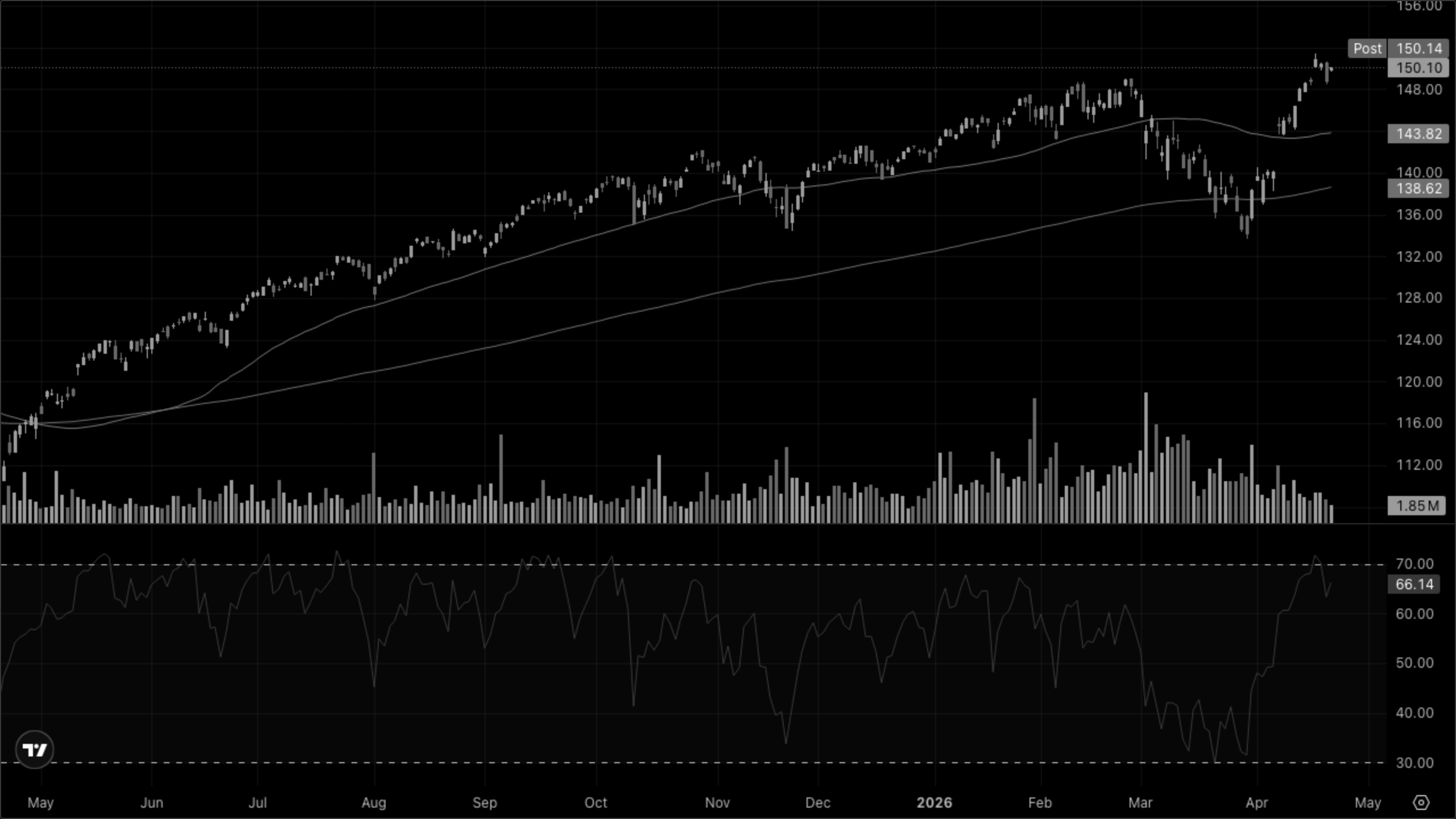

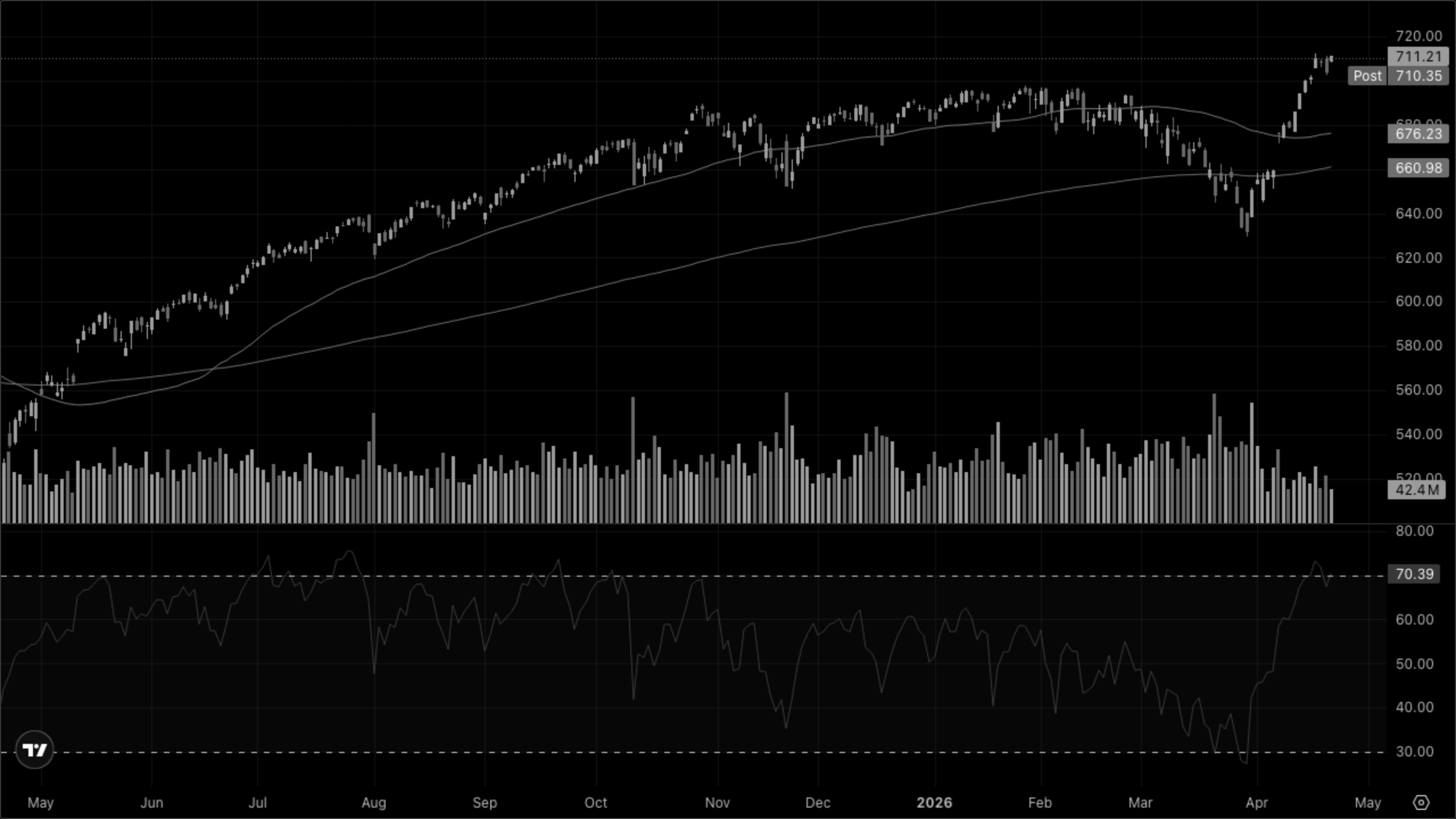

Goldilocks holds — records on tech, vol bleeding lower.

Indices closed at fresh highs as the U.S.–Iran ceasefire extension removed the last geopolitical overhang and semis carried the tape. Tech and discretionary led, defensives lagged, and the dollar firmed without yields blowing out — the textbook signature of growth-on, inflation-contained. Earnings season is reinforcing the bid: per Yahoo, >80% of S&P 500 reporters have beaten so far, with GE Vernova +8% on data-center power demand and Boeing +5.5% on a smaller-than-expected Q1 loss.

Market News

Today's tape was driven by two threads: an indefinite extension of the U.S.–Iran ceasefire (per Yahoo Finance and 24/7 Wall St.) which has been steadily compressing the geopolitical risk premium since Monday, and a strong run of Q1 earnings beats. GE Vernova (GEV) jumped ~8% after raising FY26 guidance on data-center power demand — a clean read-through to the AI capex / power-grid trade. Boeing +5.5% on a smaller Q1 loss. Semis led the Nasdaq's record close. Per CNBC, Treasury yields were little changed: 10Y ~4.30%, 2Y ~3.79%, 30Y ~4.90% — bonds shrugged at the equity melt-up, which is what you want to see in a Goldilocks read.

Sector Quadrants

Goldilocks — Growth + Disinflation

Risk-on leaders when growth is strong and inflation fades

XLK — Technology

XLY — Discretionary

XLC — Comms

Reflation — Growth + Inflation

Cyclicals that benefit from rising prices and activity

XLE — Energy

XLB — Materials

XLI — Industrials

Stagflation — Contraction + Inflation

Defensives that hold up when growth stalls but prices stay hot

XLP — Staples

XLV — Health Care

XLU — Utilities

Deflation — Contraction + Disinflation

Rate-sensitive sectors that benefit from falling yields

XLRE — Real Estate

XLF — Financials

The Goldilocks quadrant is unambiguously leading: XLK printed a fresh high with RSI >60 and an open gap above prior resistance, XLY reclaimed the EMA 200 in a hurry, and XLC is bouncing hard off recent lows. Reflation names (XLI, XLB) are participating but not leading. Stagflation defensives (XLP, XLU) are quiet, and XLV continues to fade below its EMA 200 — a clean confirmation that capital is not paying for safety today.

Cross-Asset Narrative

Rates & Curve. Per CNBC, the 10Y sits ~4.30% and the 2Y ~3.79% — the 2s10s stays positive at ~50bp with neither end moving today. Bonds did not flinch on the equity rip, which is the meaningful signal: there is no growth-scare bid in duration and no inflation re-acceleration premium being built in.

Inflation Pulse. Quiet. Gold -0.18% at $4,735.53 and crude -0.32% at $92.56. With the Iran ceasefire extending, the geopolitical bid in oil and gold continues to drain — supportive of the disinflation half of the Goldilocks call.

Risk Appetite. Decisively risk-on. VIX -2.98% to 18.91, VIXY -1.28%. Combined with the DXY +0.20% to 98.61, this is "dollar firm, vol soft, equities ripping" — capital is flowing into U.S. risk, not out of it.

Equity Regime. Mega-cap tech is doing the heavy lifting (NDX +1.73% vs. RUT +0.74%). Small caps participated but did not lead — a mild divergence to monitor, but not yet a breadth warning given the sector mix is still pro-cyclical.

Global. USD/JPY 159.48 essentially unchanged, EUR/USD 1.17 flat. No notable cross-currents from FX today.

The weight of evidence points to Goldilocks (Rising Growth + Falling Inflation).