Goldilocks holds — but oil's Sunday bid threatens the thesis.

The week ended with the S&P 500 at a record close and the Nasdaq notching its 13th straight winning session — the longest streak since 1992 — on hopes that the US–Iran ceasefire and Iran's reopening of the Strait of Hormuz to non-Iranian commercial vessels would drain the energy-driven stagflation premium out of risk assets. Equities broadened (Russell 2000 +2.11%), credit-sensitive names firmed, and gold softened. That is textbook growth-up, inflation-cooling behavior.

The asterisk is WTI's +4.23% overnight bid to 87.54 even as energy equities fell-2.76% on the Friday tape — a classic "sell the ceasefire news" in the equity complex, but a reminder that the Hormuz geopolitical premium has not fully exited the crude market. If Monday's cash session imports that bid into US equities, the Goldilocks call narrows quickly. For now, the weight of evidence — breadth, sector leadership, yield-curve steepening at +54bp, falling gold — still argues Rising Growth + Falling Inflation.

TL;DR

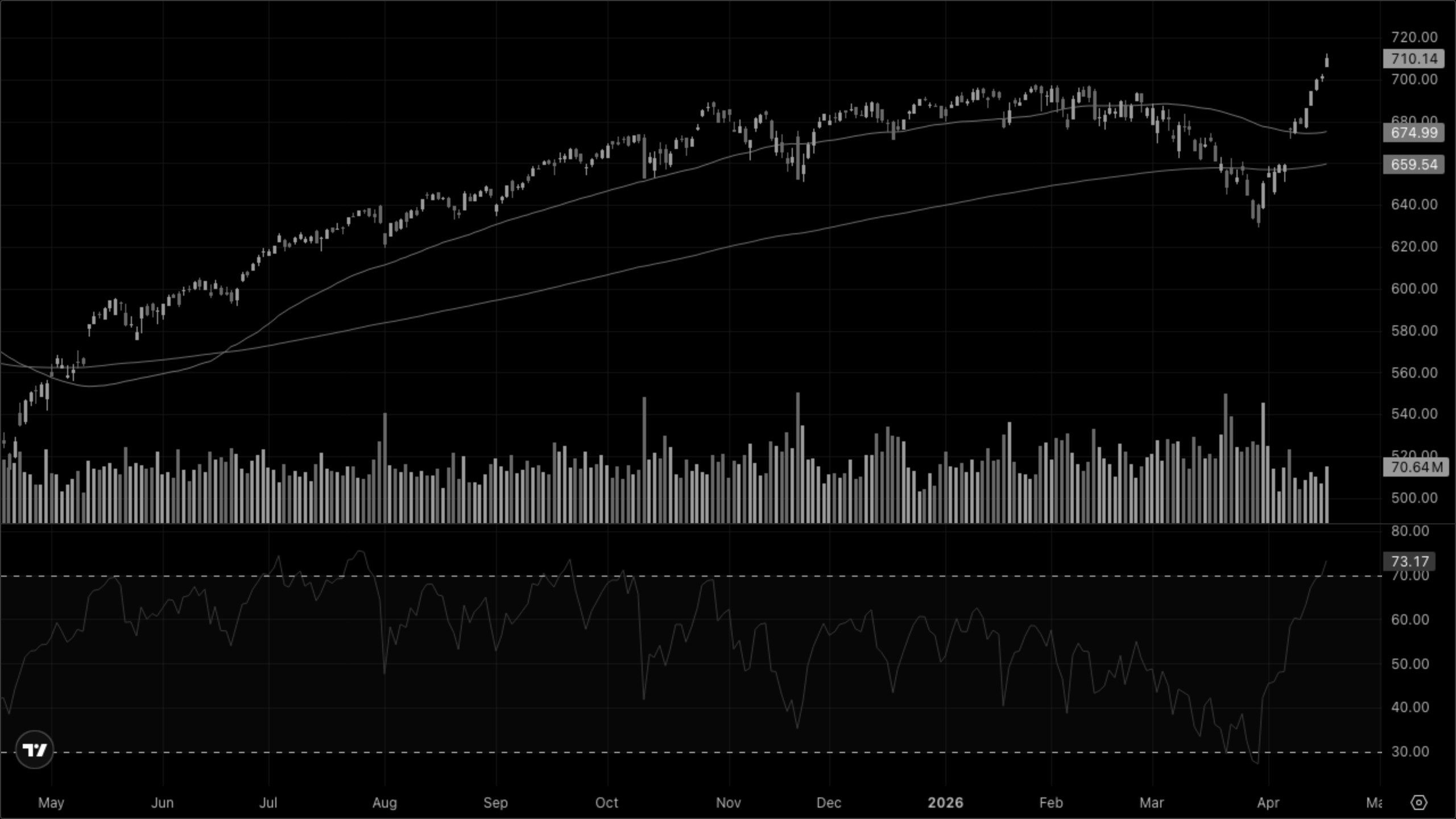

📈 SPY closed the week at 710.14 (+1.21%) — fresh record; Nasdaq's 13-day win streak is the longest since 1992.

🔥 Small caps led: IWM +2.11% and XLY +2.36% — broadening, not just mega-cap.

🛢️ WTI surged +4.23% to 87.54 on Hormuz supply risk even as XLE -2.76% — cash market faded the ceasefire.

🧊 Gold -0.90% to 4794 and silver -0.99% — defensive metals bleeding as risk appetite returns.

💵 DXY flat at 98.27; USD/JPY pushing 158.87 — BoJ intervention watch re-arming under the surface.

Since Last Update

No prior session delta block attached. Numbers above reflect session changes from the data snapshot.

Watchlist

Economic Calendar

Market News

Charts

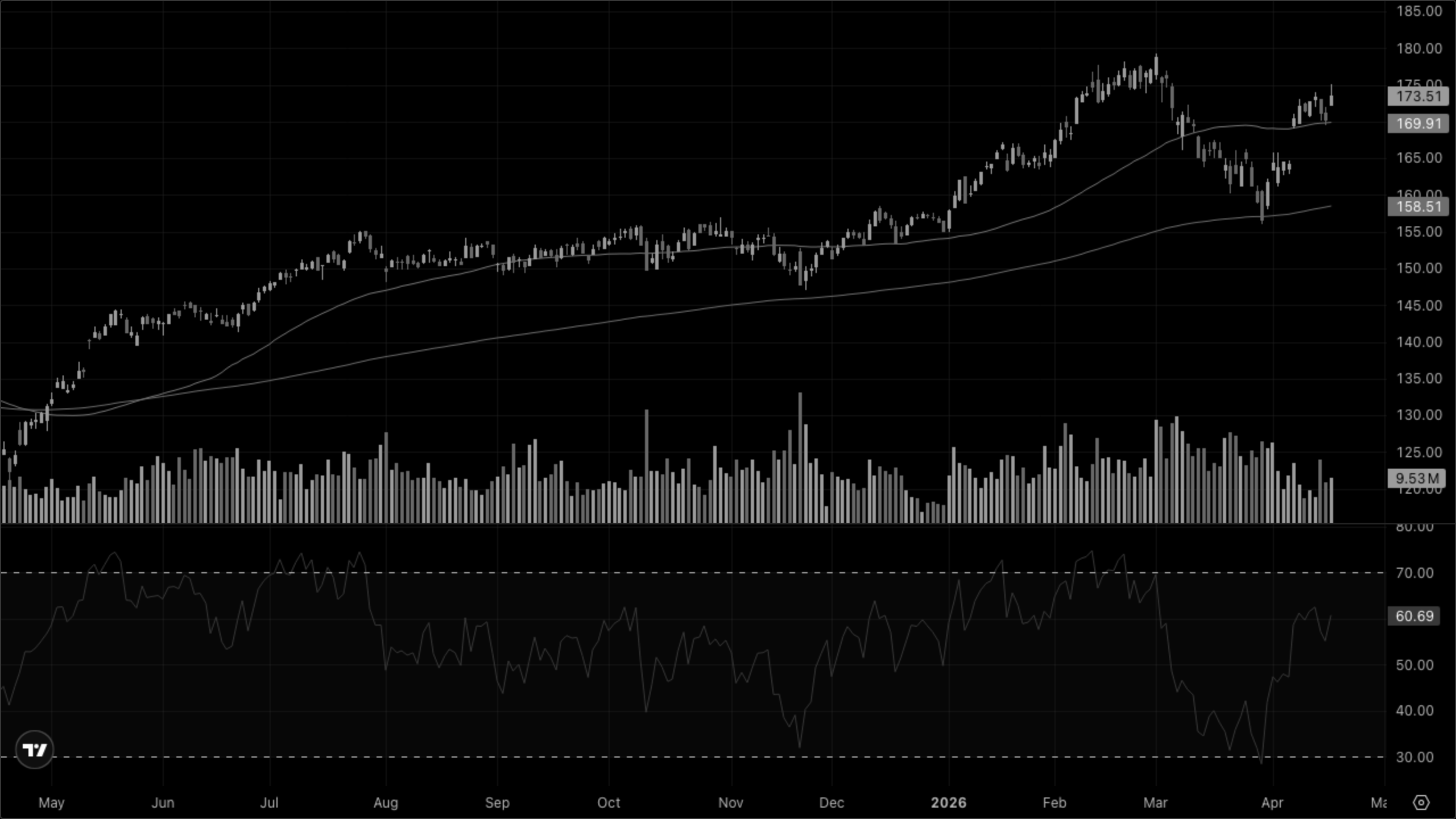

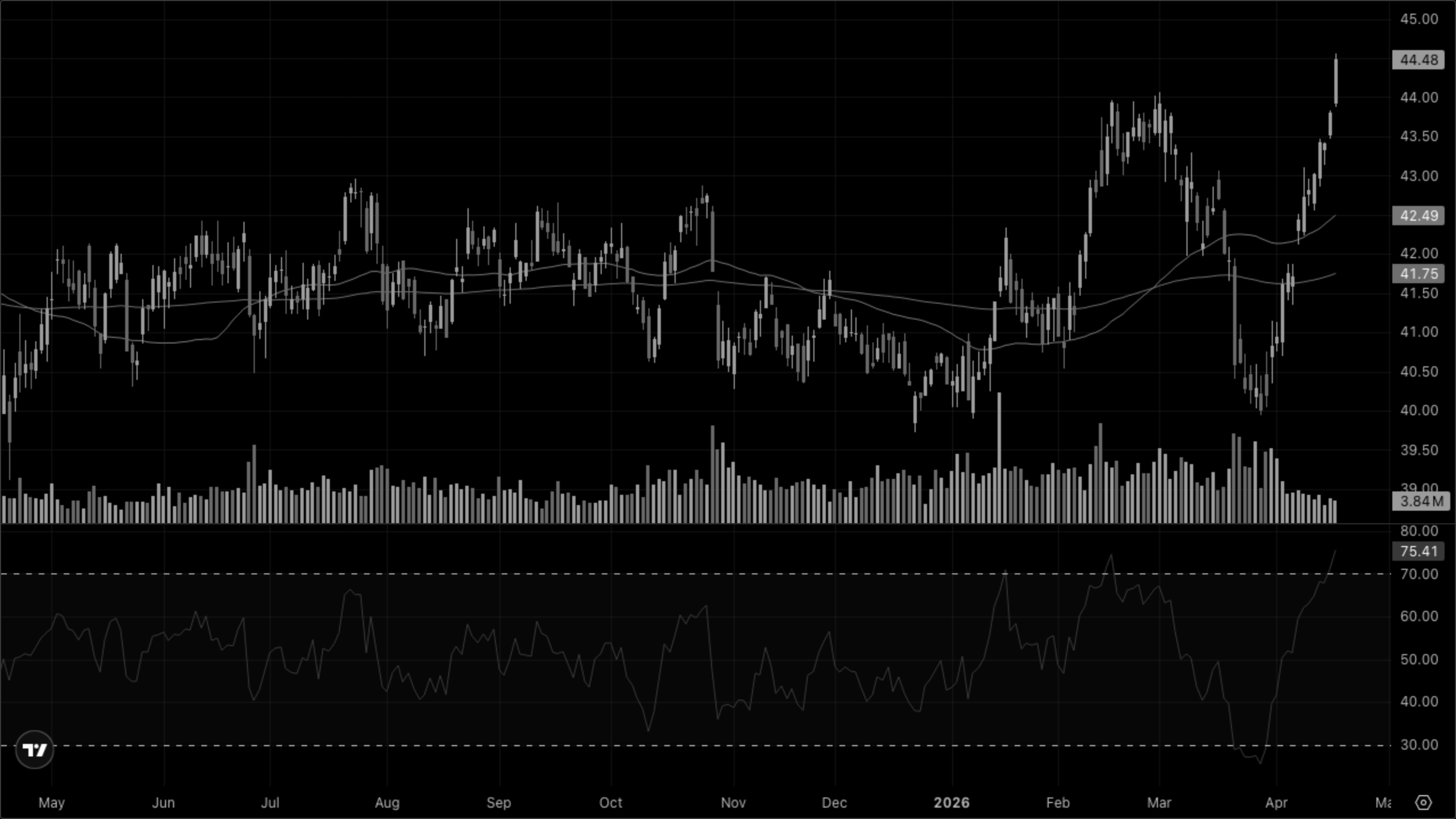

VT (Global Equity)

Breakout above the March–April consolidation with price well clear of both SMA 50 and EMA 200. RSI pushing into the low-70s signals strong momentum but extended conditions — watch for a digestion pullback to the rising SMA.

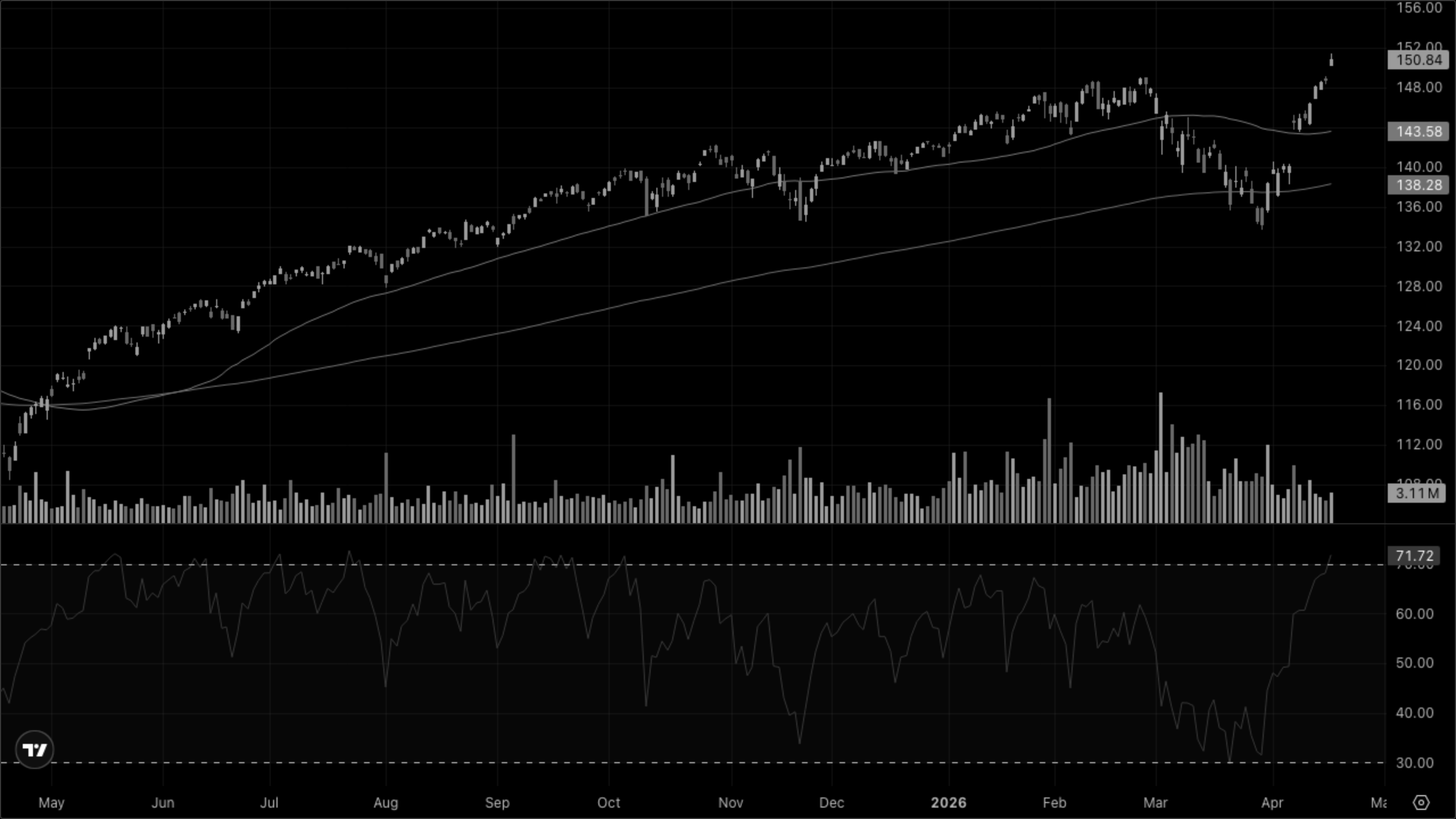

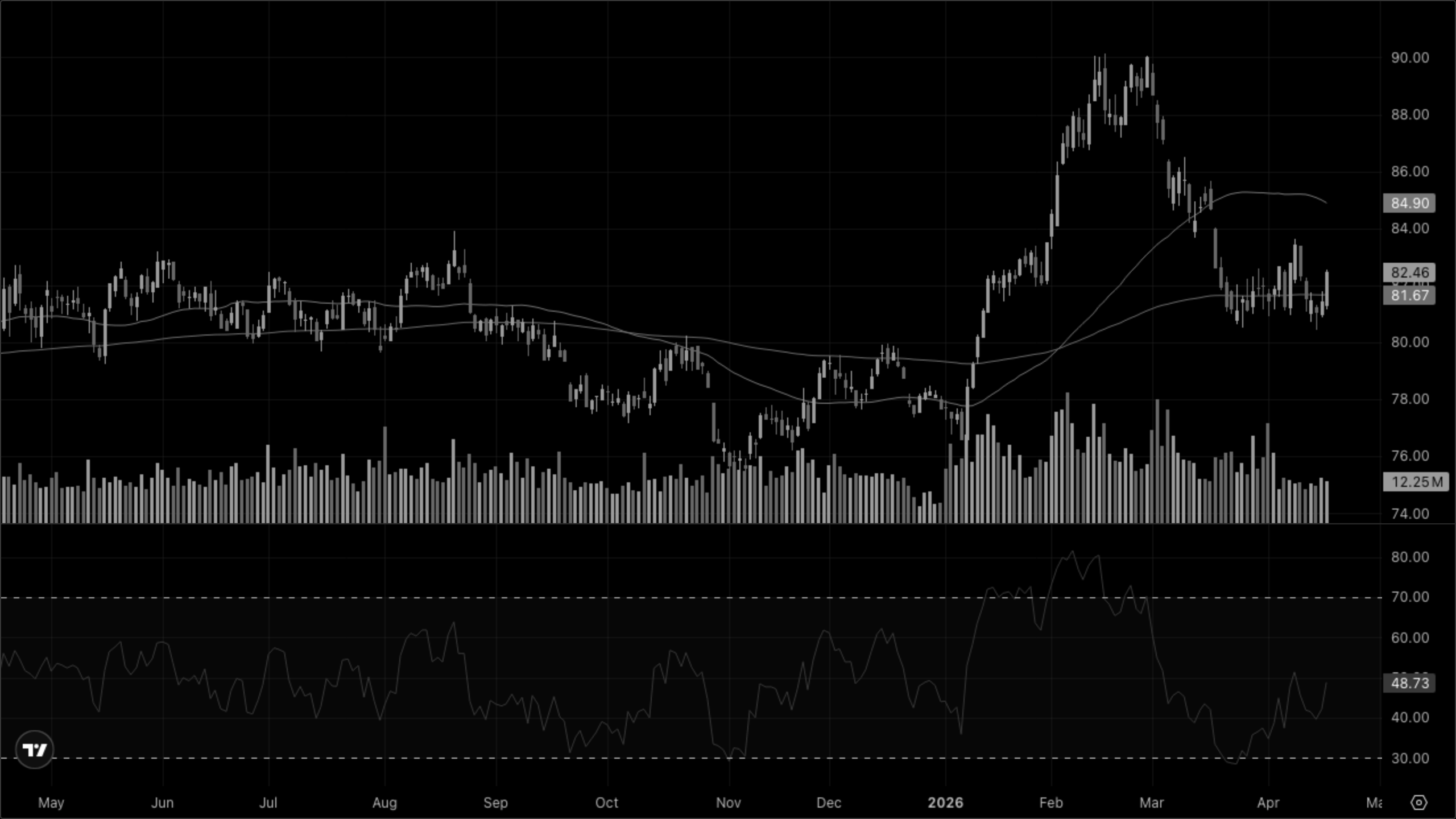

SPY (S&P 500)

Vertical thrust off the March lows with a clean breakout to new highs. RSI deep in overbought territory (~73) and volume steady — trend is unambiguous but mean-reversion risk is elevated.

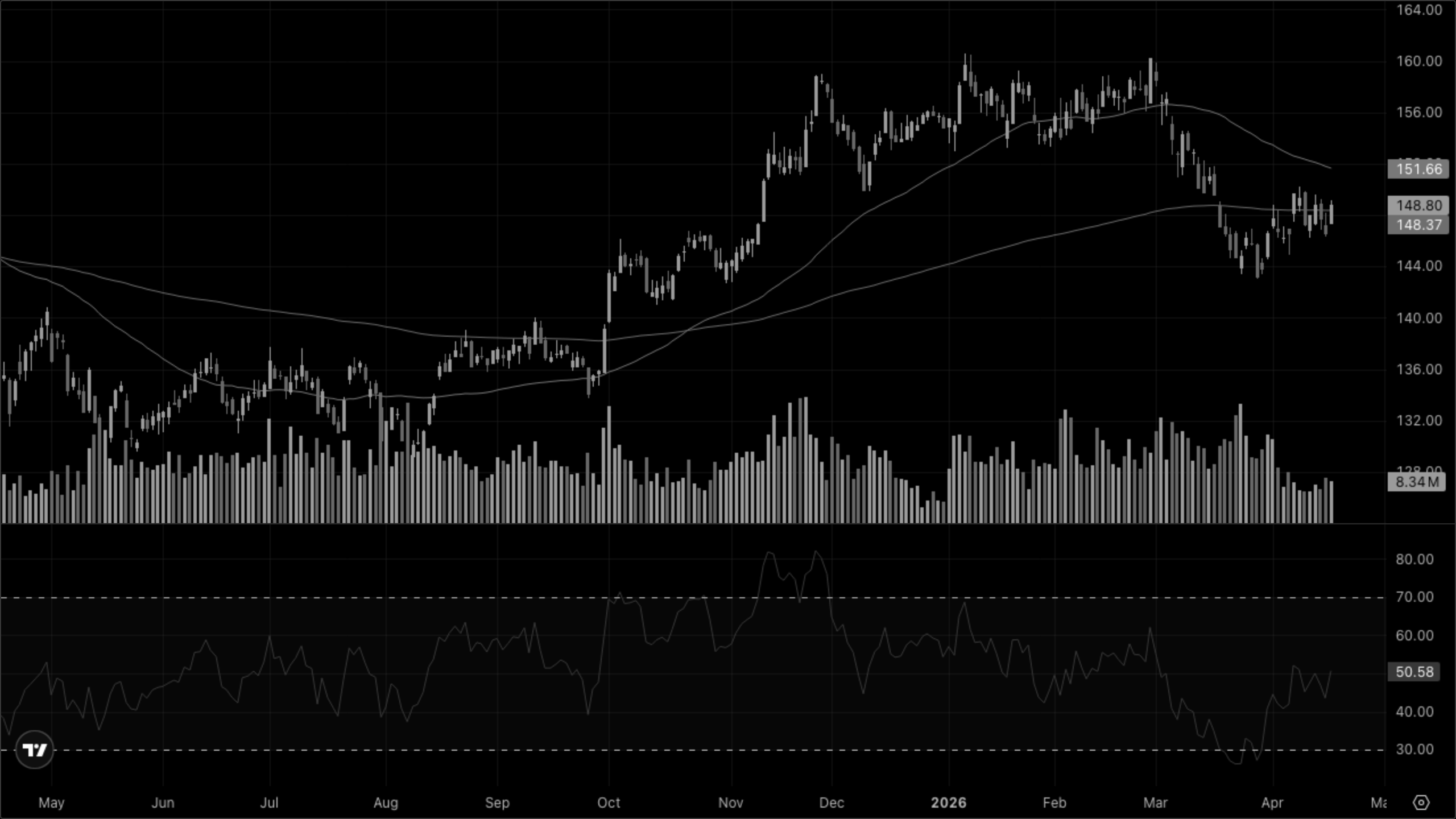

QQQ (Nasdaq-100)

Leading the complex — same breakout pattern as SPY but with more vertical separation from the SMA 50. RSI ~74, thirteen straight up days puts this in the most stretched condition of the year.

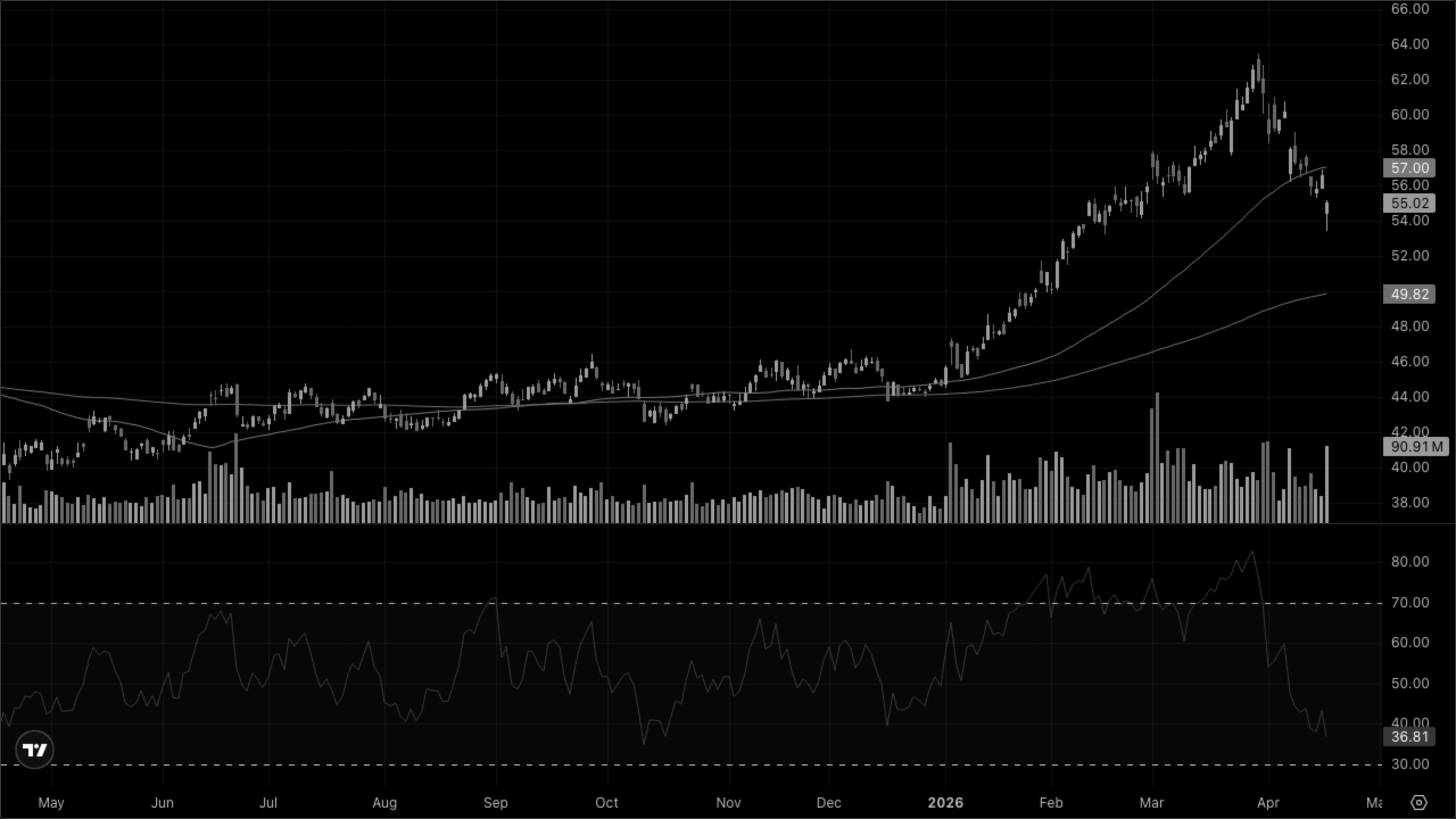

VIXY (VIX Short-Term Futures)

Downtrend fully intact — price back below the flattening SMA 50 after the March spike. Volatility compression is consistent with the Goldilocks call, but also the condition from which violent reversals originate.

Sector Quadrants

Goldilocks — Growth + Disinflation

Risk-on leaders when growth is strong and inflation fades

XLK — Technology

XLY — Discretionary

XLC — Comms

Reflation — Growth + Inflation

Cyclicals that benefit from rising prices and activity

XLE — Energy

XLB — Materials

XLI — Industrials

Stagflation — Contraction + Inflation

Defensives that hold up when growth stalls but prices stay hot

XLP — Staples

XLV — Health Care

XLU — Utilities

Deflation — Contraction + Disinflation

Rate-sensitive sectors that benefit from falling yields

XLRE — Real Estate

XLF — Financials

Leadership today came from the Goldilocks quadrant — XLY +2.36%, XLK +1.53% — alongside rate-sensitive deflation-quadrant names (XLRE +1.53%, XLF +0.77%). The reflation cohort diverged sharply: XLE -2.76% even as crude jumped, XLI firm on transport strength. Stagflation defensives were mixed with XLU -0.43%. Net read: cash equities priced in ceasefire-driven disinflation, confirming the Goldilocks call — but only if oil's overnight bid fails to carry into Monday.

Cross-Asset Narrative

Rates & Curve

The curve steepened a touch — 2Y at 3.73% (+3bp), 10Y at 4.27% (+2bp), 30Y at 4.90% — with the 2s10s spread at +54bp. Modest belly-led selling into a record equity close is a growth-confirming signal, not a stagflation one. The front end's reluctance to sell off aggressively is the tell: rate-cut pricing is intact even as risk assets party.

Inflation Pulse

Split signal. Gold -0.90% to 4794 and silver -0.99% argue the inflation premium is bleeding out of defensive metals. But WTI +4.23% to 87.54 says the Hormuz supply risk is still live — and Brent is reportedly pushing toward $98 with JPMorgan flagging $150 tail-risk scenarios if the strait doesn't reopen meaningfully. Copper -0.67% does not confirm a growth-led commodity squeeze.

Risk Appetite

Full risk-on. VIXY by visual read continues its downtrend below the falling 50-day. DXY flat at 98.27 — neither a flight-to-safety bid nor a carry-trade collapse. The tape is trusting the ceasefire.

Equity Regime

Breadth expansion is the key development: IWM +2.11% outpaced NDX +1.29%, and XLY's +2.36% suggests the rally is no longer a mega-cap-only affair. This is the kind of participation Goldilocks regimes need to sustain.

Global

VT +1.38% — global equity moving in sync with US. USD/JPY at 158.87 keeps the BoJ intervention watch warm; USD/CNY steady at 6.82.

The weight of evidence points to Goldilocks — Rising Growth + Falling Inflation — with an oil-shaped conditional attached.

What to Watch

🛢️ If WTI sustains above $90 into Monday's cash session then Goldilocks thesis cracks and stagflation risk reprices — XLE should reverse its Friday decline.

📉 If VIX stays compressed and 10Y holds below 4.35% then the bullish regime extends and breadth expansion continues; a break of 10Y above 4.40% with equities selling signals trouble.

🏦 If Waller (Bemidji), Jefferson (Detroit), or Barr (DC) strike a dovish tone this week then rate-cut pricing firms and the curve steepens further — confirming Goldilocks.

🌏 If Iran closes or restricts the Strait of Hormuz again then Brent spikes toward JPM's $150 scenario and every asset class reprices overnight — watch gold for confirmation of regime flip.

💵 If USD/JPY breaks 160 then BoJ intervention risk goes binary — sudden JPY strength would tighten global dollar liquidity and pressure US equities regardless of the domestic regime.