Stagflation rotation back in the driver's seat.

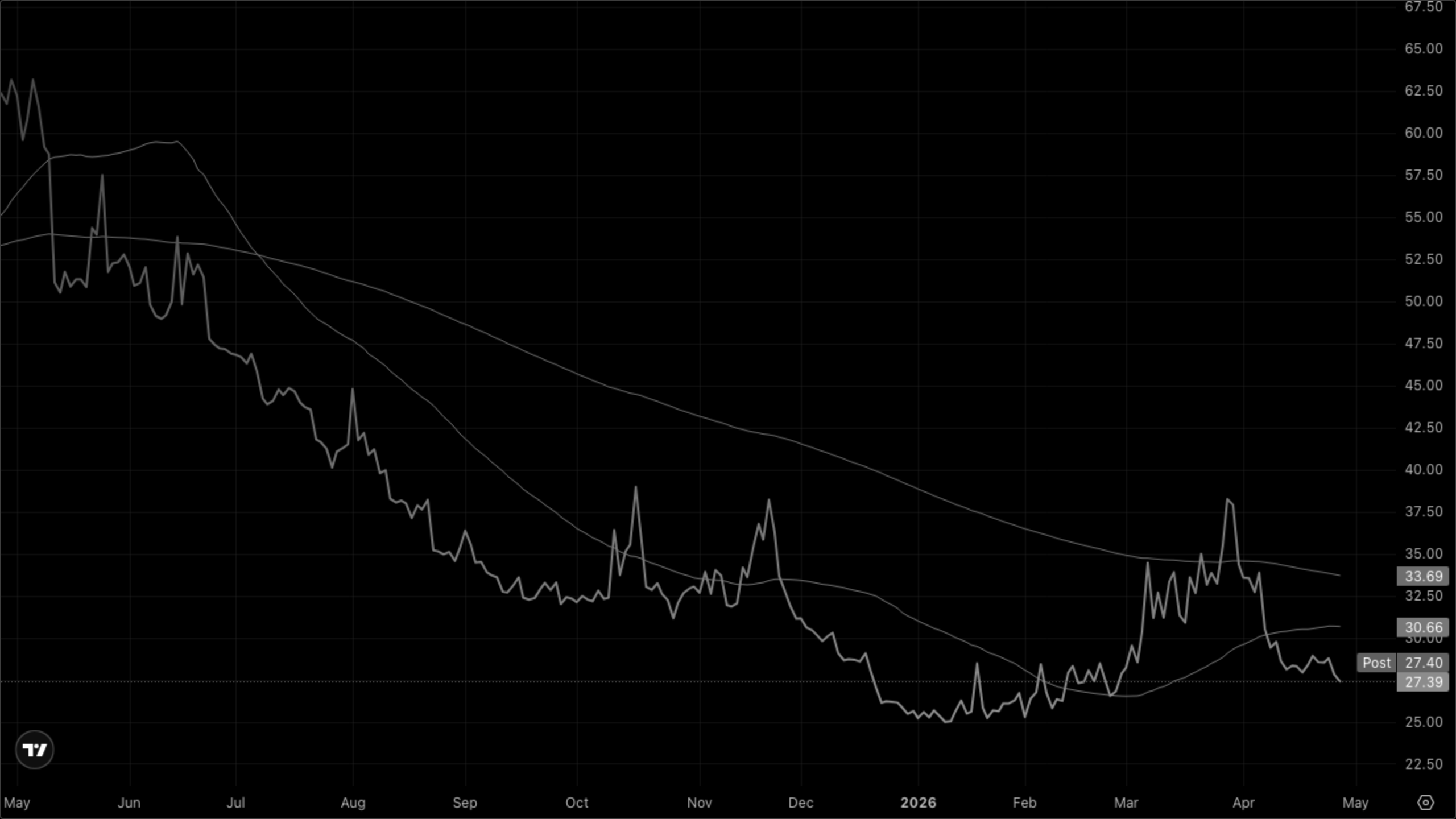

An OpenAI revenue/user miss leaked by the WSJ has knocked the AI complex hard — chipmakers down 2–5%, Nasdaq 100 off 1.0%, Russell 2000 off 1.2%. Underneath, the tape is doing something more important than the headline: XLE +1.66%, XLP +0.90%, XLRE +0.97% bid; XLY -0.70%, XLB -0.73%, tech soft. Oil holding $99+ on UAE-leaves-OPEC and Iran tensions, gold parked near $4,600, copper +1.0%, 2Y yield +4bp to 3.84%. That is a textbook stagflation-defense rotation, not a clean risk-off — credit-sensitives and defensives are absorbing flows leaving growth.

Market News

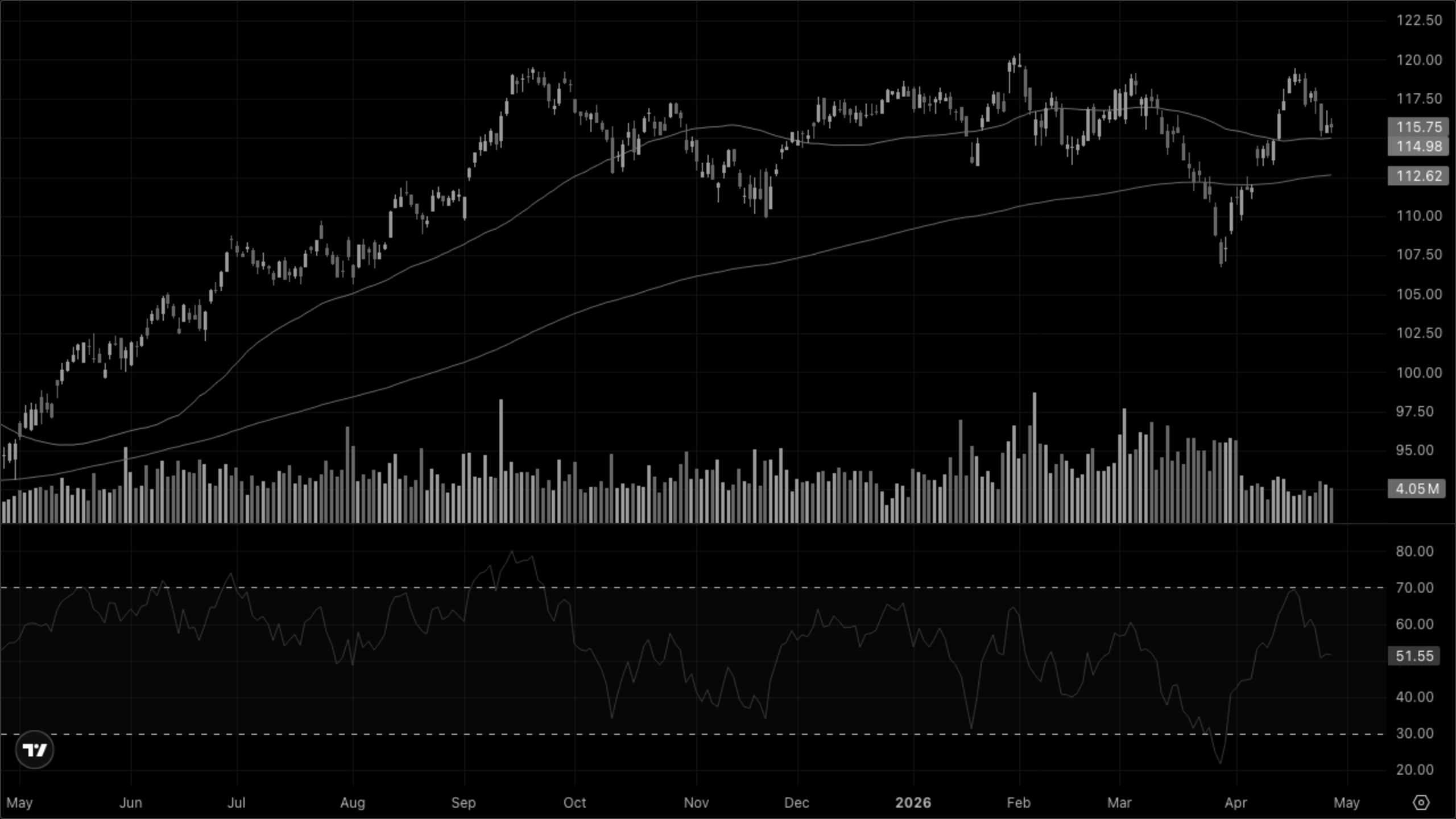

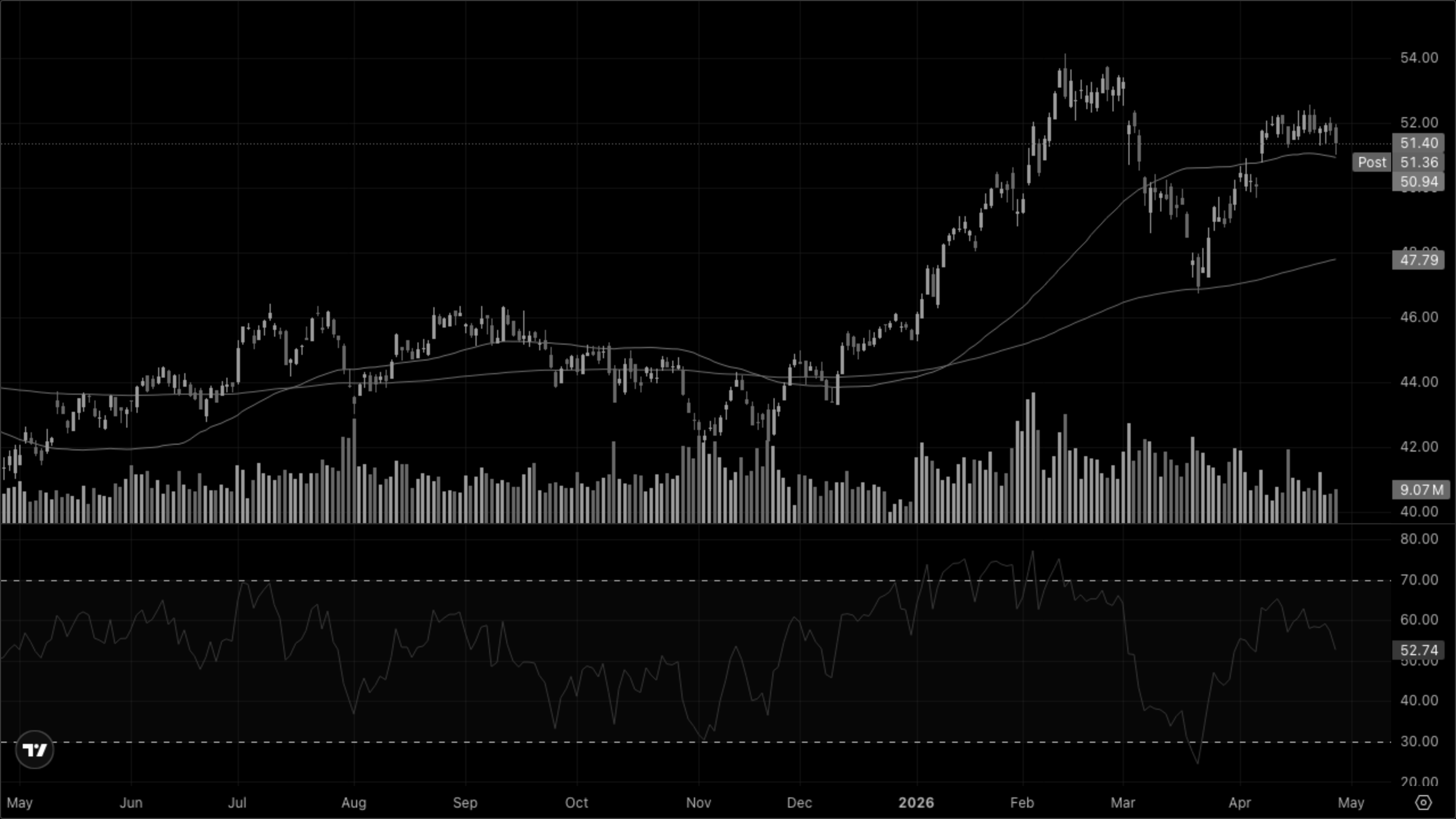

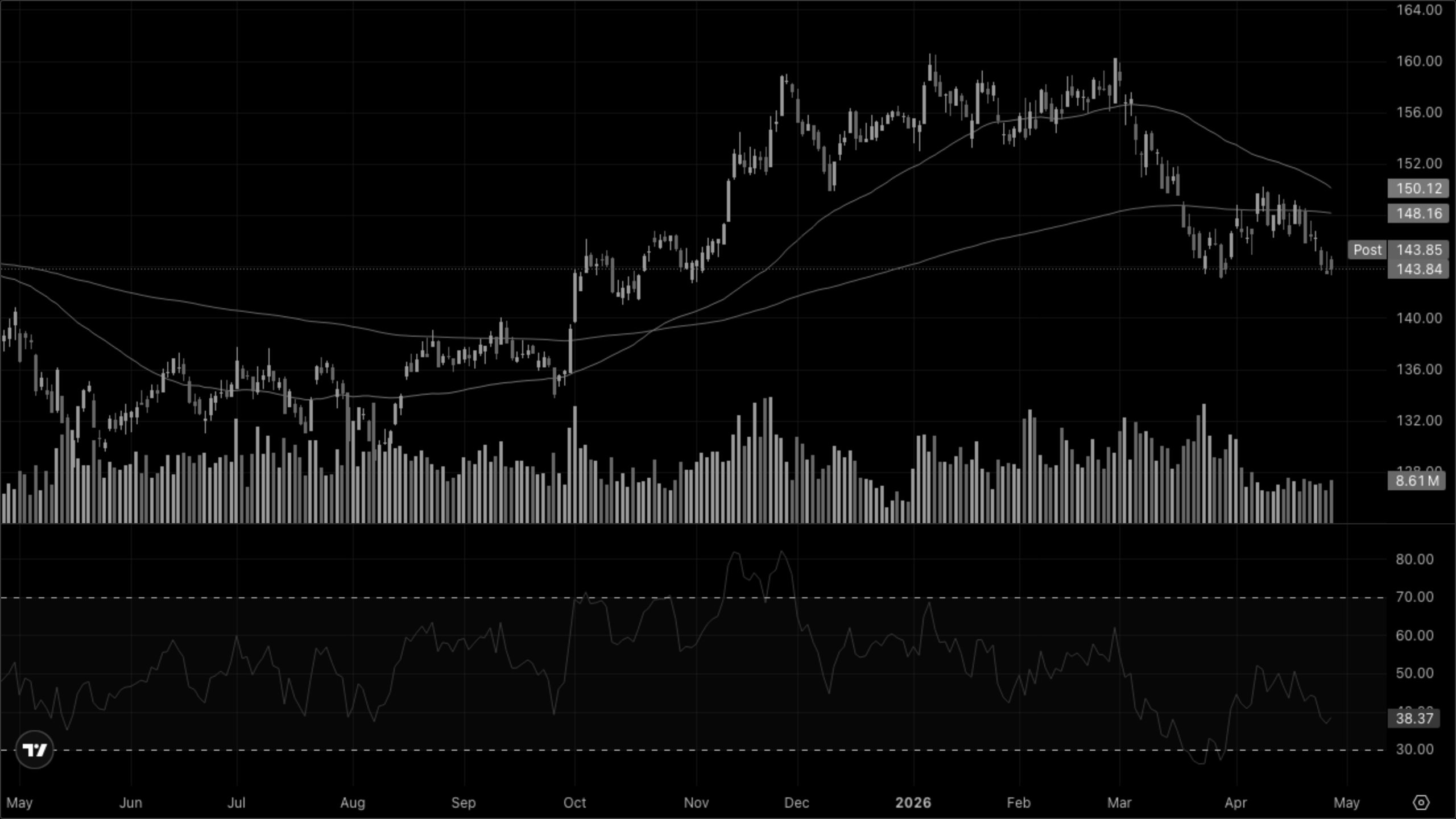

The story of the session: A WSJ report claimed OpenAI is missing internal user and revenue targets, igniting a sharp re-pricing of AI capex beneficiaries. Per session reporting, Oracle and CoreWeave led declines among OpenAI-tied names; Nvidia, Broadcom, and AMD fell roughly 2–5%; Qualcomm -3.5%. OpenAI denied the report. Defensive blue-chips outran the tape — General Motors and Coca-Cola gained on earnings beats — and energy held up as oil firmed on UAE's announced exit from OPEC and renewed U.S.–Iran friction. The week is loaded: Alphabet, Amazon, Meta, and Microsoft all report, and the market is now squarely focused on AI spend vs. monetization.

Cross-Asset Narrative

Rates & curve: The front end did the work — 2Y +4bp to 3.84%, 5Y +3bp, while 10Y +1bp and 30Y -1bp. 2s10s holds at +51bp but compressed at the wings. That's a bear-flattener at the front: market pricing slightly less near-term cutting room as commodities bid and the dollar firms.

Inflation pulse: Oil at $99.44 stayed firm despite a small intraday fade, copper +1.02% to 5.98, gold flat at $4,595. With breakevens implicitly steady and crude refusing to roll over, the inflation impulse is sticky — and that's what the rotation is reading.

Risk appetite: DXY +0.10% to 98.59 — modest USD bid, not a flight. The notable tell is VIXY printing at the lows of the range with RSI deeply oversold; despite a -1% Nasdaq, vol is not bidding. That argues for continued grind/rotation rather than capitulation.

Equity regime: Cleanest rotation print of the week: small caps (-1.15%) underperforming defensives, growth ceding to value/yield, AI leadership taking its first real body-blow ahead of Microsoft/Alphabet/Meta/Amazon prints. Watch whether dip-buyers show up Wednesday.

Global: USD/JPY pinned at 159.59, USD/CNY +0.21% to 6.84, EUR/USD flat at 1.17 — FX quiet. The macro action is in commodities and U.S. equity internals.

The weight of evidence points to Stagflation — sticky commodities, defensive leadership, front-end yields up, and the AI engine wobbling on monetization doubts.