Charts

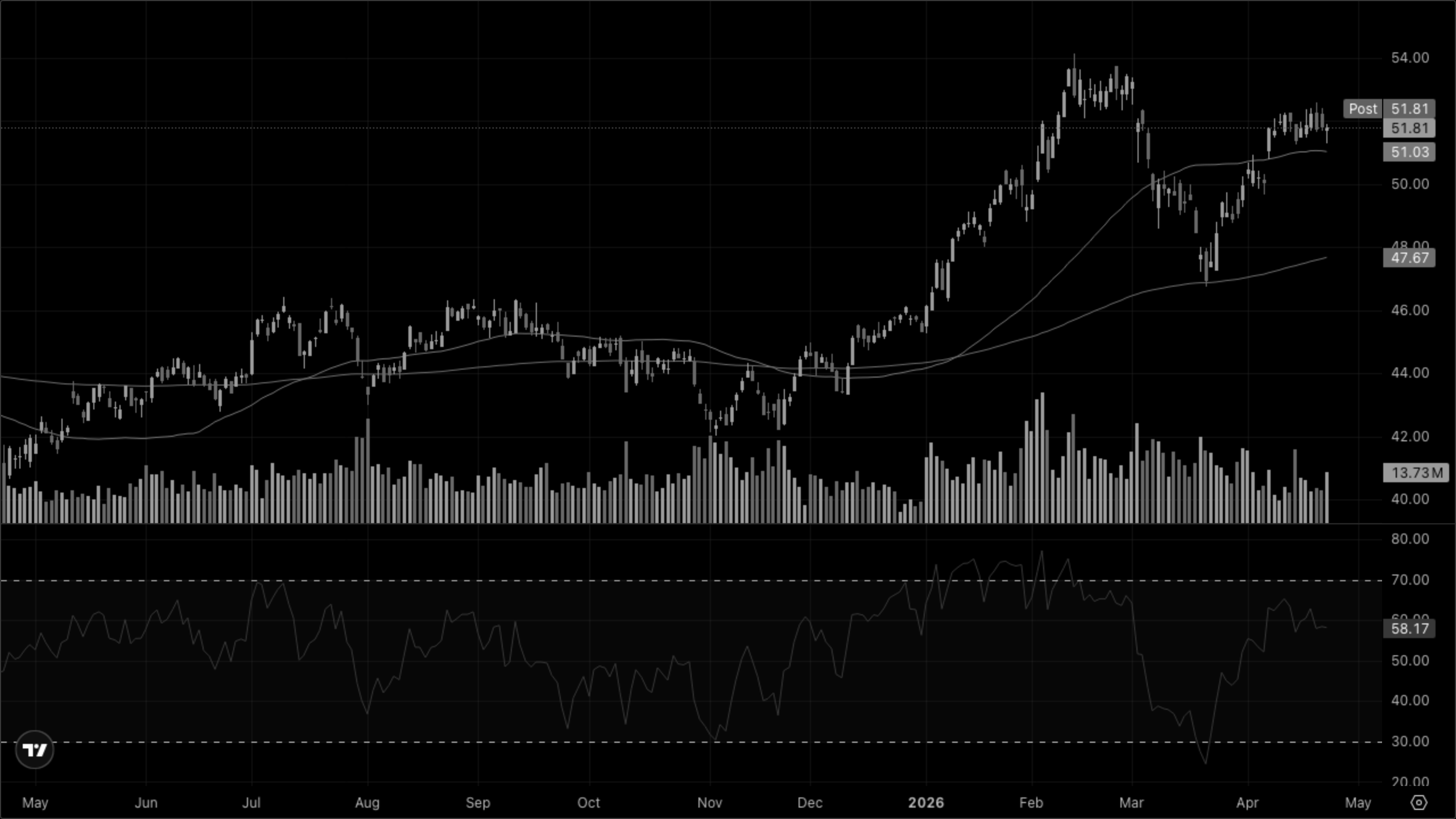

Holding well above SMA 50 and EMA 200, uptrend intact with a modest pullback from recent highs. RSI neutral-to-firm near 62, volume steady — consolidation, not distribution.

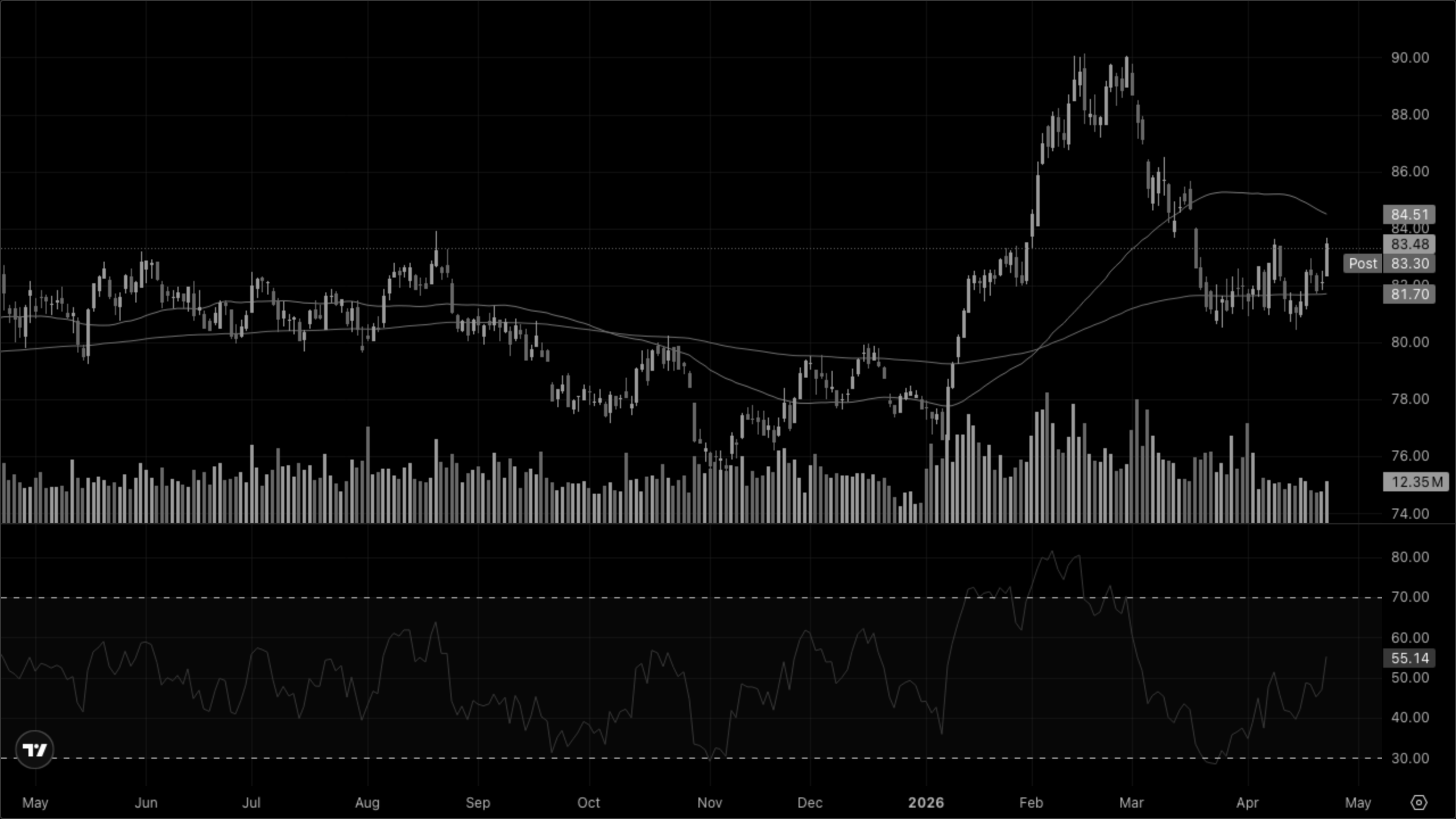

Recently printed a fresh all-time high and is digesting — still well above SMA 50 and EMA 200, with a wide gap between the two moving averages signaling a strong trend. RSI around 67 is near the overbought zone; volume unremarkable today.

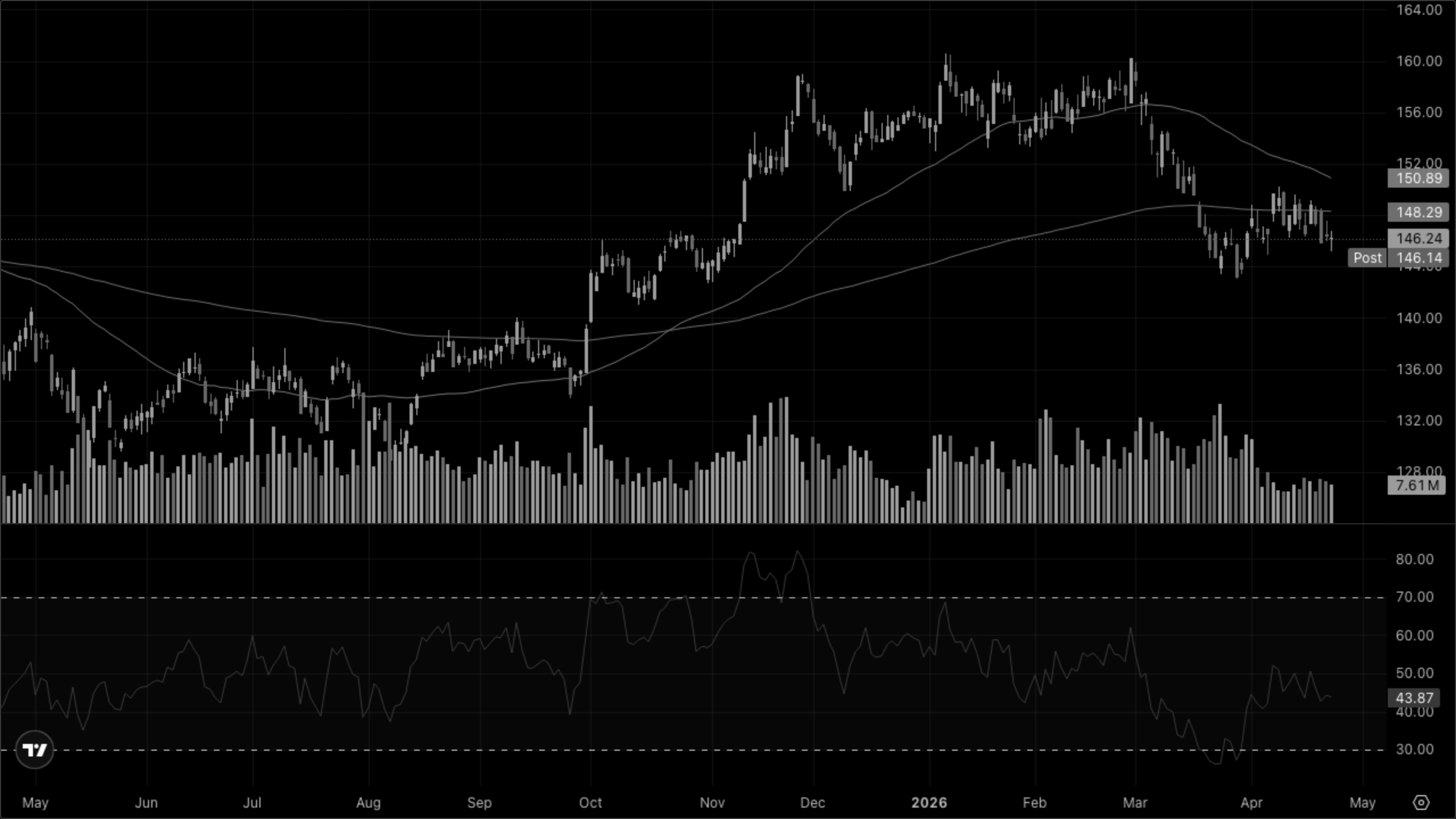

Trading above both SMA 50 and EMA 200 after a sharp April rally off the March low, but today's candle shows a clear pullback from highs. RSI near 71 flags stretched conditions — a logical spot for tech to cool on soft software earnings.

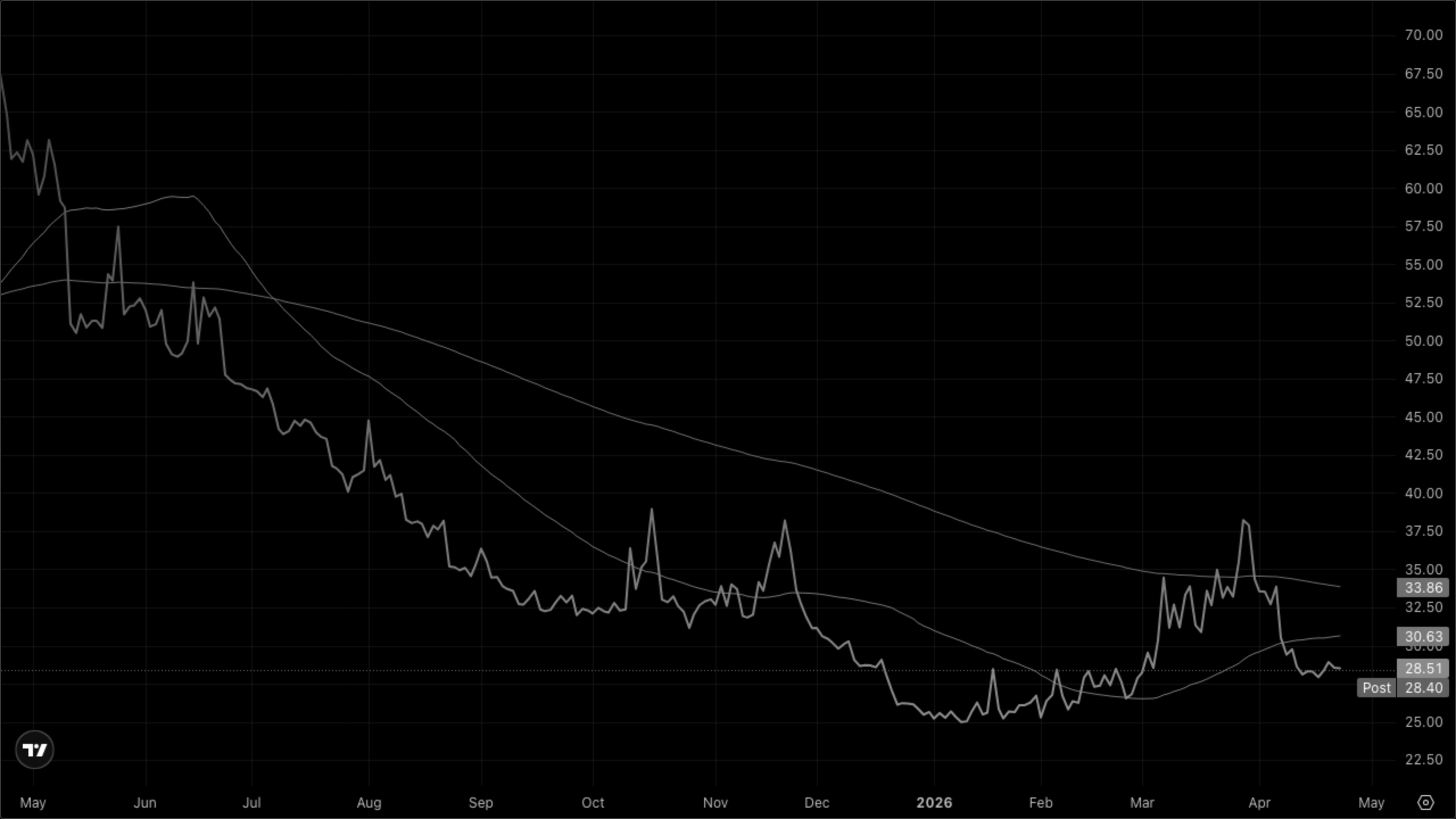

Coiled near lows with price hugging SMA 50 from below and the EMA 200 sloping down overhead. Equity weakness hasn't pushed vol higher today — orderly rotation, not a fear event.