Goldilocks holds — rotation broadens beneath megacap stall.

Breadth is the story. The Dow ripped +1.46% and the Russell 2000 +1.52% while megacap tech sagged — Caterpillar and Eli Lilly earnings drove industrials (XLI +2.50%) and health care (XLV +2.16%) to the top of the leaderboard, with utilities and staples joining for the ride. Disinflationary signals reinforce the call: WTI −3.49% to 104.71, DXY −0.80%, VIX −7.34% to 17.42, and the 5Y yield easing to 4.03%. Tech is the only sector red on the tape (XLK −0.38%), and that is rotation, not regime change.

TL;DR

- 📈 Dow +1.46%, Russell +1.52% — old-economy and small-cap leadership; SPX +0.54%, NDX a laggard +0.38%.

- 🏭 XLI +2.50%, XLV +2.16%, XLU +2.05% — industrials, health care, utilities all leading; tech the only red sector.

- 🛢️ WTI −3.49% to 104.71 — sharpest crude drop in weeks easing the inflation impulse.

- 🇯🇵 USD/JPY −2.34% to 156.69 after Japan’s “final warning” verbal intervention; yen posts strongest day since mid-March.

- 🧊 VIX −7.34% to 17.42 alongside DXY −0.80% and gold +1.47% — financial conditions ease across the board.

Market News

Earnings carrying the tape this morning: Caterpillar reportedly jumped on a beat that lifted the Dow by hundreds of points, while Eli Lilly surged on stronger-than-expected weight-loss drug results — both flowed straight into XLI and XLV leadership. The other side of the megacap trade saw Microsoft, Salesforce, and Nvidia trading heavy, capping NDX upside at +0.38%. In FX, Japan’s top currency officials issued what was characterized as a “final warning” verbal intervention after USD/JPY pierced 160 overnight; the pair then collapsed roughly 240 pips into the morning, with the yen posting its strongest daily move since mid-March. Crude meanwhile gave back recent gains as the geopolitical risk premium fades intraday.

Charts

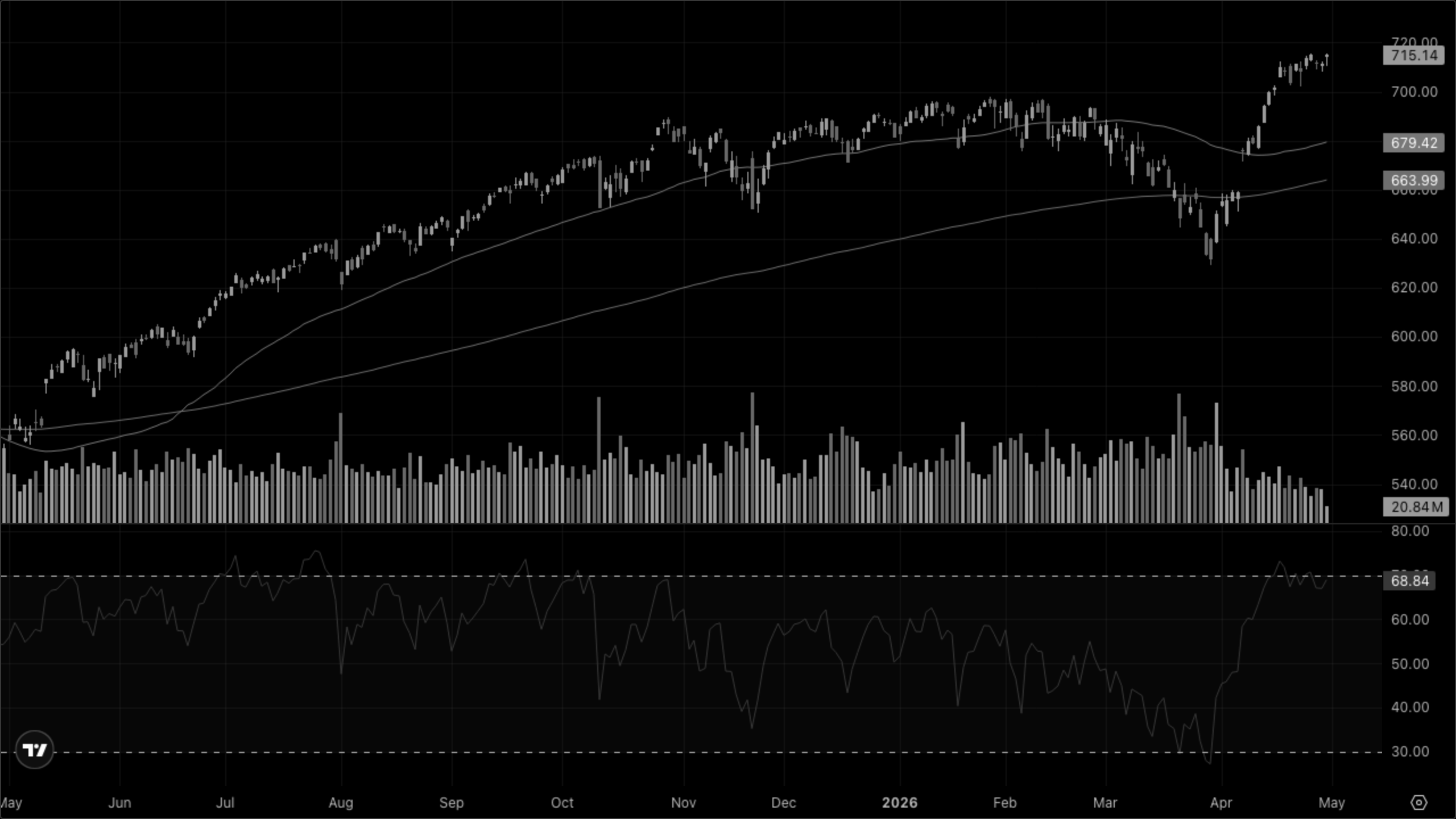

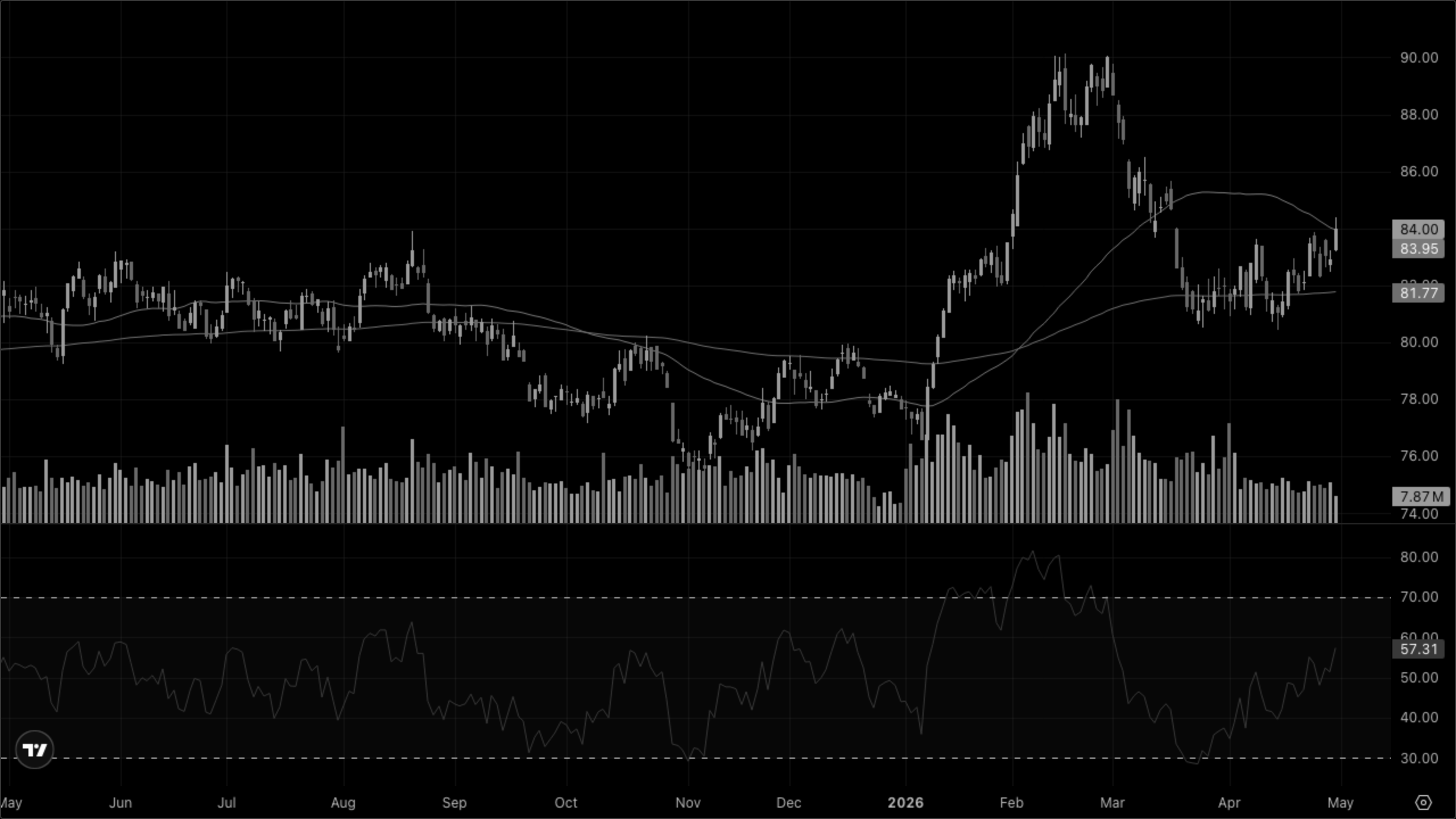

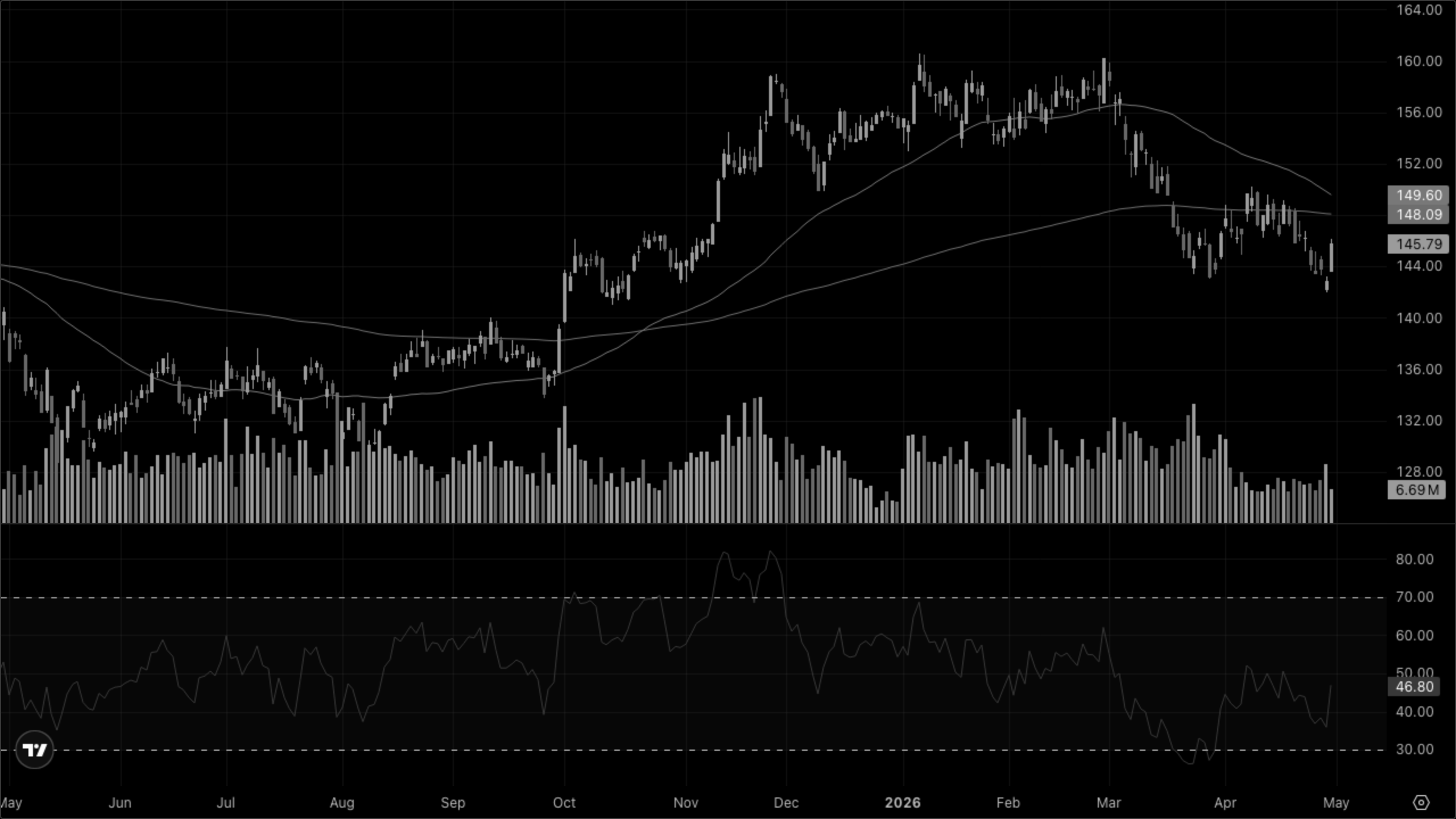

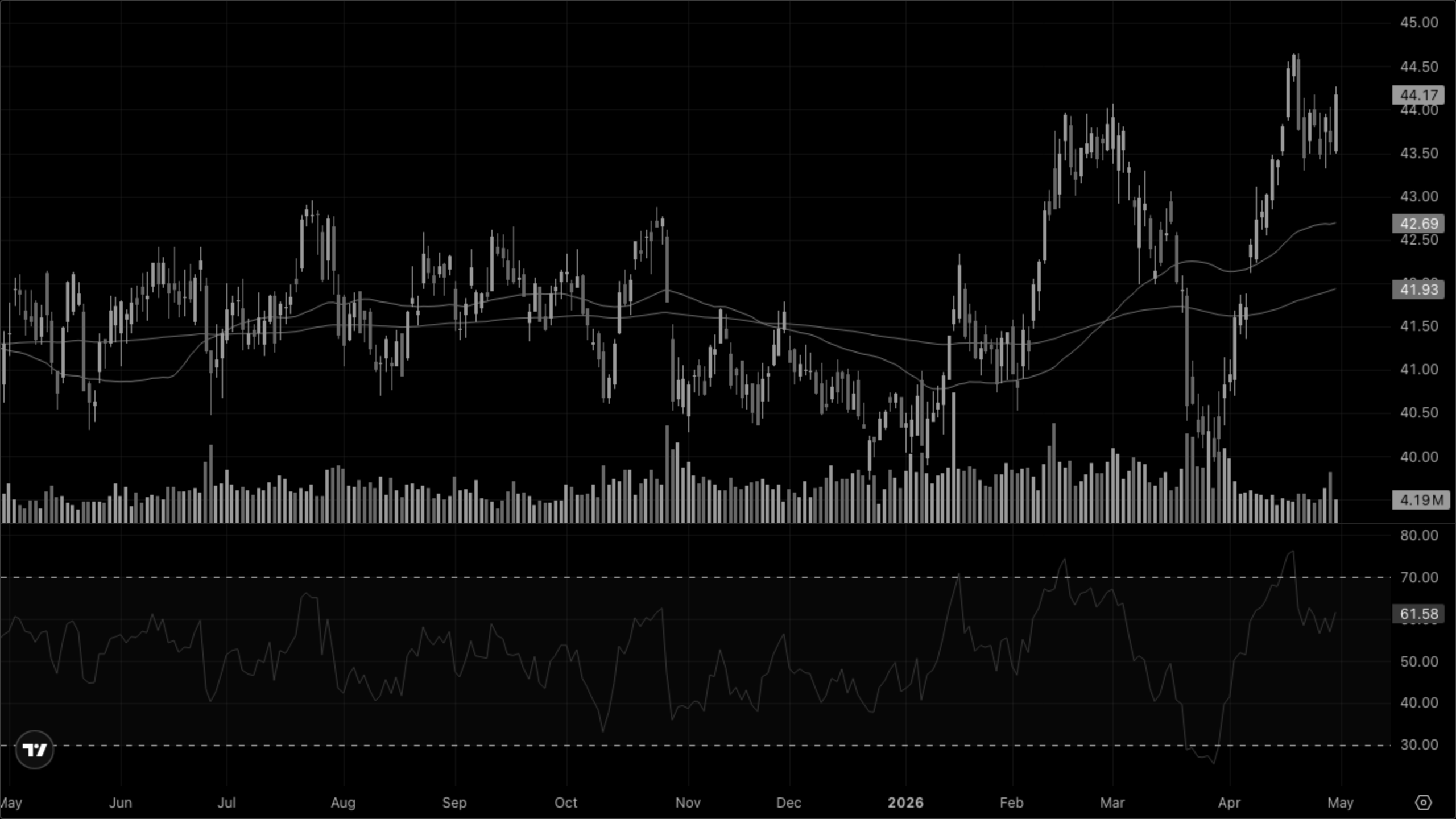

VT (Global Equity)

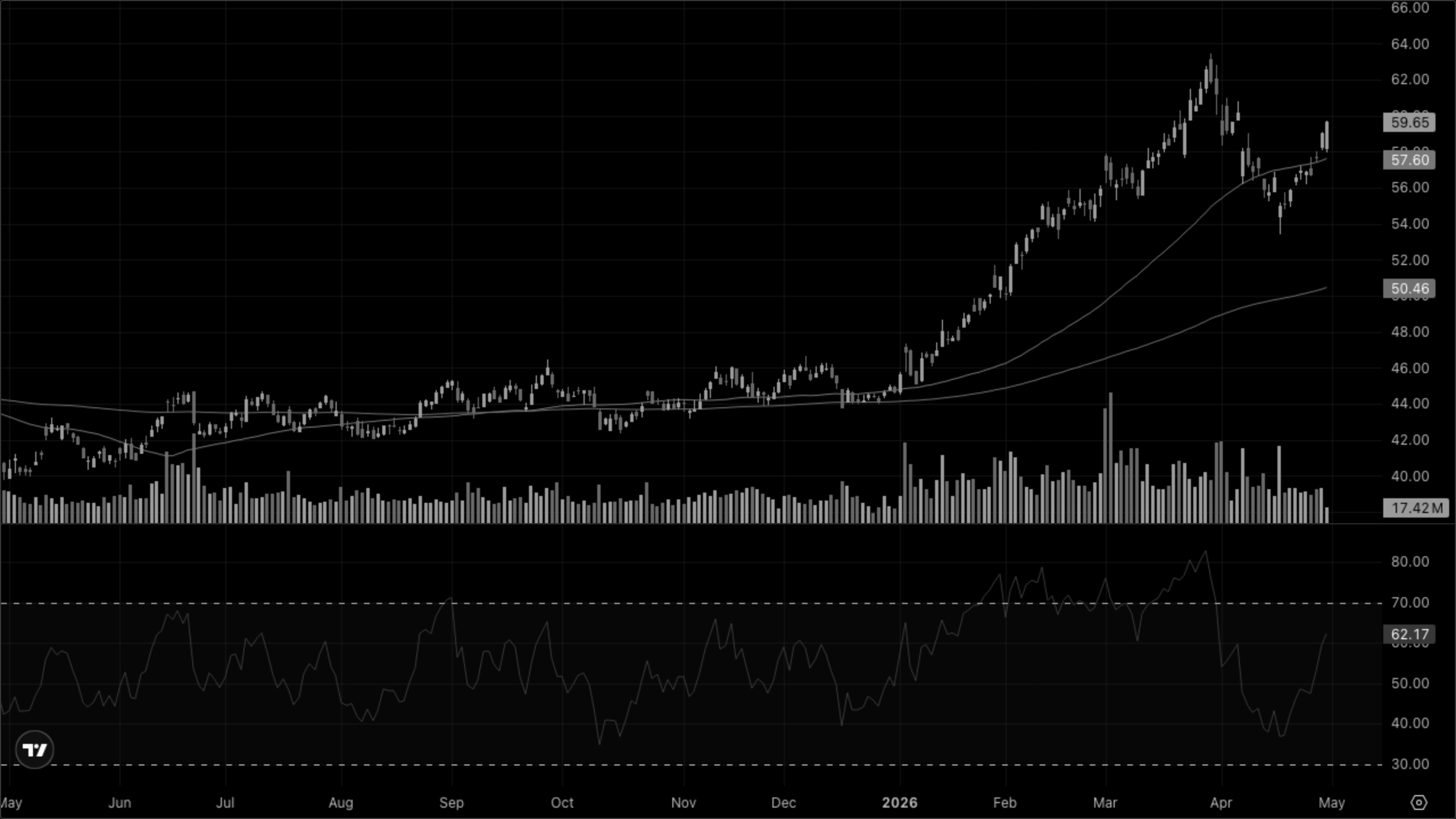

SPY (S&P 500)

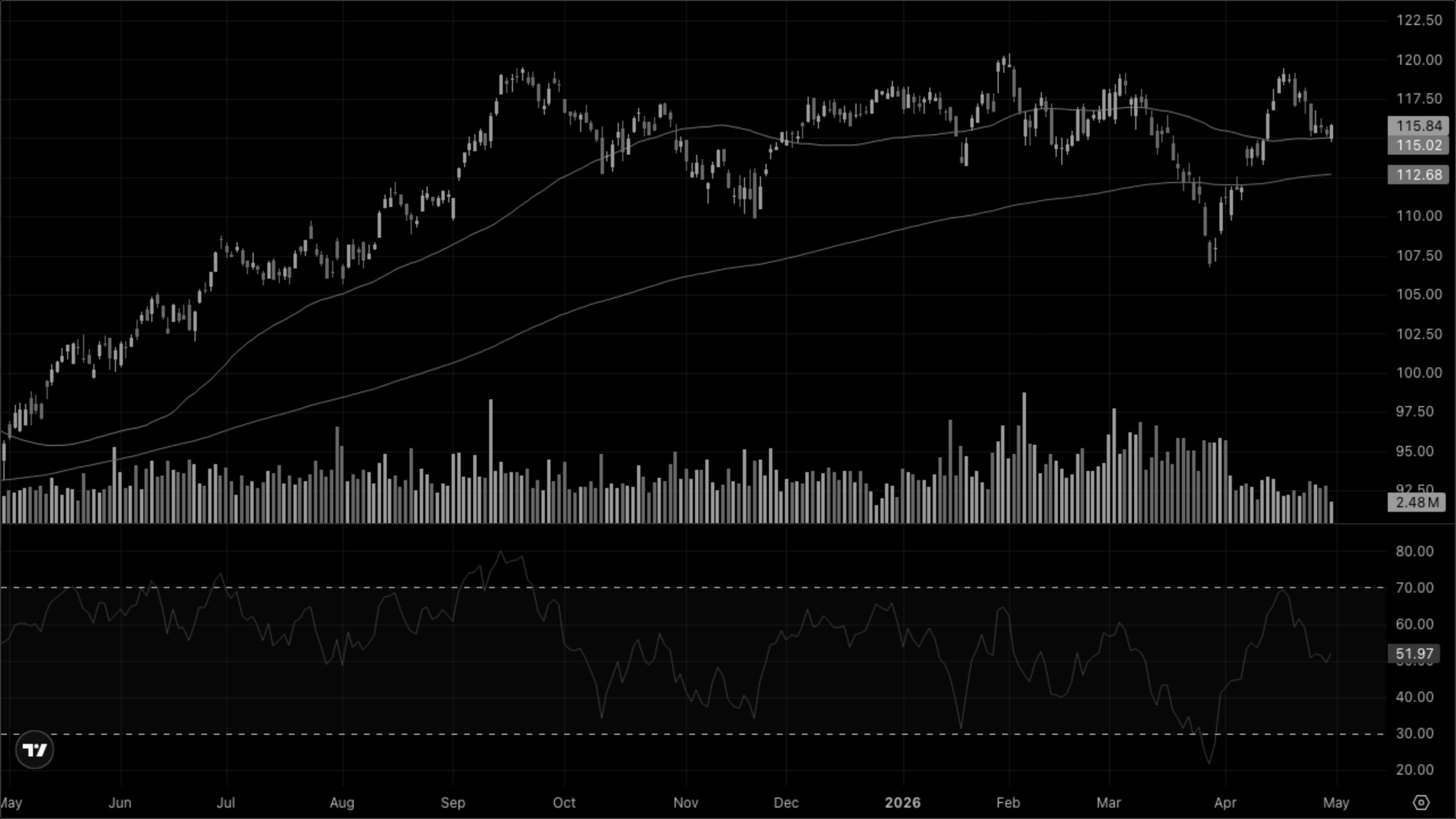

QQQ (Nasdaq-100)

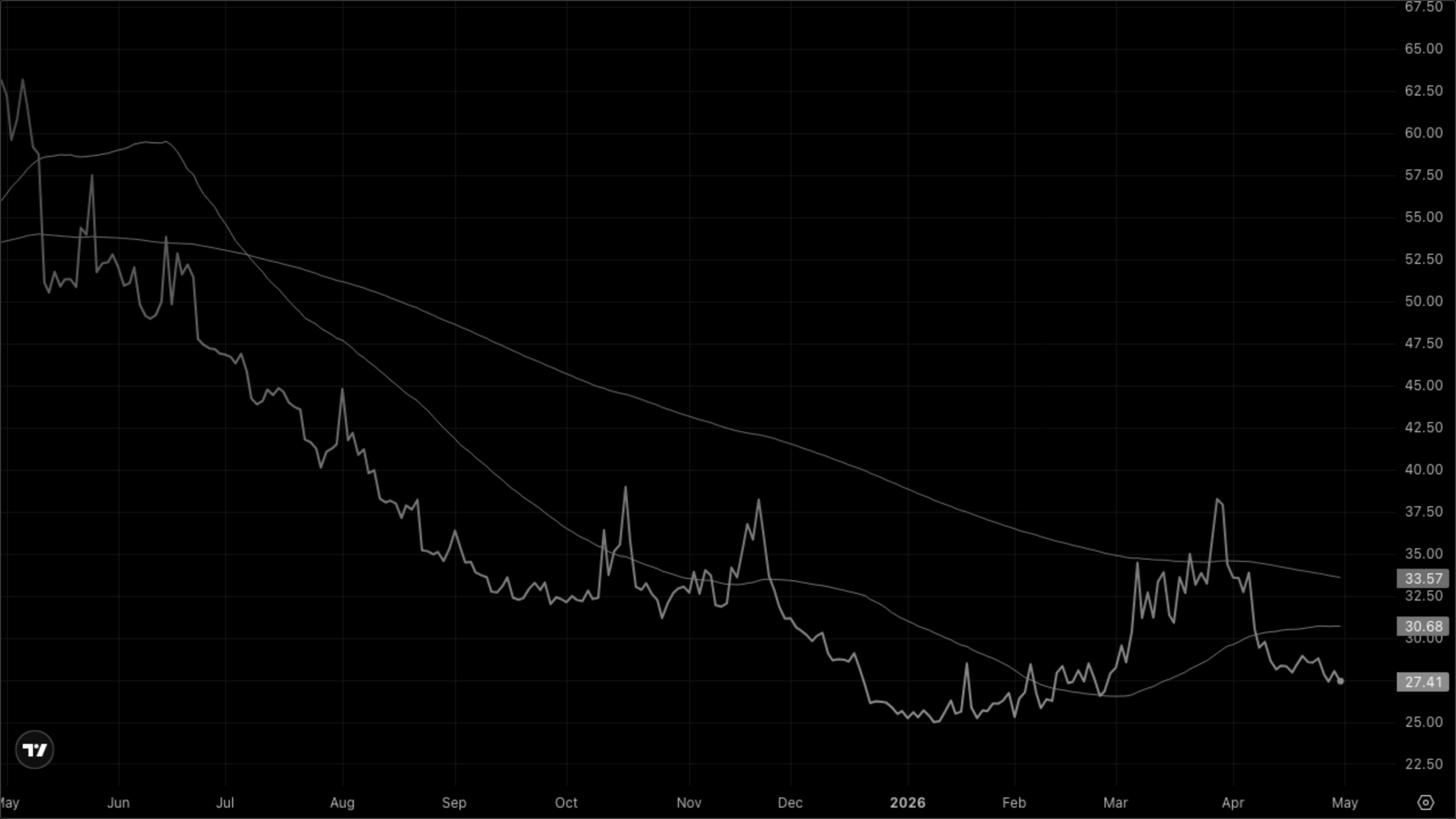

VIXY (VIX Short-Term Futures)

Sector Quadrants

Goldilocks — Growth + Disinflation

Risk-on leaders when growth is strong and inflation fades

XLK — Technology

XLY — Discretionary

XLC — Comms

Reflation — Growth + Inflation

Cyclicals that benefit from rising prices and activity

XLE — Energy

XLB — Materials

XLI — Industrials

Stagflation — Contraction + Inflation

Defensives that hold up when growth stalls but prices stay hot

XLP — Staples

XLV — Health Care

XLU — Utilities

Deflation — Contraction + Disinflation

Rate-sensitive sectors that benefit from falling yields

XLRE — Real Estate

XLF — Financials

Today’s leadership splits awkwardly across quadrants. Industrials carry the Reflation banner (XLI +2.50%) on Caterpillar, but the “Stagflation” defensives are right behind (XLV +2.16%, XLU +2.05%, XLP +1.42%) — that combo is more “earnings-driven defensives plus broadening cyclicals” than a true stagflation tilt, especially with WTI down hard and DXY soft. Goldilocks tech is the lone red corner; the broad green print plus disinflationary commodities still skews the regime call to Goldilocks with a value/late-cycle flavor.

Cross-Asset Narrative

Rates & curve. The 5Y eased to 4.03% (−4bp) and the 30Y to 4.98% — a modest bull-flatten on the visible legs, consistent with disinflation and easing risk premium rather than growth fear.

Inflation pulse. Mixed but net dovish: WTI −3.49% to 104.71 is the dominant signal; gold +1.47% and silver +2.67% are catching a bid almost entirely on dollar weakness (DXY −0.80%) rather than reflation. Copper +0.67% — incremental, not thematic.

Risk appetite. Decisively risk-on under the surface: VIX collapses −7.34% to 17.42, VIXY −2.14%, and the dollar drops alongside — that’s the textbook financial-conditions easing combo.

Equity regime. Clear small-cap and value rotation: Russell +1.52% beats SPX +0.54% beats NDX +0.38%. Cyclical industrials over megacap tech is healthy breadth, not breakdown.

Global. The yen story is the day’s biggest non-equity move — USD/JPY −2.34% after Japanese officials’ “final warning” verbal intervention. EUR/USD +0.42% and USD/CNY −0.14% round out broad-based dollar weakness.

The weight of evidence points to Goldilocks.

What to Watch

- 📊 If 10Y/5Y yields drift further while VIX stays sub-18, then Goldilocks gets reinforced — financial conditions doing the heavy lifting.

- 🛢️ If WTI loses 100 then disinflation becomes the dominant macro narrative; if it reclaims 110 on Mideast headlines, stagflation odds rise quickly.

- 🇯🇵 If USD/JPY breaks back above 158 despite verbal intervention, then expect actual MOF/BOJ action — global vol spillover risk.

- 💵 If DXY breaks below 98 then the metals/EM bid extends; a bounce above 99 would stall today’s reflation-lite rotation.

- 🏦 If XLF and XLRE join the rally (currently lagging at +0.36% and +1.16%), that confirms broad participation — failure to follow would flag a defensive twist beneath the surface.