SPX and NDX are printing fresh record highs into the close, but the surface-level strength masks a narrow tape: semis and mega-cap tech are doing all the heavy lifting, while defensives, industrials, financials and comms trade red. Yields are softer, WTI is down sharply, and VIX is back in front of an 18-handle — the disinflation + easy-money backdrop remains intact, which is why Goldilocks still wins even with breadth this thin. The risk is that if tech stalls, there's nothing behind it to hold the index up.

TL;DR

🔥 NDX +1.95% to 27,303.67, fresh ATH — Intel's blowout Q1 ($13.6B revenue vs $12.3B est, EPS $0.29 vs $0.01 est) has driven a semi-led melt-up into the close.

📈 SPX +0.80% to 7,165.07, SPY +0.77% to 713.94 — records, but Dow down 0.16% to 49,230 tells you how narrow this move is.

🛢️ WTI -2.19% to $94.87 — EIA surprise build + OPEC+ signaling +206k bpd for May is overpowering the Middle East bid.

🧊 VIX -3.11% to 18.70, 10Y yield -2bp to 4.31%, 5Y -3bp to 3.92% — classic risk-on/disinflation combo into the weekend.

🏥 XLV -1.41%, XLC -1.58%, XLI -0.92%, XLF -0.73% — the "everything except tech" tape. Nine of eleven sectors negative intraday highs despite the index prints.

Watchlist

Economic Calendar

Market News

Intel (INTC) Q1 blowout is the story of the session. Revenue $13.6B vs $12.3B consensus; adjusted EPS $0.29 vs $0.01 expected — a ~2,800% surprise. Data Center & AI revenue +22% to $5.1B, Foundry +16%. Guidance set at $13.8–14.8B for Q2, well above the ~$13.1B consensus. Semis are on an 18-session winning streak; Nvidia's cap is back through $5T into the close.

Oil getting hit despite Middle East noise — last week's surprise EIA build (+1.925M bbl) and OPEC+ greenlighting a ~206kbpd May production bump have re-asserted themselves now that the immediate Strait-of-Hormuz premium is bleeding out.

Next week: mega-cap tech earnings cluster and a Fed meeting that may be Powell's last as chair — both sit directly in front of this rally.

Charts

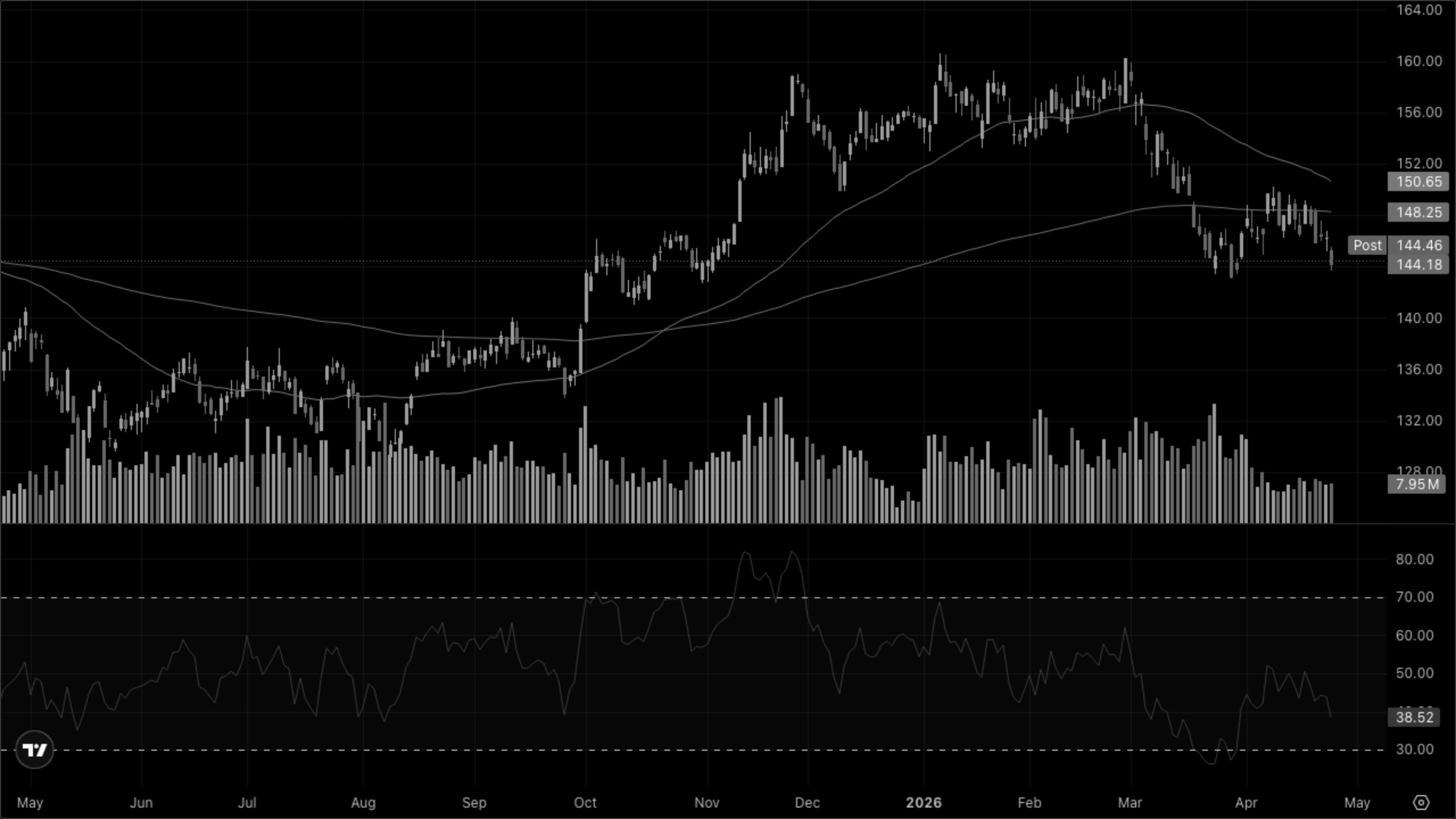

VT (Global Equity)

Clean breakout to new highs, price well above a rising SMA 50 and a well-established EMA 200; RSI ~65 — trending but not yet overbought. Volume on the breakout is steady rather than climactic.

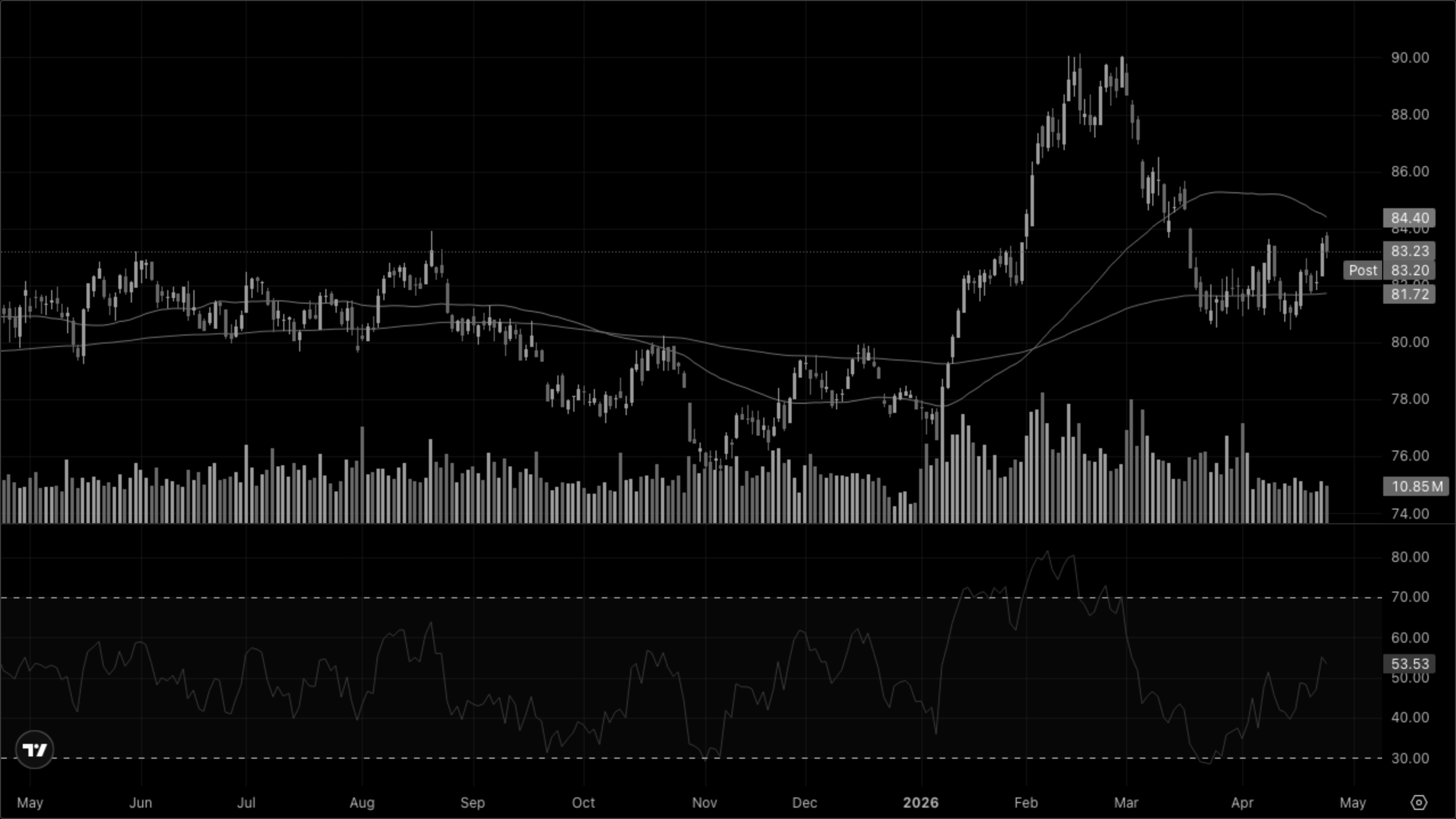

SPY (S&P 500)

Tagging a fresh all-time high after a V-recovery off the early-April shakeout; both SMA 50 and EMA 200 are curling back up and price is accelerating above them. RSI pushing ~70 — extended but not divergent yet.

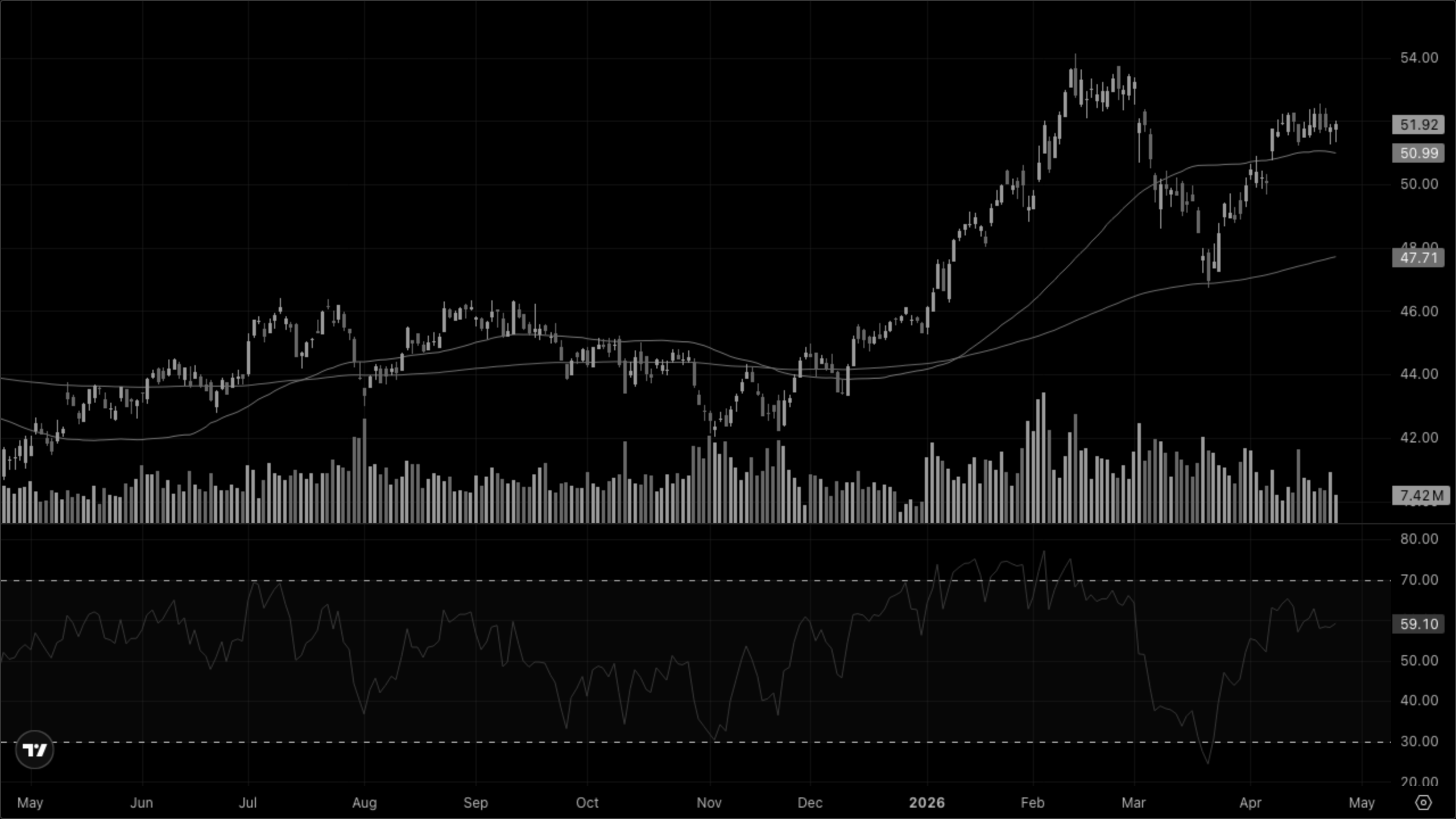

QQQ (Nasdaq-100)

The strongest chart on the board — vertical move out of the March/April base, well clear of both moving averages and riding the upper rail. RSI ~75 screams overbought; any stall here needs watching as the leadership.

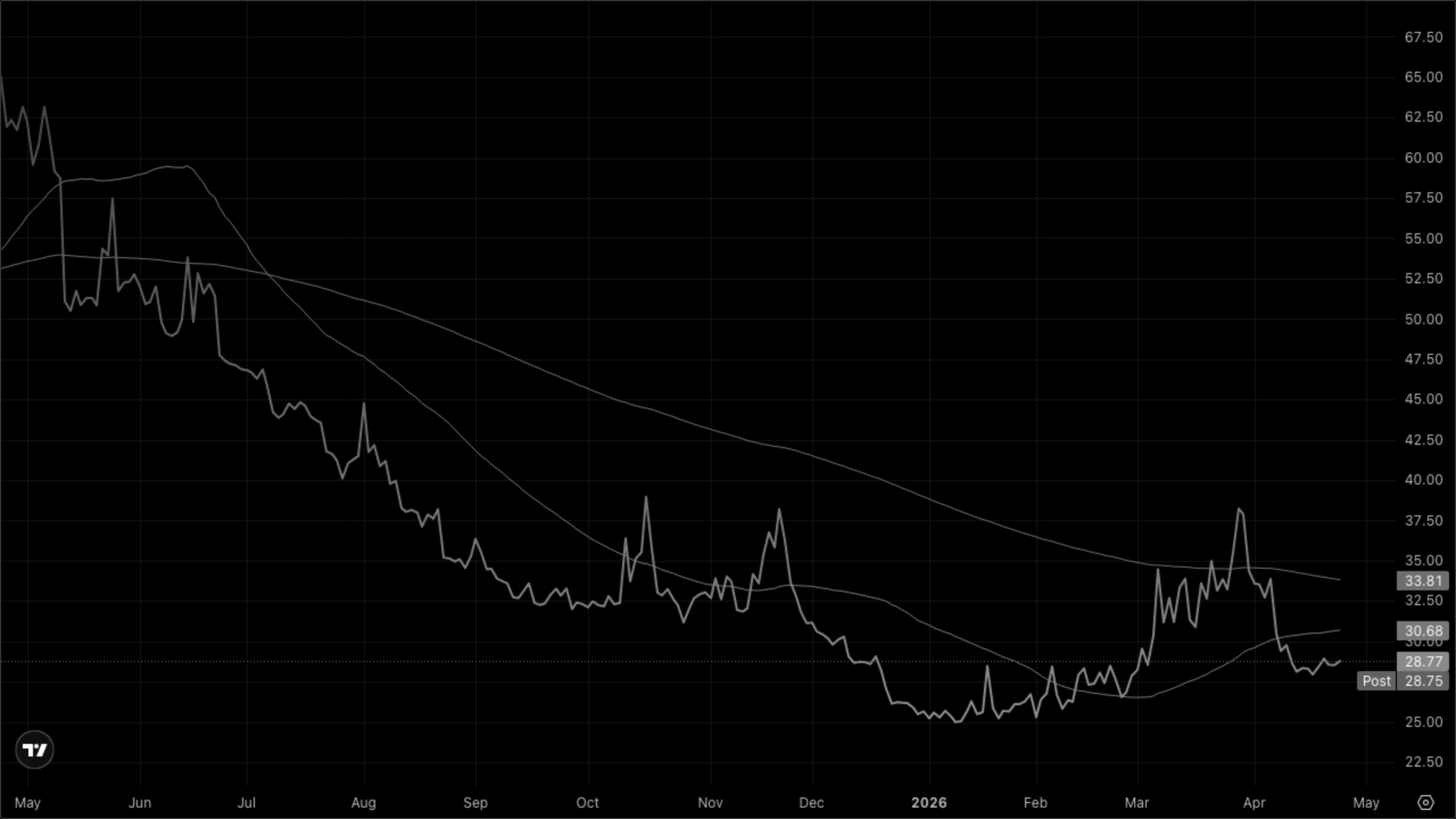

VIXY (VIX Short-Term Futures)

Volatility bleed continues — VIXY back below both SMA 50 and EMA 200 and fading the March fear spike. Structure is still a downtrend, consistent with risk-on regime but leaves little cushion if a catalyst hits.

Sector Quadrants

Goldilocks — Growth + Disinflation

Risk-on leaders when growth is strong and inflation fades

XLK — Technology

XLY — Discretionary

XLC — Comms

Reflation — Growth + Inflation

Cyclicals that benefit from rising prices and activity

XLE — Energy

XLB — Materials

XLI — Industrials

Stagflation — Contraction + Inflation

Defensives that hold up when growth stalls but prices stay hot

XLP — Staples

XLV — Health Care

XLU — Utilities

Deflation — Contraction + Disinflation

Rate-sensitive sectors that benefit from falling yields

XLRE — Real Estate

XLF — Financials

The Goldilocks quadrant is carrying the tape single-handed — XLK (implied via Intel/NVDA) and XLY +0.81% bid, but XLC -1.58% is a notable red mark inside the "winners" box. Reflation is mixed-to-soft (XLE -0.19%, XLI -0.92%, only XLB +0.21%) which is consistent with oil down and industrial demand uninspiring. Defensives are not bid (XLV -1.41%, XLP -0.30%, XLRE -0.30%) — so this is not a stealth stagflation/deflation rotation, it's just a narrow semi-led bid. That narrowness is the key risk to the Goldilocks call.

Cross-Asset Narrative

Rates & curve

5Y -3bp to 3.92%, 10Y -2bp to 4.31% — belly leading the bid, which means real yields are doing the work rather than a growth-scare bull-steepener. Consistent with disinflation getting priced in ahead of next week's Fed.

Inflation pulse

The deflationary tell of the day: WTI -2.19% to $94.87 on EIA build + OPEC+ supply. Gold essentially unchanged at $4,708 (flat is a win after recent runs), copper -0.90% to $6.03. No inflation impulse anywhere in commodities today.

Risk appetite

VIX -3.11% to 18.70, curling back below 19. EUR/USD firmer (+0.29%), USD/JPY -0.22% to 159.30 — dollar offered, risk-on. No flight-to-safety bid in gold or Treasuries beyond the mild curve bull-flattening.

Equity regime

The big tell: Russell 2000 only +0.43% while NDX is up nearly 2%. Large-cap growth dominance has reasserted hard after last week's small-cap catch-up attempt. Dow negative on an SPX record day confirms this is a cap-weight/semis story, not a participation story.

Global

USD/JPY easing back to 159.30 after pressing 160 earlier in the week — takes some pressure off the MOF and gives EM a small tailwind.

The weight of evidence points to Goldilocks — but a narrow, semi-led version that is one earnings miss or Fed surprise away from a breadth-led pullback.

What to Watch

🏦 If the Fed next week holds dovish and Powell signals the handoff cleanly, Goldilocks extends. A hawkish tilt or messy succession headline breaks the narrow tape quickly.

💾 If mega-cap tech earnings next week beat like Intel did, breadth doesn't matter. A single disappointment (MSFT/META/GOOGL) with RSI already ~75 on QQQ is the obvious risk.

📉 If 10Y breaks back above 4.40% it would pressure the rate-sensitive leg of Goldilocks (XLK multiples, XLRE). Below 4.25% and the bid in duration strengthens the disinflation call.

🛢️ If WTI loses $90 that's a clean disinflation green-light — watch XLE for the confirm/deny. A re-test of $100 on Iran headlines flips the oil story back to stagflation risk.

⚡ If VIX takes out 18.00 it signals the tape is willing to absorb more risk; a surprise spike back through 20 with breadth still this narrow is the classic turn.