The day closed with the regime signature getting sharper, not softer. Growth-cyclical leadership cracked — Nasdaq 100 finished -1.01% at 27,029.01, Russell 2000 -1.15% at 2,756.05, and XLK gave back -1.69% in a session where mega-cap tech could not hold a bid. At the same time, the inflation-sensitive complex did the opposite of what a cooling economy would imply: copper popped +1.56% to 6.01, silver added +0.99% to 73.76, and gold ground higher by +0.18% to 4,603.34 even as the dollar firmed (DXY +0.07% to 98.67). WTI hovering at 99.34 keeps the energy input cost story alive.

The leadership tape inside equities tells the same story. Staples (XLP +0.90%), Real Estate (XLRE +0.97%), and Utilities (XLU +0.13%) — the classic defensive triumvirate — were the only sector ETFs in our snapshot finishing green of any size, while every cyclical-growth proxy bled. That is not a clean reflation rotation; that is defensives + hard assets, which is the textbook stagflation footprint. The long end behaved consistently: the 30Y eased -0.01 to 4.94% while the belly (5Y) firmed +0.03 to 3.98%, a flattening shape consistent with the market pricing slower forward growth alongside sticky near-term price pressure.

TL;DR

📉 Growth equities led the slide — Nasdaq 100 -1.01% to 27,029.01, Russell 2000 -1.15% to 2,756.05, XLK -1.69%.

🛡️ Defensives caught the bid — XLP +0.90%, XLRE +0.97%, XLU +0.13%; the only green corners of the equity tape.

🟠 Industrial metals strong — copper +1.56% to 6.01, silver +0.99% to 73.76; inflation-pulse very much alive.

🪙 Gold held firm at 4,603.34 (+0.18%) despite DXY +0.07% — hard-asset bid uncoupled from dollar move.

🏦 Curve flattened — 5Y +3bp to 3.98%, 30Y -1bp to 4.94%; growth concerns at the long end, sticky inflation in the belly.

Watchlist

Economic Calendar

Market News

Charts

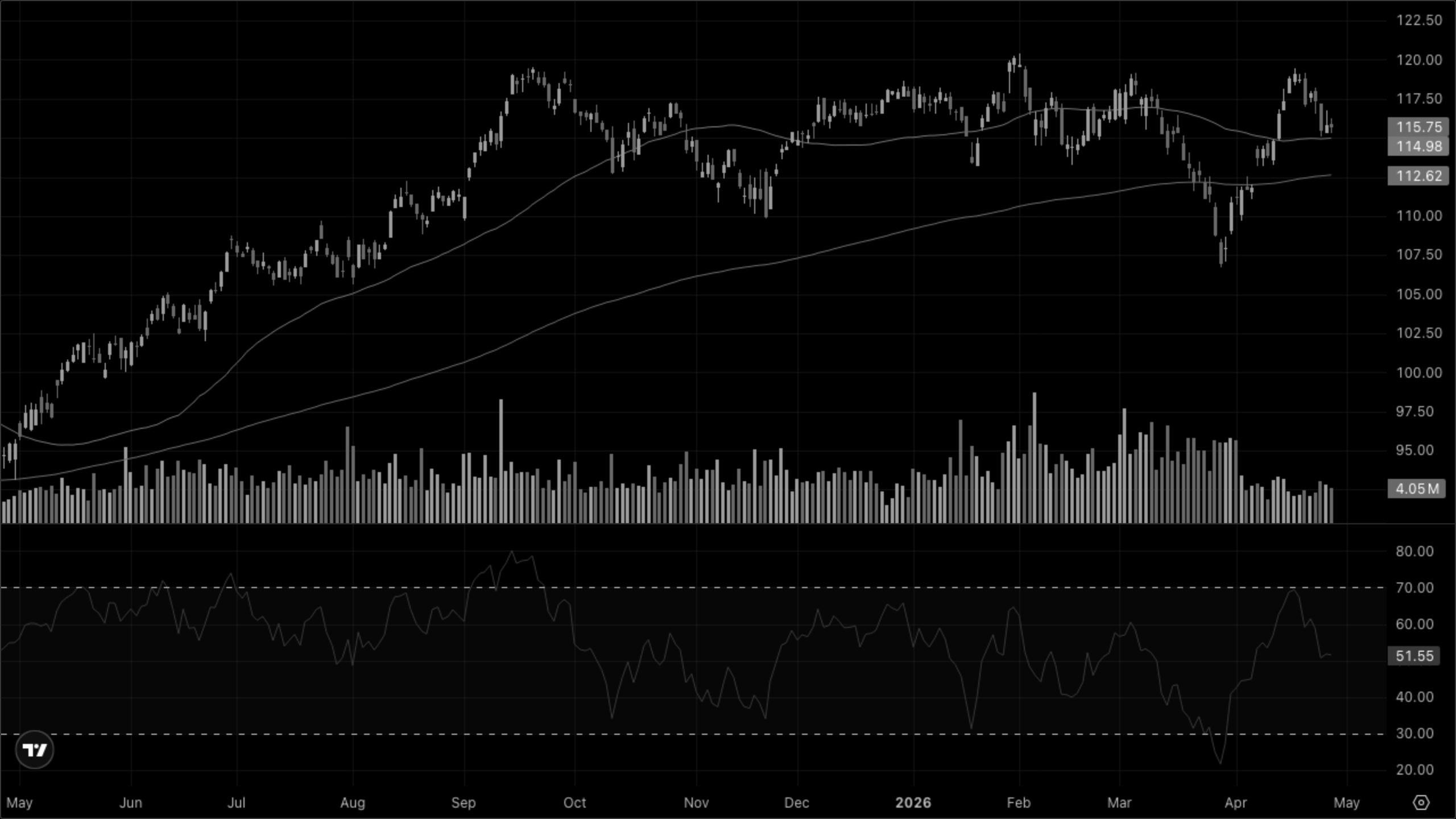

VT (Global Equity)

Hovering near recent highs and well above both SMA 50 and EMA 200, but RSI has rolled off the upper band toward the low-60s — momentum cooling without a trend break.

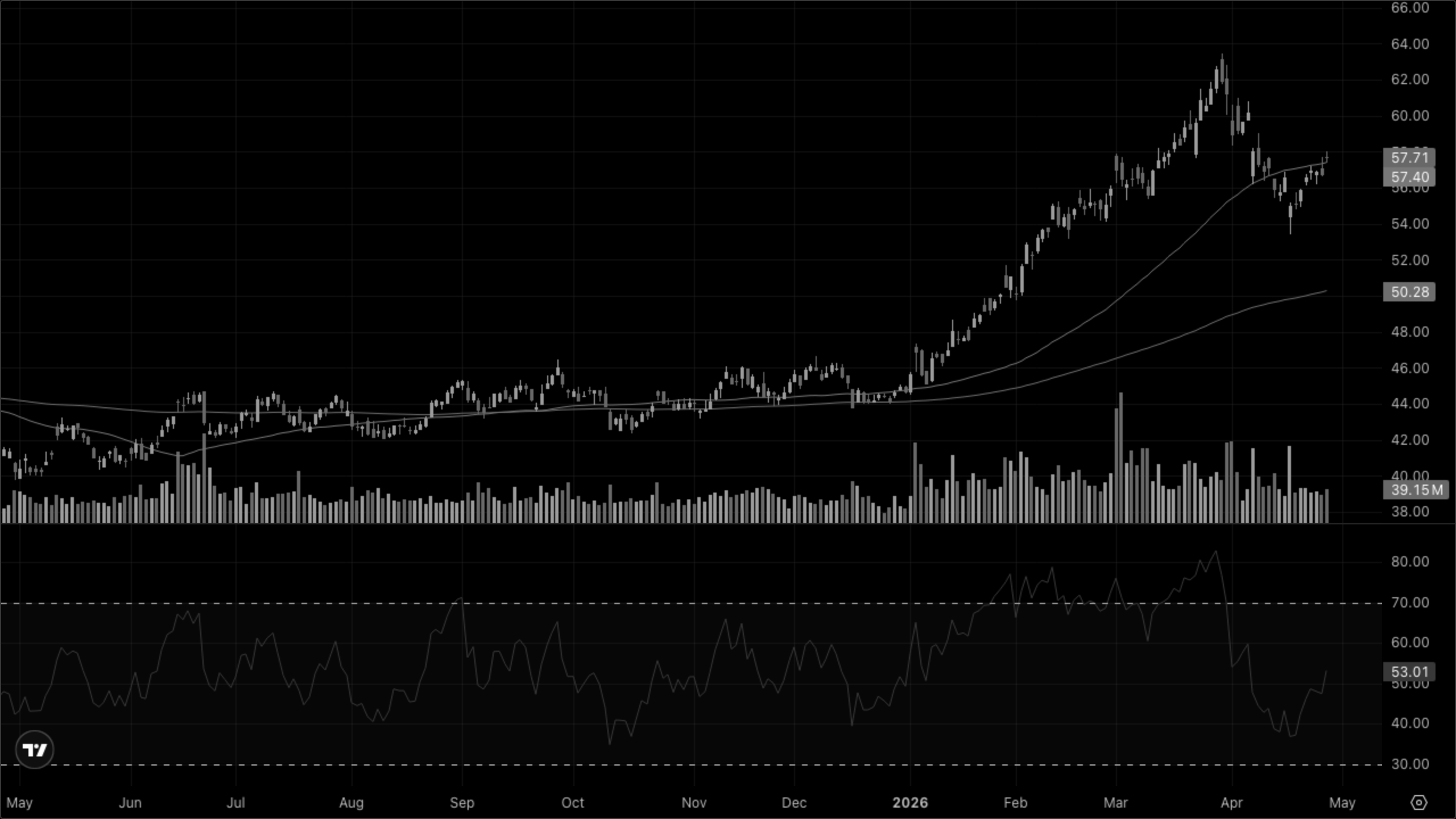

SPY (S&P 500)

Price still above SMA 50 and EMA 200 with the 50 sitting comfortably over the 200, but the RSI has drifted from overbought back to a neutral mid-60s read — classic distribution pattern after a sharp recovery.

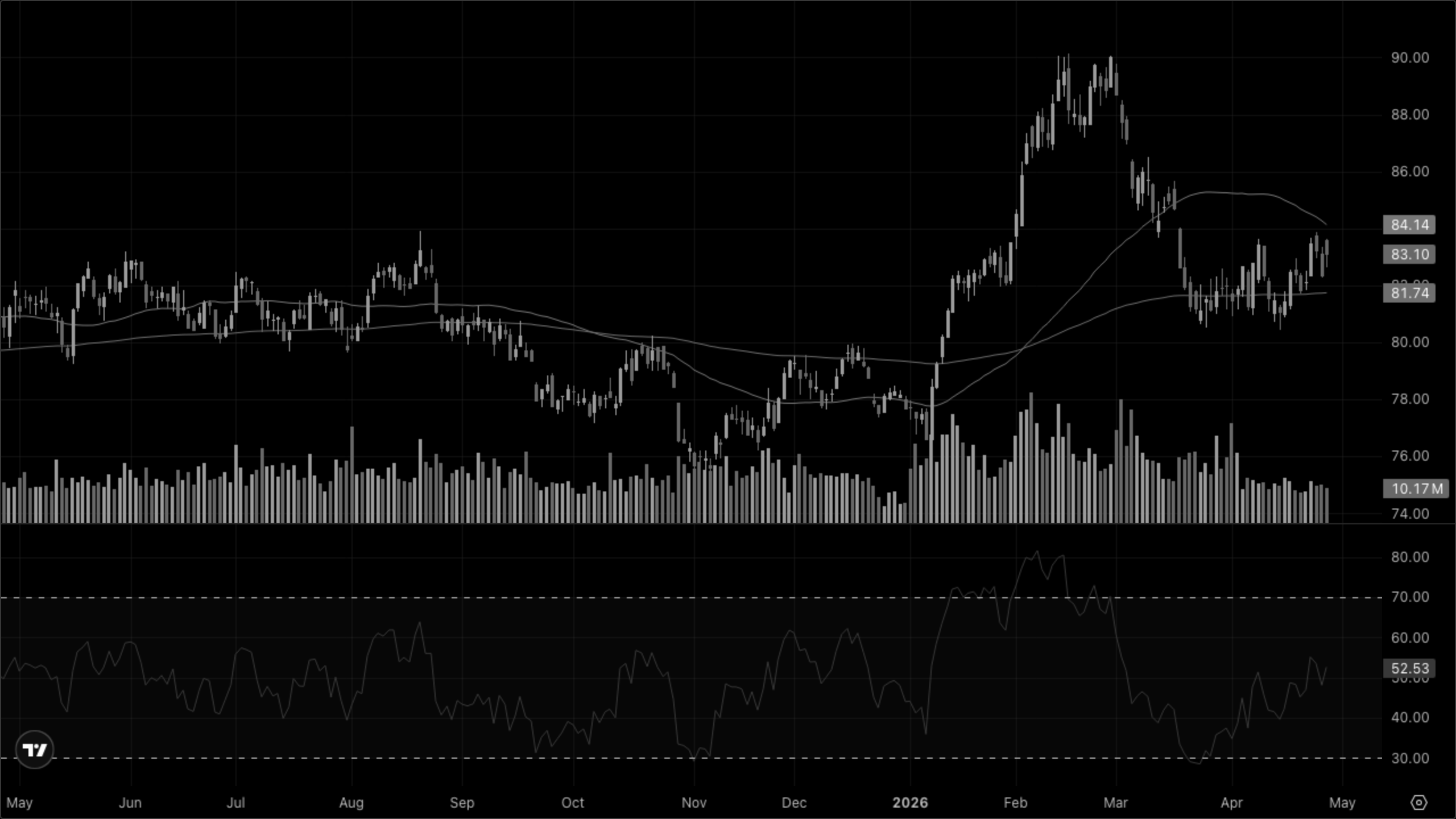

QQQ (Nasdaq-100)

Strong V-recovery has carried QQQ back above both moving averages and to fresh nominal highs, but today's red bar prints with RSI fading from overbought — first warning that the vertical leg is losing thrust.

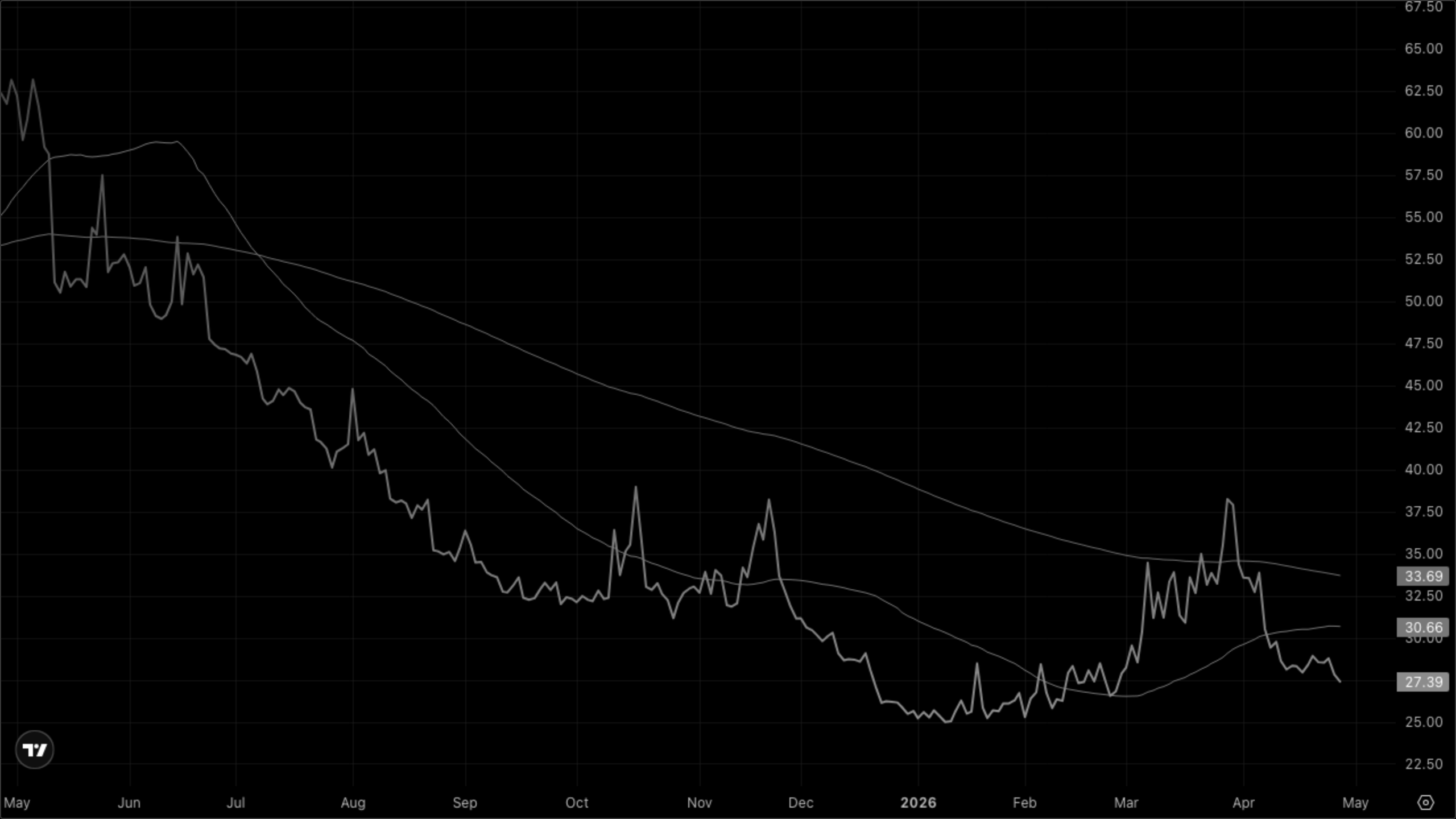

VIXY (VIX Short-Term Futures)

Pulled back into the low end of the recent range and now trading below SMA 50, but still well off the multi-month lows — vol is bid relative to the prior regime, just compressed today.

Sector Quadrants

Goldilocks — Growth + Disinflation

Risk-on leaders when growth is strong and inflation fades

XLK — Technology

XLY — Discretionary

XLC — Comms

Reflation — Growth + Inflation

Cyclicals that benefit from rising prices and activity

XLE — Energy

XLB — Materials

XLI — Industrials

Stagflation — Contraction + Inflation

Defensives that hold up when growth stalls but prices stay hot

XLP — Staples

XLV — Health Care

XLU — Utilities

Deflation — Contraction + Disinflation

Rate-sensitive sectors that benefit from falling yields

XLRE — Real Estate

XLF — Financials

Today's quadrant scoreboard is the cleanest signal we've had in a while: Goldilocks (XLK, XLY, XLC) all red, Reflation cyclicals (XLB, XLI) red, while Stagflation defensives (XLP, XLU) and the rate-sensitive Real Estate corner (XLRE) all printed green. That's a defensive + hard-asset combination — sectors that prefer either falling growth or stuck-high prices, not the early-cycle reflation mix. The split confirms rather than contradicts the stagflation lean coming through in commodities and the curve.

Cross-Asset Narrative

Rates & curve. The story is in the shape, not the level. The 5Y added 3bp to 3.98% while the 30Y eased 1bp to 4.94% — a long-end-led flattening, which historically signals the market reducing its growth expectations even as front- and belly-end inflation pricing stays sticky. Without an explicit 2s10s in the snapshot, the 5s30s spread itself compressed today.

Inflation pulse. Loud. Copper +1.56% to 6.01 is the standout — Dr. Copper rarely moves 150bp in a session without a real demand impulse or a supply shock making news. Silver added 0.99% to 73.76 and gold ground higher to 4,603.34 despite a firmer dollar. WTI ticked down 27 cents to 99.34 but is still pinned near triple digits. The inflation gauge is anything but cooling.

Risk appetite. Mixed but defensive. VIXY fell 1.51% to 27.39, suggesting no acute stress, yet the level itself is elevated relative to the early-year regime. DXY firmed 0.07% to 98.67 — modest haven bid in FX. The combination of softer vol with weaker growth equities is consistent with orderly de-risking, not a panic.

Equity regime. The rotation today was decisive: large-cap growth out, defensives and rate-sensitives in. Russell 2000 -1.15% underperforming the larger caps argues against a cyclical revival — small caps usually lead in true reflation. XLF essentially flat (+0.08%) despite a flatter curve is notable; banks that should hate flattening shrugged.

Global. VT -0.57% to 149.46 underperformed not in absolute terms but relative to the magnitude of the US tech drawdown — non-US equity may be cushioning. USD/JPY at 159.63 keeps the BoJ-watch trade alive; USD/CNY essentially unchanged at 6.84.

The weight of evidence points to stagflation.

What to Watch

🟠 Copper follow-through. If copper holds above 6.00 and grinds higher tomorrow, the inflation-pulse signal hardens and the stagflation regime gets more confident; a sharp reversal would suggest today's pop was a one-off.

🏦 Long end behavior. If 30Y yield breaks below 4.90% with the 5Y still firm, the curve-flattening growth-fear narrative gets louder — bullish duration, defensive equities, gold.

📉 Russell 2000 vs Nasdaq. If small caps continue to lag tomorrow, the cyclical-weakness read is confirmed; an IWM-led bounce would partially walk back the regime call.

🪙 Gold + DXY decoupling. If gold extends above 4,610 with DXY also higher, that is a textbook stagflation hedge; gold falling on a stronger dollar would be a normalization sign.

⚡ VIXY direction. A move back above 28.50 alongside another red equity day would shift the read from orderly de-risking toward something more concerning; sustained moves below 27 would argue the tape is just digesting, not breaking.