Goldilocks holds — the reflation overlay is fading.

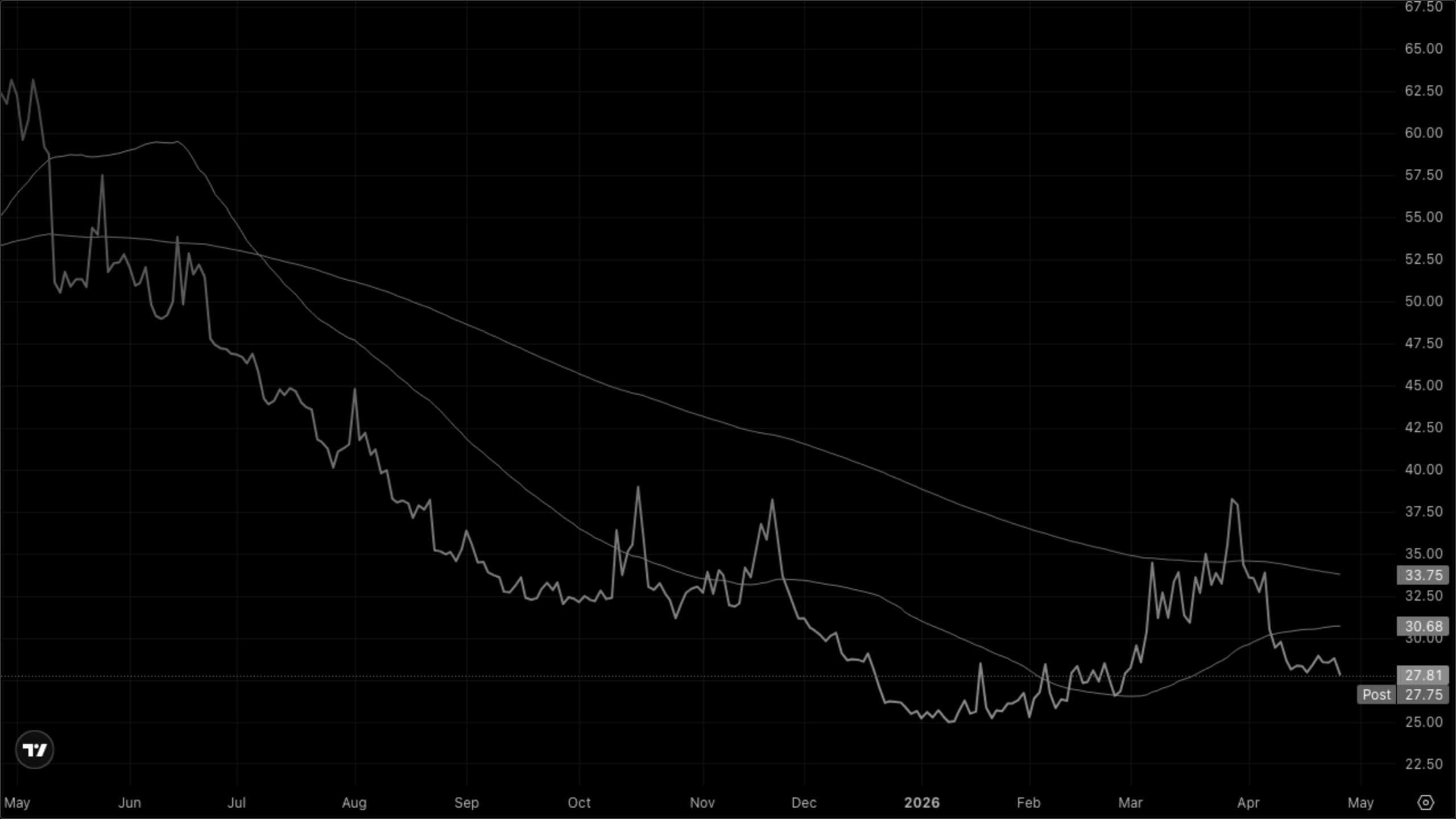

The midday call was Goldilocks with a reflation tilt; the afternoon tape is dialing the reflation piece back. WTI has rolled from +1.36% to -0.18% ($96.50) as the morning's Iran/Hormuz risk premium bleeds out of the print. Long-end yields haven't budged from the midday read — 10Y still 4.34% (+3bp), 30Y 4.95% (+3bp) — but the marginal driver has shifted from a bear-steepener narrative to mechanical pre-FOMC positioning. Vol keeps melting (VIX -3.64% to 18.02), tech and comms are firm, and defensives are being sold harder than at lunch (XLP -1.07%, XLV -0.50%). The weight of evidence still points to growth + disinflation, just without the energy bid that made midday look reflationary.

Cross-Asset Narrative

Rates & curve. No new information versus midday — 10Y still 4.34% (+3bp), 30Y still 4.95% (+3bp), 2s10s holds at +54bp. The bear-steepener that drove the financials bid earlier is quiet into the close as positioning compresses ahead of tomorrow's FOMC kickoff.

Inflation pulse. The reflationary signal that defined midday is unwinding. WTI has rolled -0.18% to $96.50 from a +1.36% midday print, gold has flipped back to +0.12% ($4,687.83), and silver is firm at +0.53%. Copper unchanged. The energy/precious-metals tape is no longer pulling in the same direction.

Risk appetite. Vol crush extended — VIX -3.64% to 18.02, VIXY -3.34%. DXY anchored at 98.50. With both vol and the dollar offered, the path of least resistance for risk assets remains higher into the Fed.

Equity regime. Defensives (XLP, XLV, XLY) are being sold harder than at midday while Goldilocks (XLK, XLC) holds — leadership remains pro-cyclical-growth, not pro-defensive. Russell 2000 +0.04% essentially flat; large-cap growth is still the engine.

The weight of evidence points to Goldilocks, with the morning's reflation overlay fading as oil unwinds.