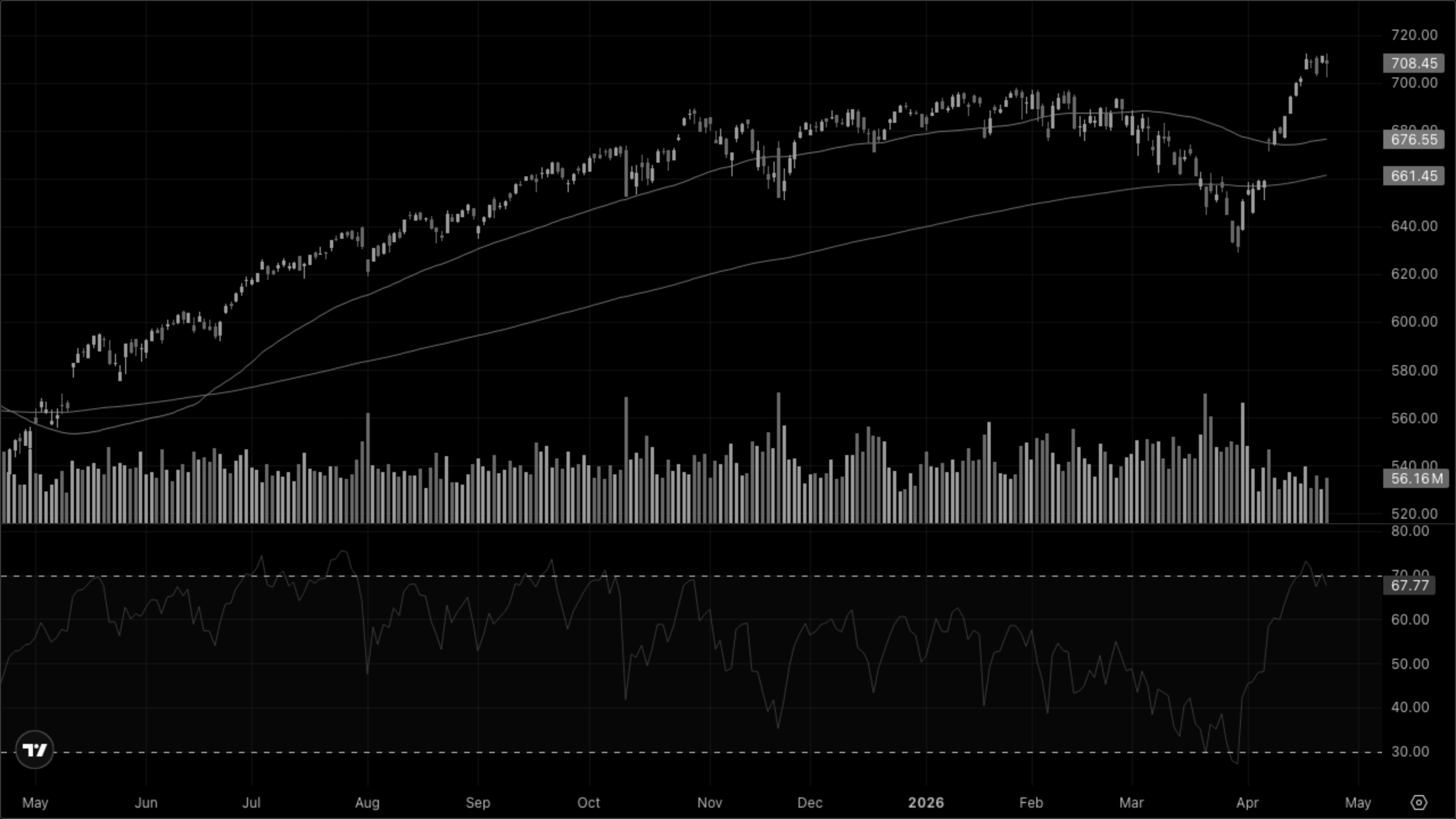

Defensive rotation deepens — growth quadrants cracking.

The tape today was a textbook defensive shuffle. Utilities (XLU +2.72%), Staples (XLP +1.67%), and Real Estate (XLRE +1.15%) led while Technology (XLK -1.42%) and Discretionary (XLY -1.00%) were dumped. That is not a Goldilocks signature. At the same time, copper fell 1.36% and gold slid 0.70%, so this was not a pure stagflation bid either — it had a distinct growth-scare flavor. The weight of evidence is shifting from "Goldilocks holds" toward a tug-of-war between stagflation (defensives bid, crude still anchored at $96.66) and deflation fear (copper dumped, growth cyclicals weak ex-XLI).

What keeps this from resolving cleanly into either bucket: industrials ripped +1.77% on a weak-tape day, the curve barely budged (2Y +1bp to 3.84%, 30Y +1bp to 4.92%), and the dollar is inert at 98.87. The bond market is not corroborating a recession scare. This looks more like a rotation out of crowded growth names into quality / income / pricing-power defensives, with the commodity complex unwinding length rather than signalling demand collapse.

Cross-Asset Narrative

Rates & curve: Essentially a non-event. 2Y held 3.84%, 30Y at 4.92%, both up a single basis point. The lack of a bid into Treasuries despite equity weakness is notable — this was an intra-equity rotation, not a macro fear event. If real recession were being priced, the long end should be catching a safe-haven bid it did not today.

Inflation pulse: Gold -0.70% to 4671.39, silver -0.76%, copper -1.36% to 6.00. Crude WTI -0.34% to 96.66 but still sitting above $96 — the inflation anchor hasn't broken. Metals taking a hit alongside the dollar drift (DXY +0.08% at 98.87) reads as position unwind more than regime repricing.

Risk appetite: VIX +2.06% to 19.30, topping 21.56 intraday before settling. VIXY was flat (-0.11%) and the long-term chart still shows a firm downtrend, so hedge demand ticked up but vol regime is unchanged. This is a "trimming exposure" session, not capitulation.

Equity regime: The headline rotation is the story. Large caps down but small caps (RUT -0.37%) not especially worse, defensives outperforming cyclicals, industrials bucking the trend. Growth-vs-value traded in favor of value intraday. Healthcare only -0.10% is telling: quality bid, speculative out.

Global: USD/JPY 159.79 inches closer to intervention zone; EUR/USD and USD/CNY essentially unchanged. No FX drama.

The weight of evidence points to a late-cycle defensive tilt straddling Stagflation and the early edge of Deflation — Goldilocks leadership has lost the bid.