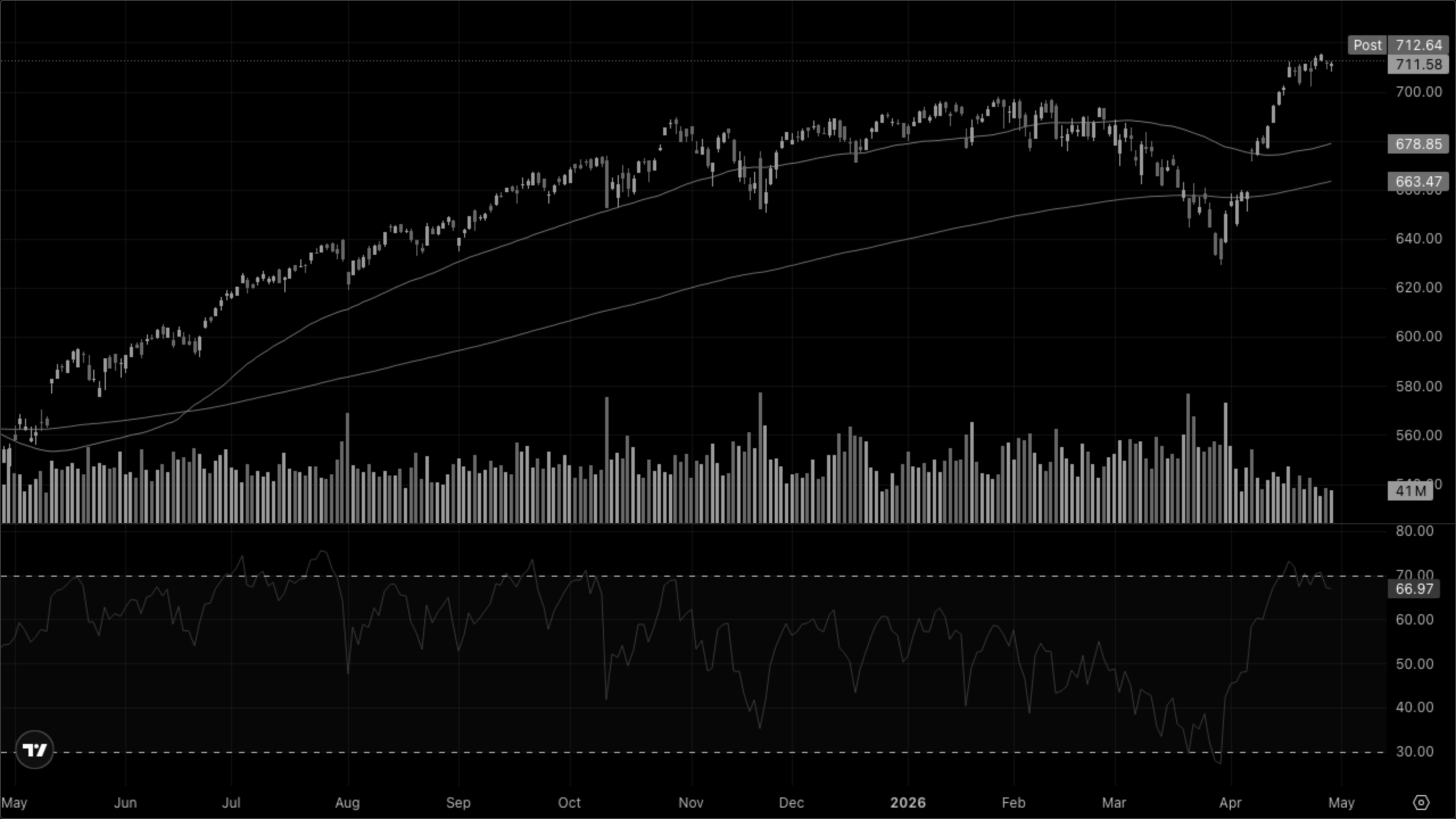

Stagflationary impulse strengthening into the close.

The tape is splitting along regime lines. The long end is selling off (30Y at 5.00%, 5Y +10bp to 4.08%), oil sits above $108, and gold is pinned near $4,550 — classic falling-growth-plus-rising-inflation signatures. Equities look like a single-factor market: the Nasdaq 100 is up 0.58% on mega-cap tech (XLK +0.80%) while Russell 2000 (-0.60%), industrials (-0.61%), healthcare (-0.70%) and utilities (-1.23%) are all heavy. VIXY is bid +2.26%. Underneath the headline NDX print, this is a defensive-rate-sensitive selloff with cyclicals leaning over.

Cross-Asset Narrative

Rates & curve

The long end is the story. 5Y +10bp to 4.08%, 30Y +6bp to a round 5.00% — the 5s30s is compressing as the belly underperforms, and the broader curve is bear-steepening on the day. With oil holding triple digits, the term-premium repricing makes sense: the market is no longer paying up for duration when realized inflation pressure refuses to fade.

Inflation pulse

Crude at $108.35 is the regime input that matters most right now — copper flat at $5.93 and silver $71.52 don't argue against it, and gold at $4,549 sits near its highs. There is no disinflation impulse in this snapshot.

Risk appetite

VIXY +2.26% with the long end selling off and small caps -0.60% is a defensive bid forming under a green-tape NDX print — the kind of split where the index masks deteriorating internals.

Equity regime

Mega-cap growth (XLK) up while Russell, industrials, healthcare, and utilities all sell — this is narrowing leadership, not broad participation. Watch whether tech can carry alone if rates keep grinding higher.

The weight of evidence points to a stagflationary impulse — high oil, rising long-end yields, narrow large-cap leadership, and defensives under pressure from the rate move.