Goldilocks holds — but oil is the swing factor.

Tech led the tape to fresh record closes on the Nasdaq 100 and SPY, VIX fell back into the mid-18s, and Treasury yields barely budged across the curve. That is the textbook Goldilocks setup: growth signal from equities, disinflation signal from the belly, risk-on from vol. The catch is WTI crude pushing up to $94.45 on renewed Strait of Hormuz disruption even after the Iran ceasefire was extended — a supply-driven energy tax that does not show up in today's equity print but sits on tomorrow's CPI and margin math. Gold and silver gave back on the ceasefire headline, but oil did not. That divergence is the tell.

Copper at 6.03 slipped another 1.5% while equities ripped, keeping the copper/gold ratio pinned near cycle lows (~0.00128) — a quiet deflationary cross-current underneath the Goldilocks tape. Rate-sensitives (XLRE -0.73%, XLF -0.17%) lagged even as yields held. Translation: today was a tech-concentrated rally riding Tesla's post-close beat and a benign yield backdrop, not a broad cyclical thrust. The regime call is intact, but the breadth is thinner than the headline suggests.

Cross-Asset Narrative

Rates & Curve. The curve barely moved: 2Y at 3.81%, 10Y at 4.32%, 30Y at 4.92%, 2s10s holding +51bp. A benign bond tape let equities do the work. Intraday ranges on yields were single basis points — this was not a rates-driven story.

Inflation pulse. Mixed. WTI at $94.45 (+1.71%) is the inflation worry — tied to Strait of Hormuz shipping disruption despite the extended Iran ceasefire. Gold gave back -0.88% to 4702 and silver -2.14%; the safe-haven bid is unwinding while the supply-driven oil bid is not. Breakevens not in the snapshot but the combination is classically ambiguous.

Risk appetite. Clean risk-on. VIX -2.98% to 18.91, back below the 20 handle. DXY flat at 98.70 — no safe-haven dollar bid. USD/JPY at 159.54 holds the carry-trade regime intact.

Equity regime. Growth over value. XLK +2.20% vs flat-to-red defensives and financials. Russell +0.74% underperformed QQQ by ~100bp — small caps participated but did not lead. This is mega-cap tech leadership, not a broadening.

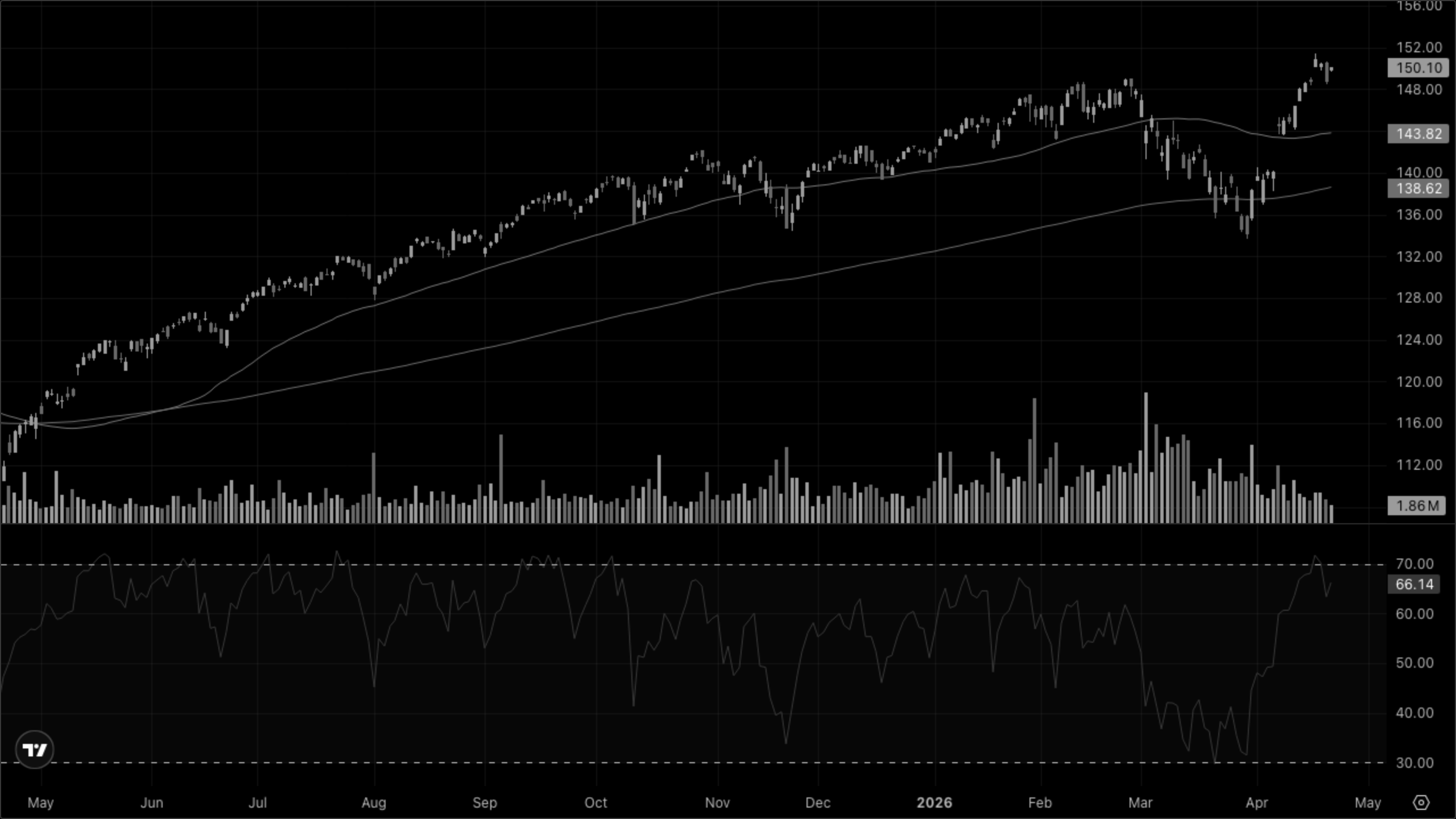

Global. USD/CNY at 6.83 (+0.07%) and EUR/USD at 1.17 (-0.07%) are sleepy. VT at 150.10 (+0.90%) participated but lagged SPY — US tech is still the concentration.

The weight of evidence points to Goldilocks, with oil as the stagflation tail risk to watch.