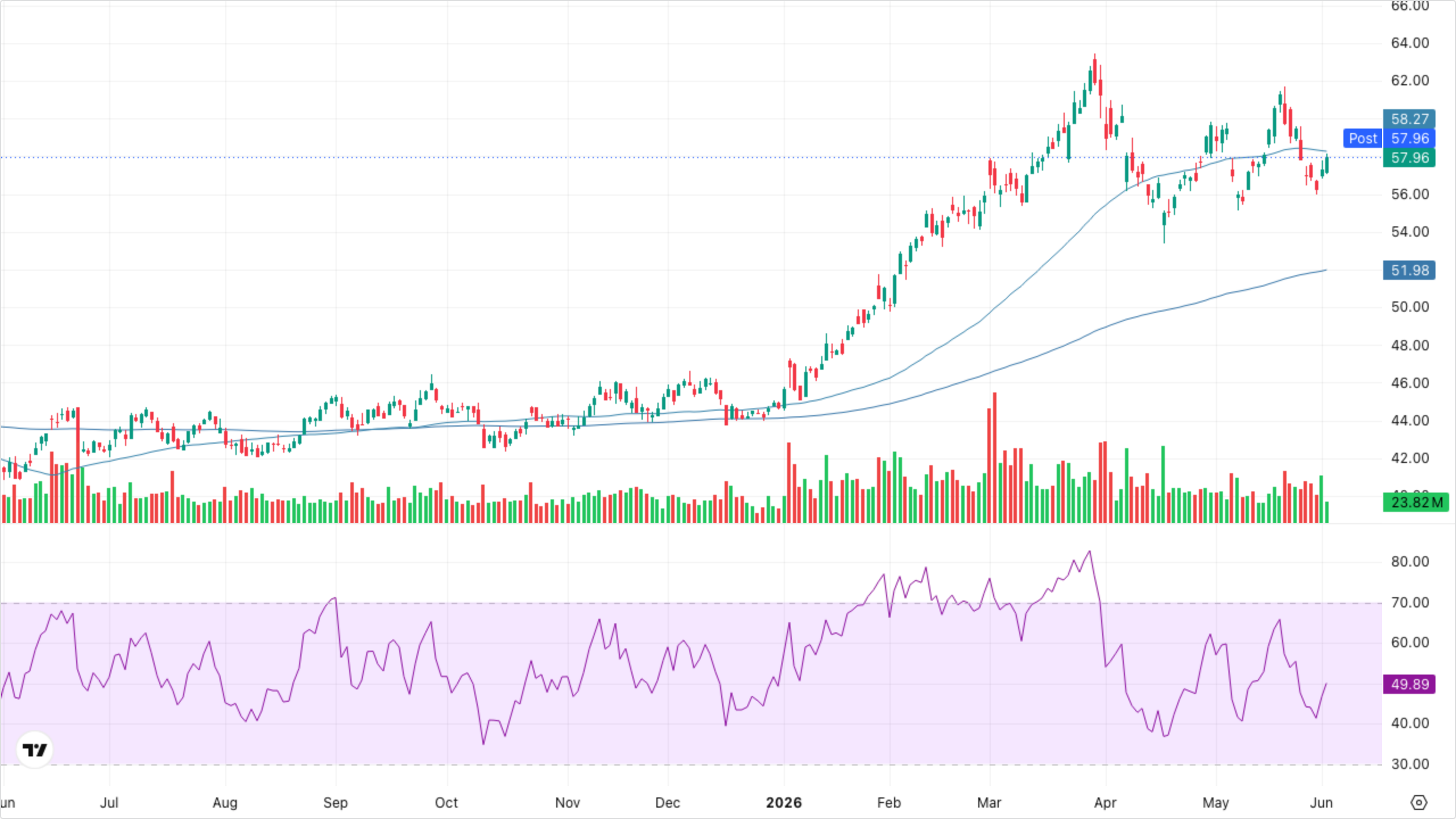

Mixed. WTI +0.88% to $94.20 is the standout — still elevated from the prior session's surge. Gold flat at $4,487, silver -0.27%, copper -0.09%. If oil were a true regime-changer, we'd expect breakevens leaking through into yields; we're not seeing that.

Risk Appetite

Unambiguously risk-on. VIX -1.87% to 15.76, VIXY -1.64% to 23.46 and printing new cycle lows. DXY essentially unchanged at 99.22. No flight-to-safety bid.

Equity Regime

Small-cap leadership stands out: Russell 2000 +0.90% vs. SPX +0.13%. Combined with cyclicals (XLE, XLB, XLI) outperforming and tech still bid, the rotation is broader and more pro-growth than the headline index print suggests.

Global

VT +0.47% — global equity participating with US. USD/JPY at 159.94, USD/CNY at 6.76, EUR/USD at 1.16. FX quiet, no cross-border stress signal.

The weight of evidence points to Goldilocks, with a reflation overlay worth monitoring if crude stays bid.