Sector Quadrants

Goldilocks — Growth + Disinflation

Risk-on leaders when growth is strong and inflation fades

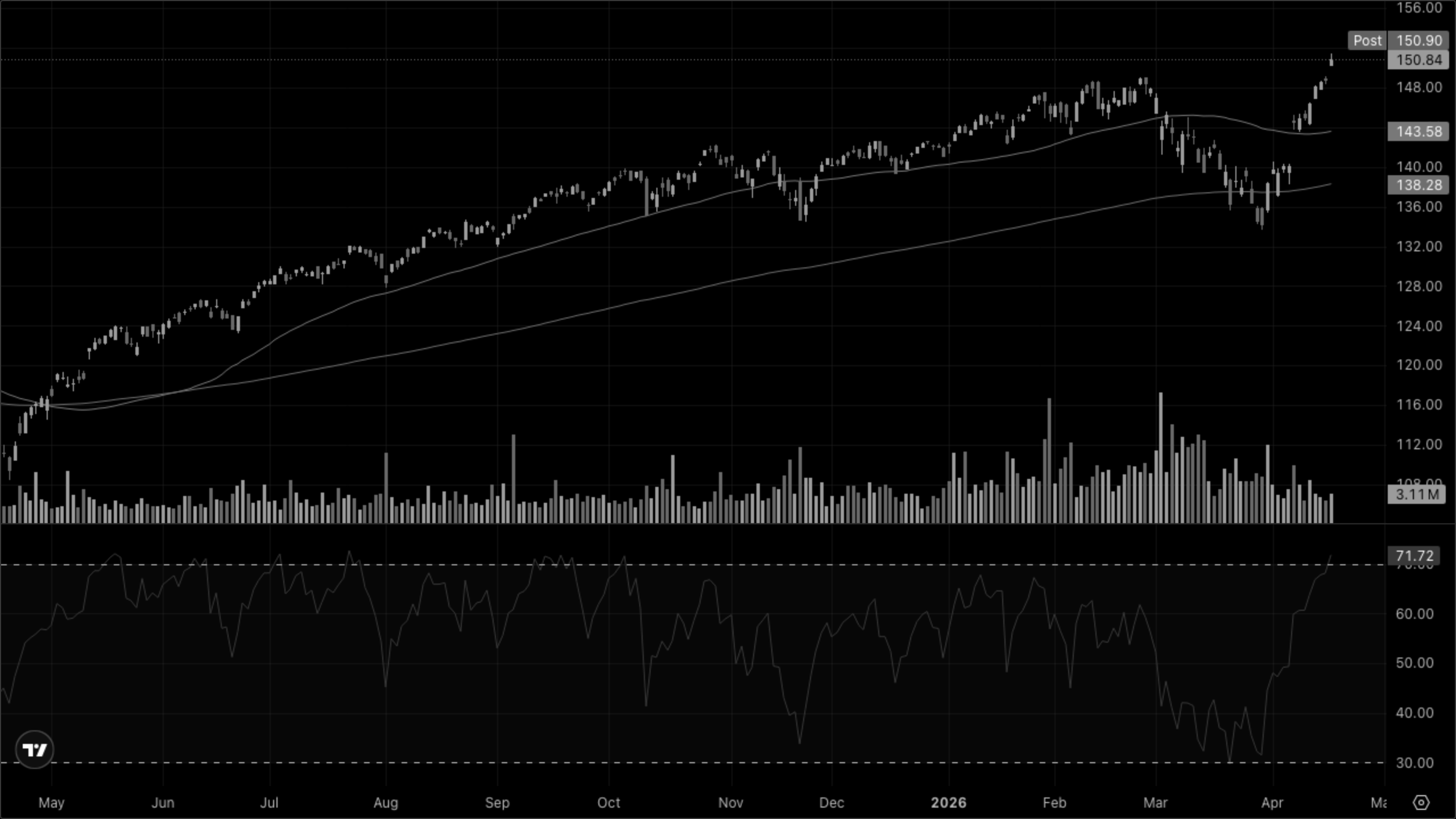

XLK — Technology

XLY — Discretionary

XLC — Comms

Reflation — Growth + Inflation

Cyclicals that benefit from rising prices and activity

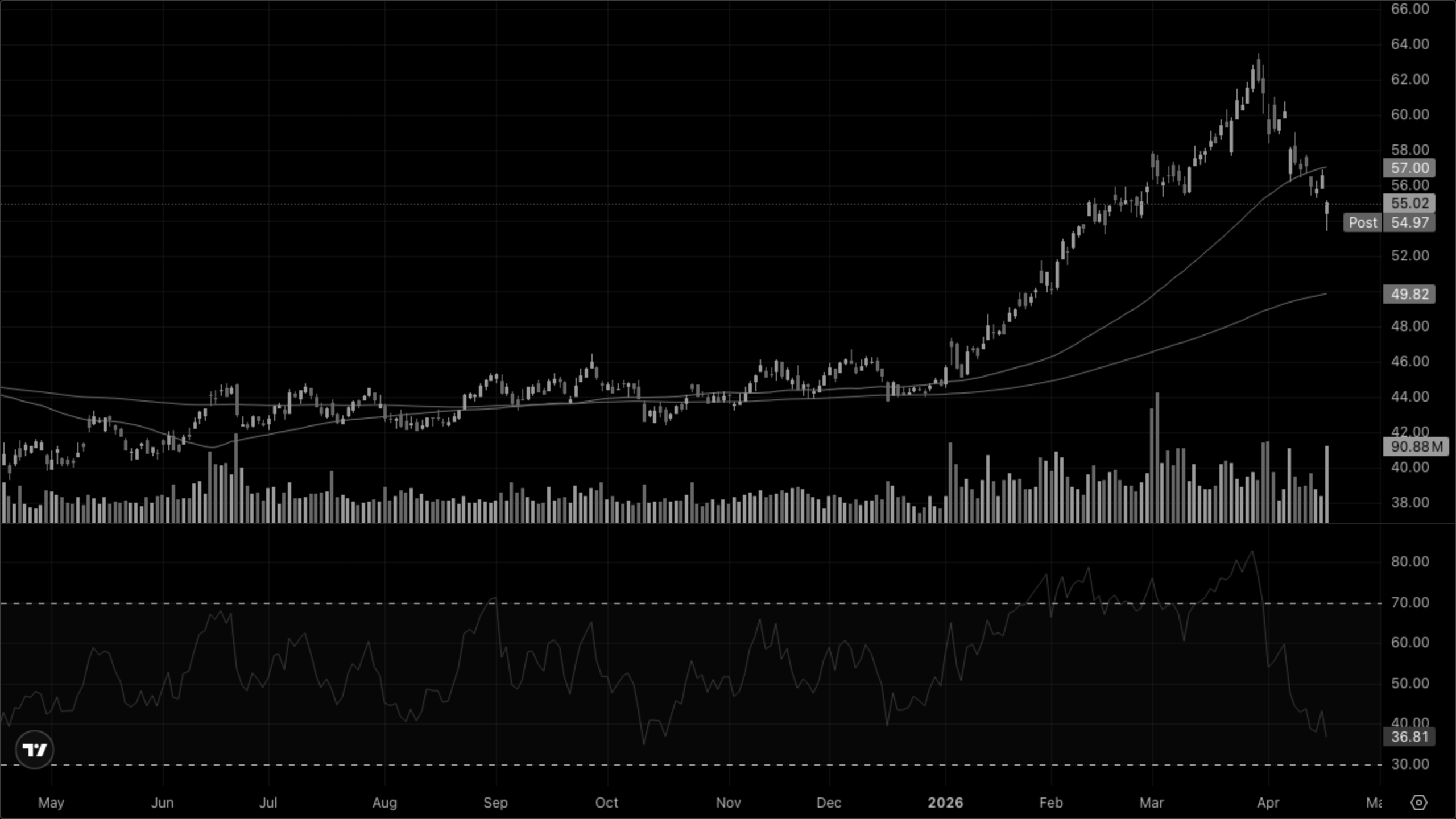

XLE — Energy

XLB — Materials

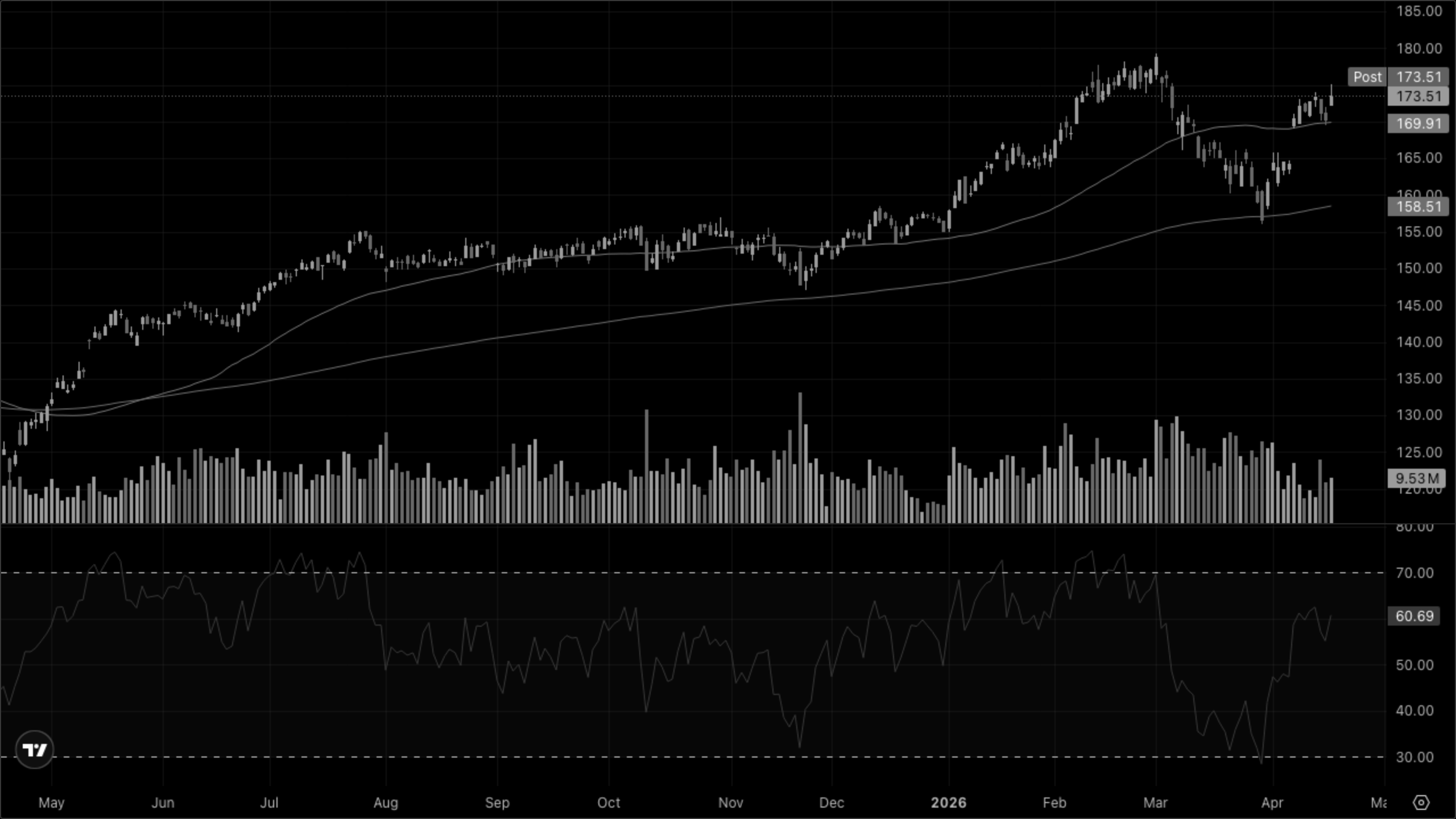

XLI — Industrials

Stagflation — Contraction + Inflation

Defensives that hold up when growth stalls but prices stay hot

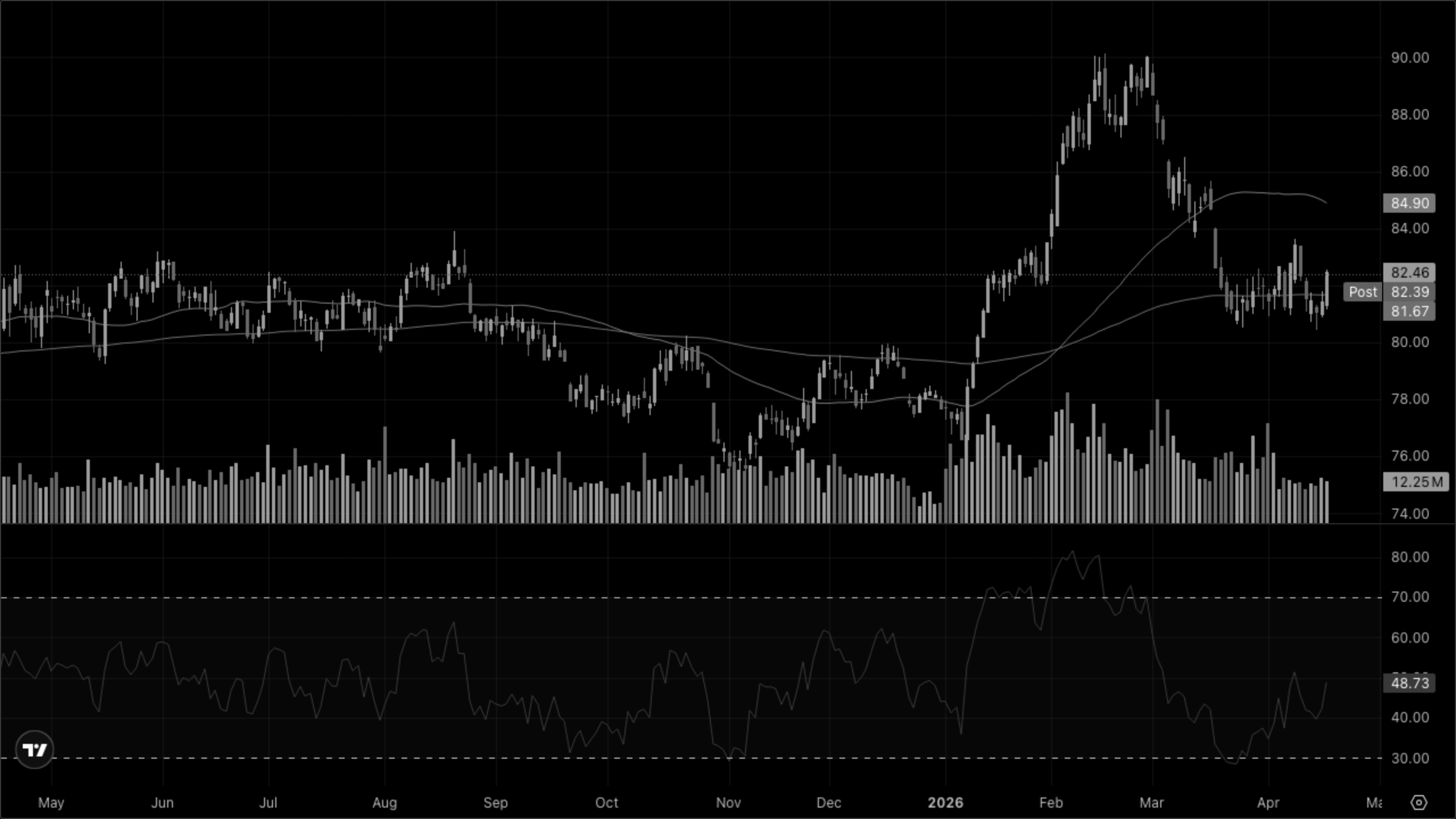

XLP — Staples

XLV — Health Care

XLU — Utilities

Deflation — Contraction + Disinflation

Rate-sensitive sectors that benefit from falling yields

XLRE — Real Estate

XLF — Financials

Leadership is concentrated in the Goldilocks quadrant — XLY +2.36%, XLK +1.53%, XLC +0.23% — while Reflation is split: XLI +1.87% and XLB +0.25% rallying on growth, but XLE -2.76% hammered by the oil break. Stagflation defensives are mixed (XLP, XLV green but lagging; XLU red), and rate-sensitives XLRE +1.53% benefit from the lower-yield backdrop. Net read: growth strong, inflation impulse weakening — the Goldilocks call is getting confirmation from both leadership and the Reflation/Stagflation fades.

Cross-Asset Narrative

Rates & Curve

Yields down across the stack: 2Y -7bp (3.71%), 5Y -7bp (3.85%), 10Y -7bp (4.25%), 30Y -5bp (4.88%). Parallel shift with slight bull-steepening at the long end. 2s10s holds +54bp. Oil's collapse is pulling breakeven expectations lower and giving Treasuries a bid alongside the equity rip — unusual combo that screams "inflation scare unwind" rather than growth fear.

Inflation Pulse

WTI -9.86% is the dominant signal — biggest disinflation shock in months. Silver +3.09% and copper +0.63% complicate the picture; real-asset bid persists even as the energy component breaks. Watch 5Y breakevens tomorrow.

Risk Appetite

VIXY -1.27% to 27.93, DXY flat at 98.23. Classic risk-on profile without dollar stress. No flight-to-safety signature anywhere in the complex.

Equity Regime

Dow leading (+1.79%) over Nasdaq (+1.29%) is a subtle tell — cyclicals and broader participation rather than mega-cap-only. XLY's +2.36% confirms a consumer/risk-on rotation, not just an AI bid.

Global

USD/JPY -0.33% to 158.59, EUR/USD and USD/CNY effectively flat. Yen strength is notable given the risk-on tape — likely BoJ/positioning, not risk-off.

The weight of evidence points to Goldilocks — Growth + Disinflation.