Stagflation drift as oil shock bleeds into defensives.

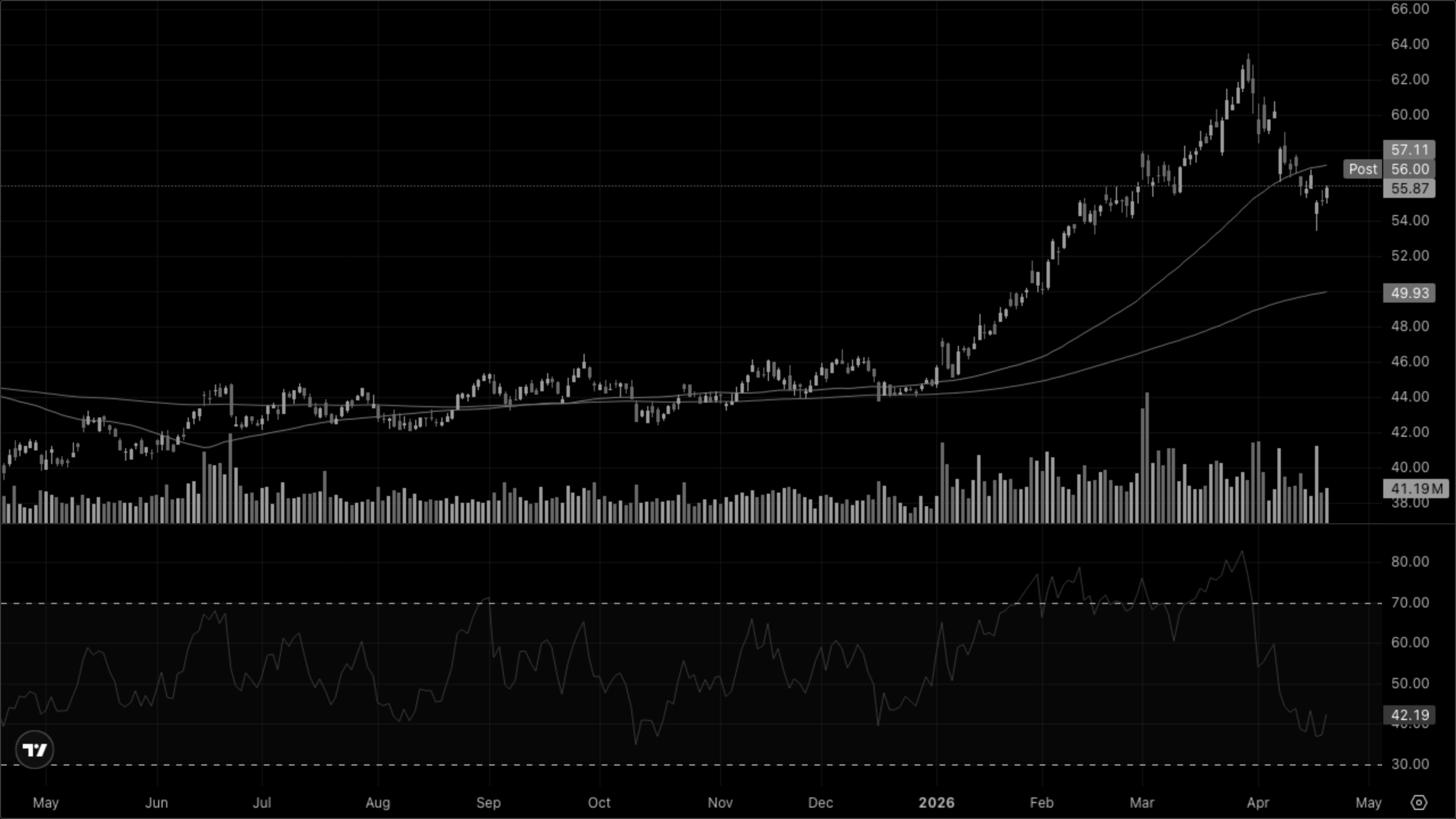

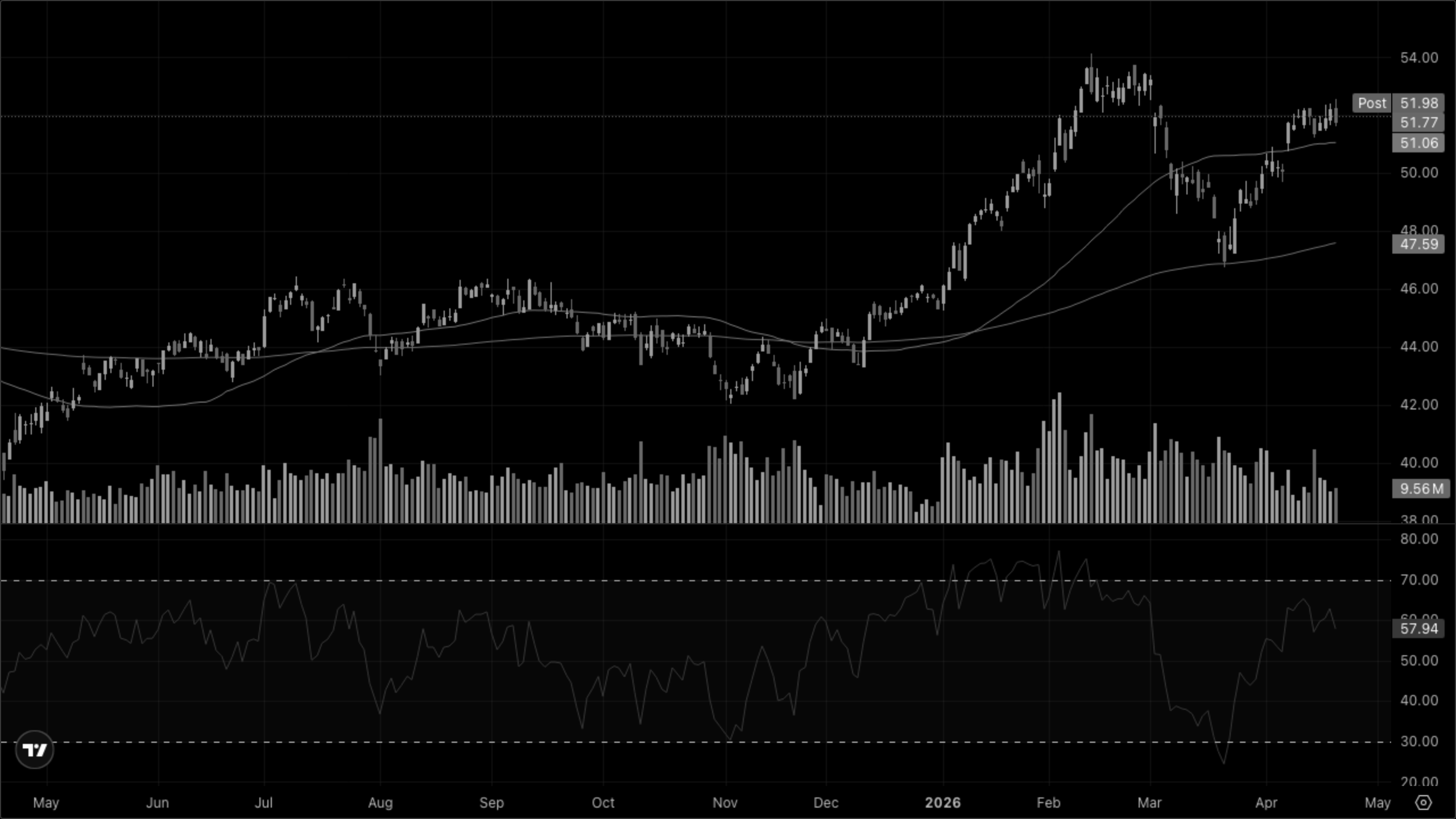

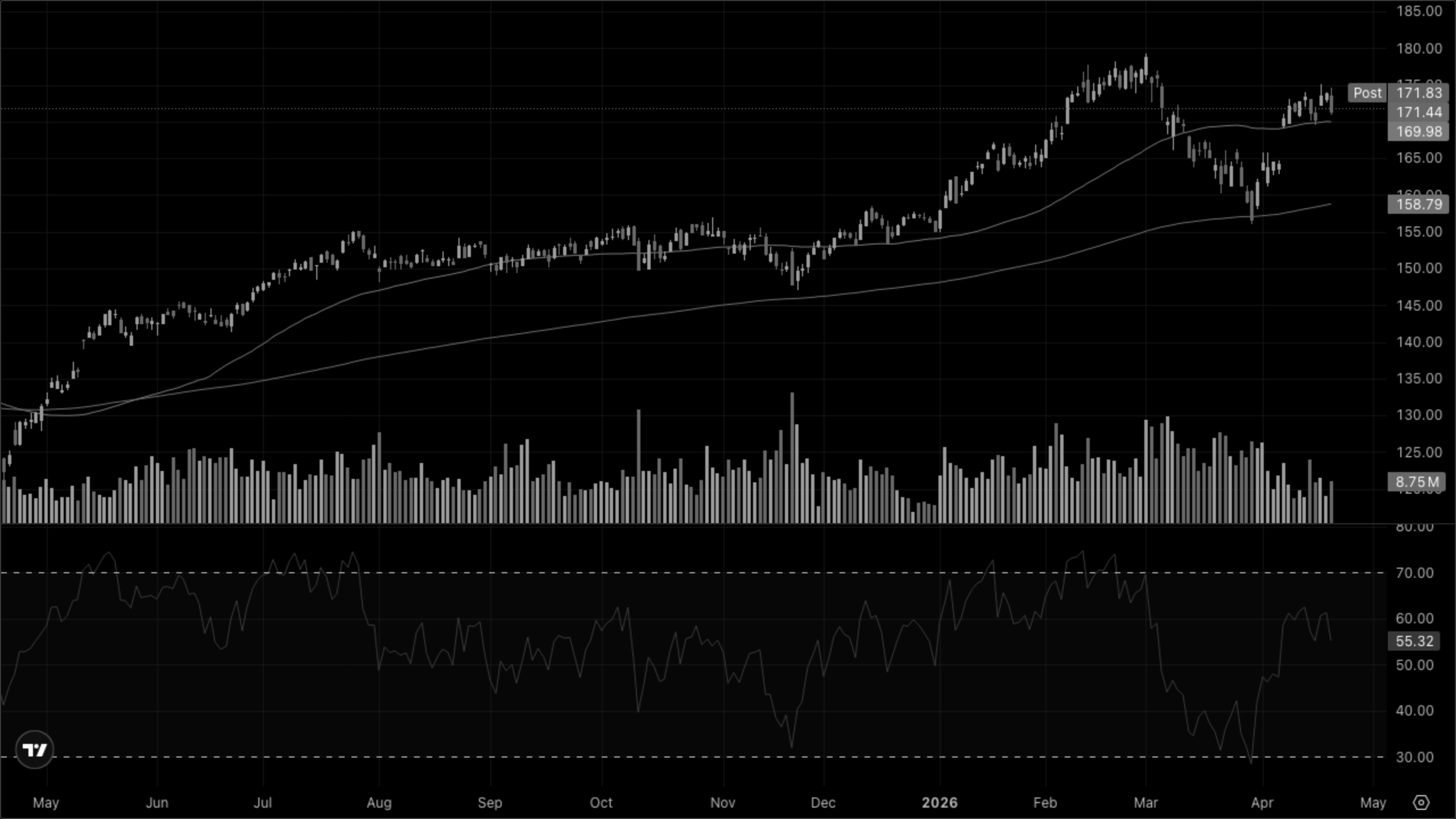

A geopolitical risk-off tape. Energy is the only sector with a real bid (XLE +1.45%) while defensives that usually absorb risk-off flows — Utilities (XLU -1.75%) and Real Estate (XLRE -1.93%) — are getting hit the hardest. That isn't a classic recession trade; it's the rate-sensitive complex buckling underneath a sticky-oil, firm-dollar backdrop. WTI sits at $90.12, gold holds $4,716, DXY pushes to 98.41, and VIXY adds nearly 2%. Cyclicals weaken alongside defensives (XLI -1.41%, XLB -0.88%), leaving only tech flat. The weight of evidence leans stagflation-adjacent with the Iran ceasefire deadline as the overnight catalyst.

Cross-Asset Narrative

Inflation pulse: Crude at $90.12 and gold at $4,716.70 — both near recent highs, neither breaking out today but refusing to give ground while the geopolitical tail stays fat. Copper $6.02, silver $76.86 — industrial metals essentially unchanged, so the bid is geopolitical, not cyclical.

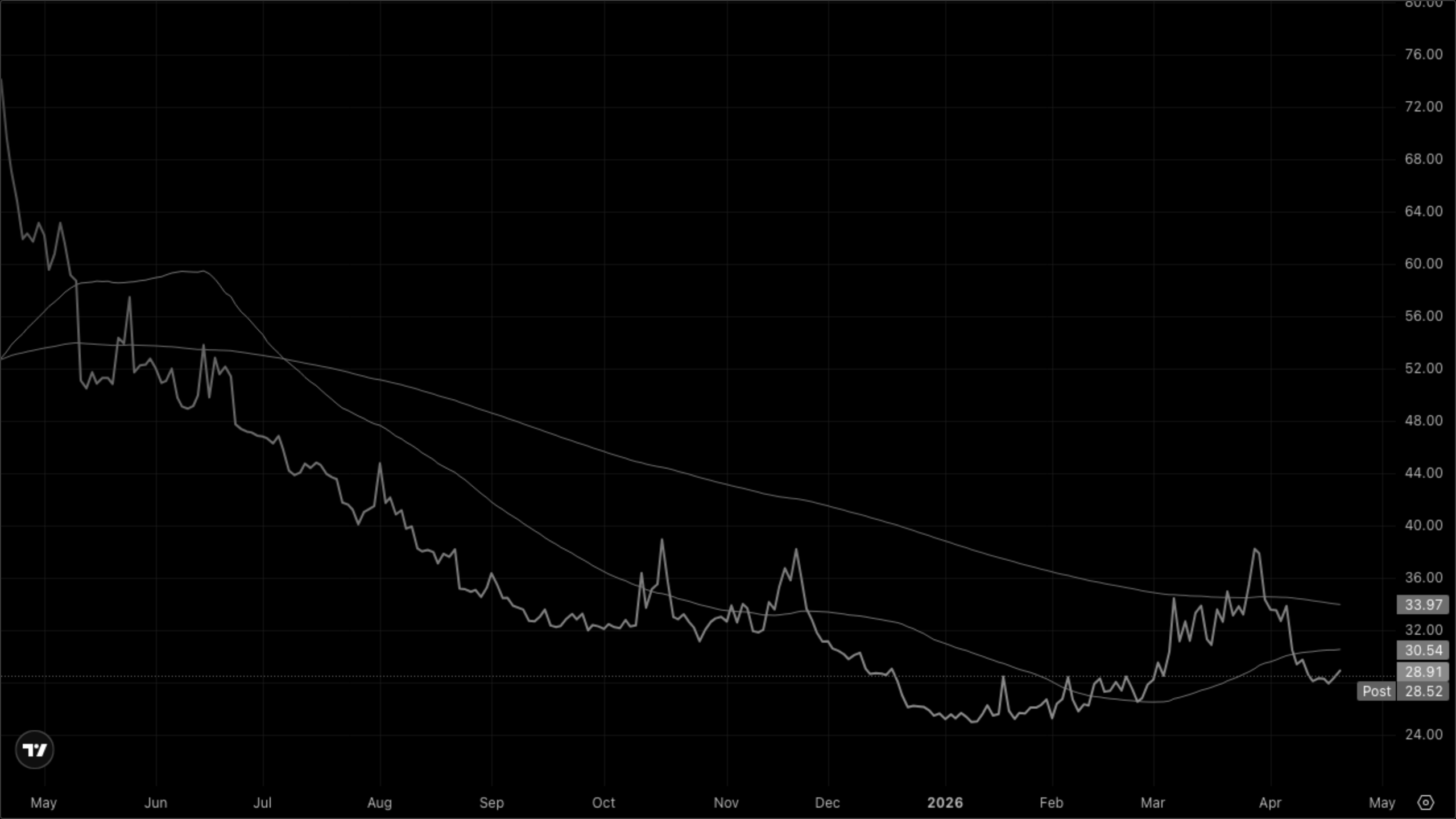

Risk appetite: VIXY +1.83% to 28.91 with DXY +0.36% to 98.41. The dollar is doing the safety work — EUR/USD sagging, USD/JPY stuck at 159.38 on an upper bound that continues to pressure the BoJ. This is a risk-off tape that favors cash-like USD over duration.

Equity regime: The rotation map is the story. Winners: Energy. Losers: Real Estate and Utilities, the two most rate-sensitive groups. That's not the stack you'd expect in a pure recession scare — it says rates are NOT rallying into the risk-off move. With Treasury yield levels not in today's snapshot, the duration proxy selloff is the cleanest tell.

Global: USD/CNY steady at 6.82, EUR/USD 1.17 — no disorderly FX move, but the dollar is grinding. Japan unchanged at the yen's pain threshold.

The weight of evidence points to stagflation-adjacent risk-off, with energy the only functional hedge on the tape.