Market news

Today marks one year since "Liberation Day" tariffs. The Trump administration announced new tariff changes in the final minutes of trading: 100% tariffs on pharmaceutical imports unless drugmakers cut prices or produce domestically, while steel, aluminum, and copper derivative tariffs were reduced to 25%. More than a dozen major drug companies including Eli Lilly, Pfizer, and Johnson & Johnson have already signed exemption deals. Meanwhile, Iran's reported cooperation with Oman on a Strait of Hormuz shipping protocol provided the catalyst for the afternoon reversal, offering the first tangible de-escalation signal since the conflict began.

Sector quadrants

Goldilocks — Growth + Disinflation

Risk-on leaders when growth is strong and inflation fades

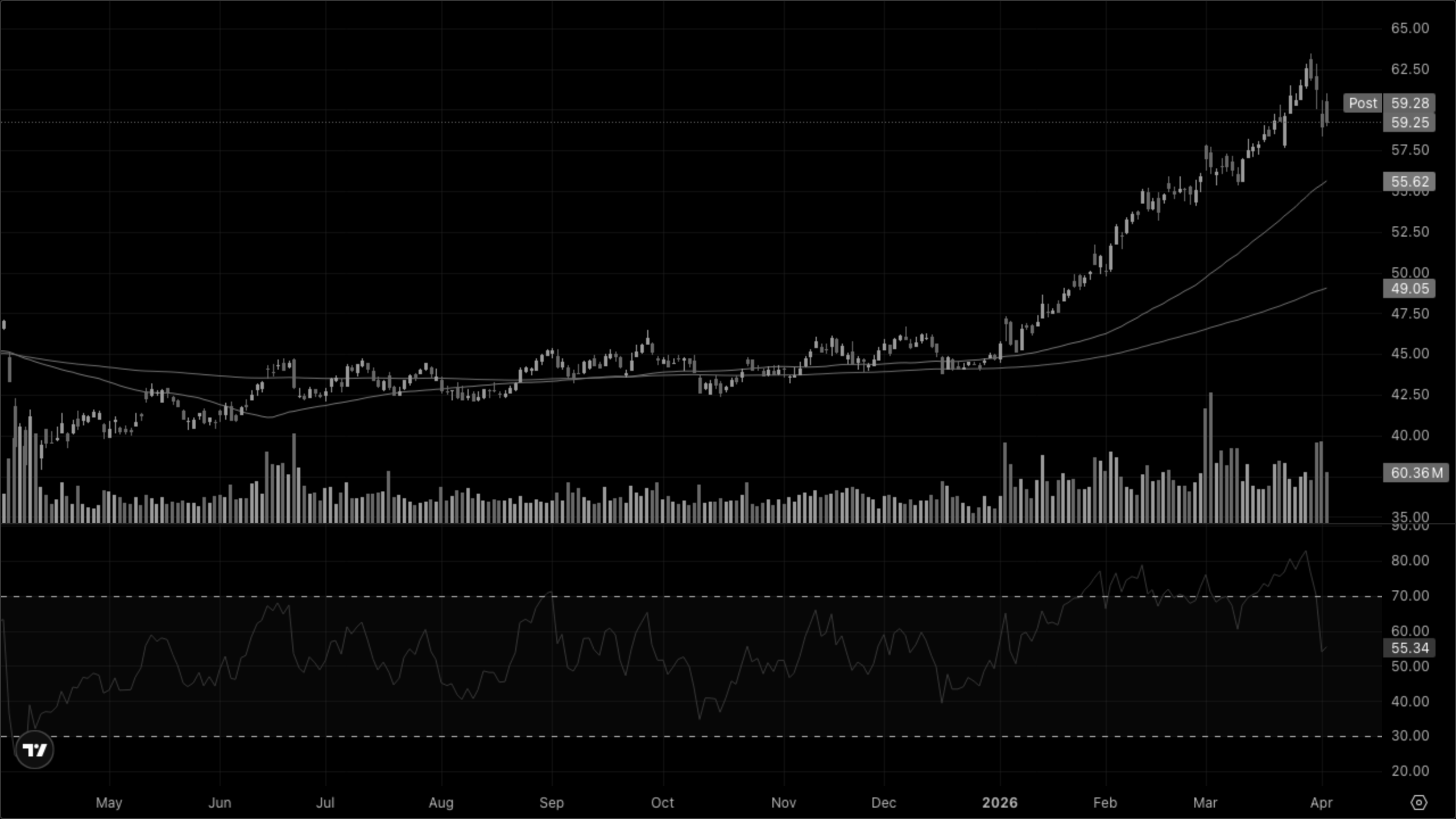

XLK — Technology

XLY — Discretionary

XLC — Comms

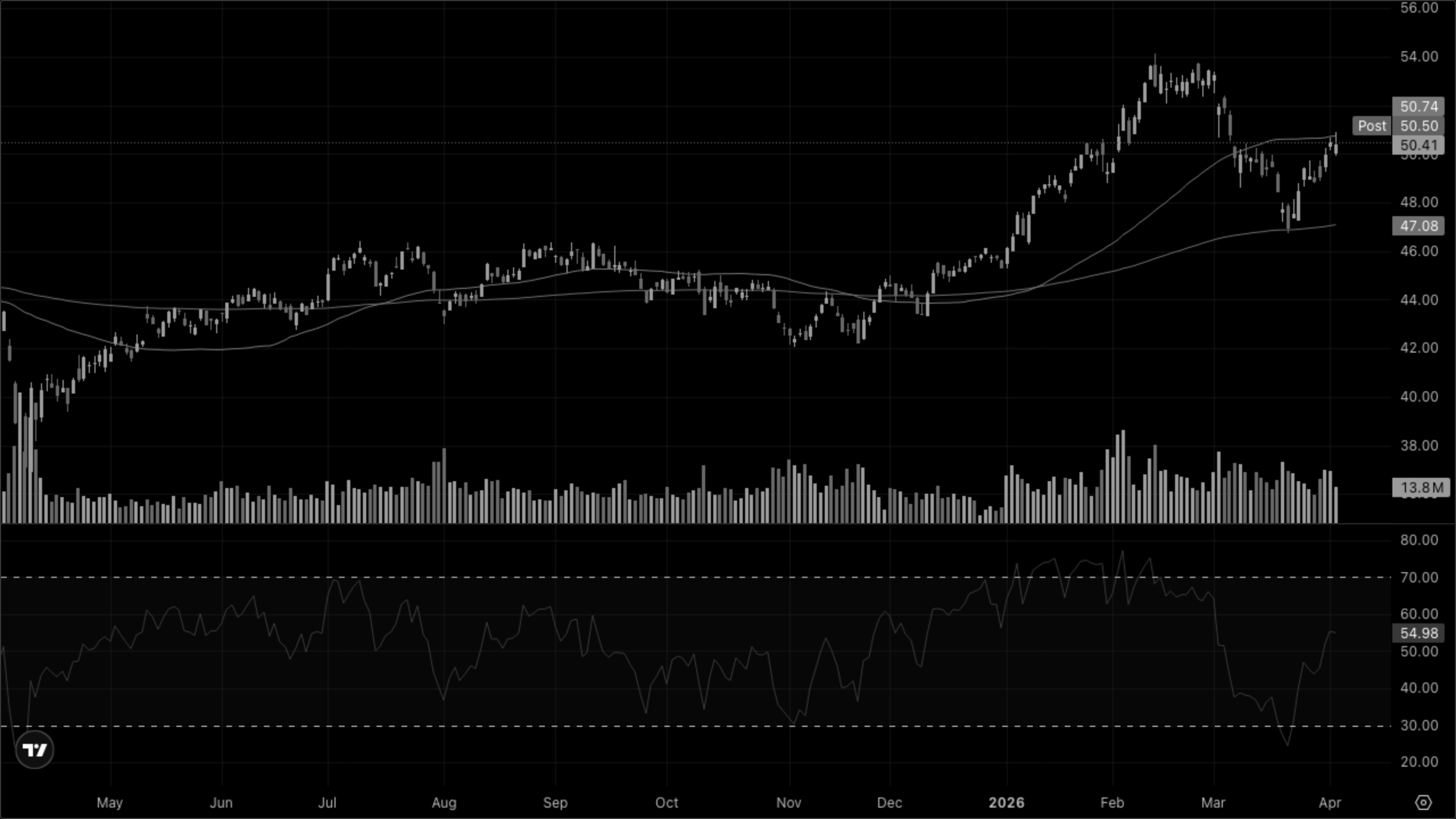

Reflation — Growth + Inflation

Cyclicals that benefit from rising prices and activity

XLE — Energy

XLB — Materials

XLI — Industrials

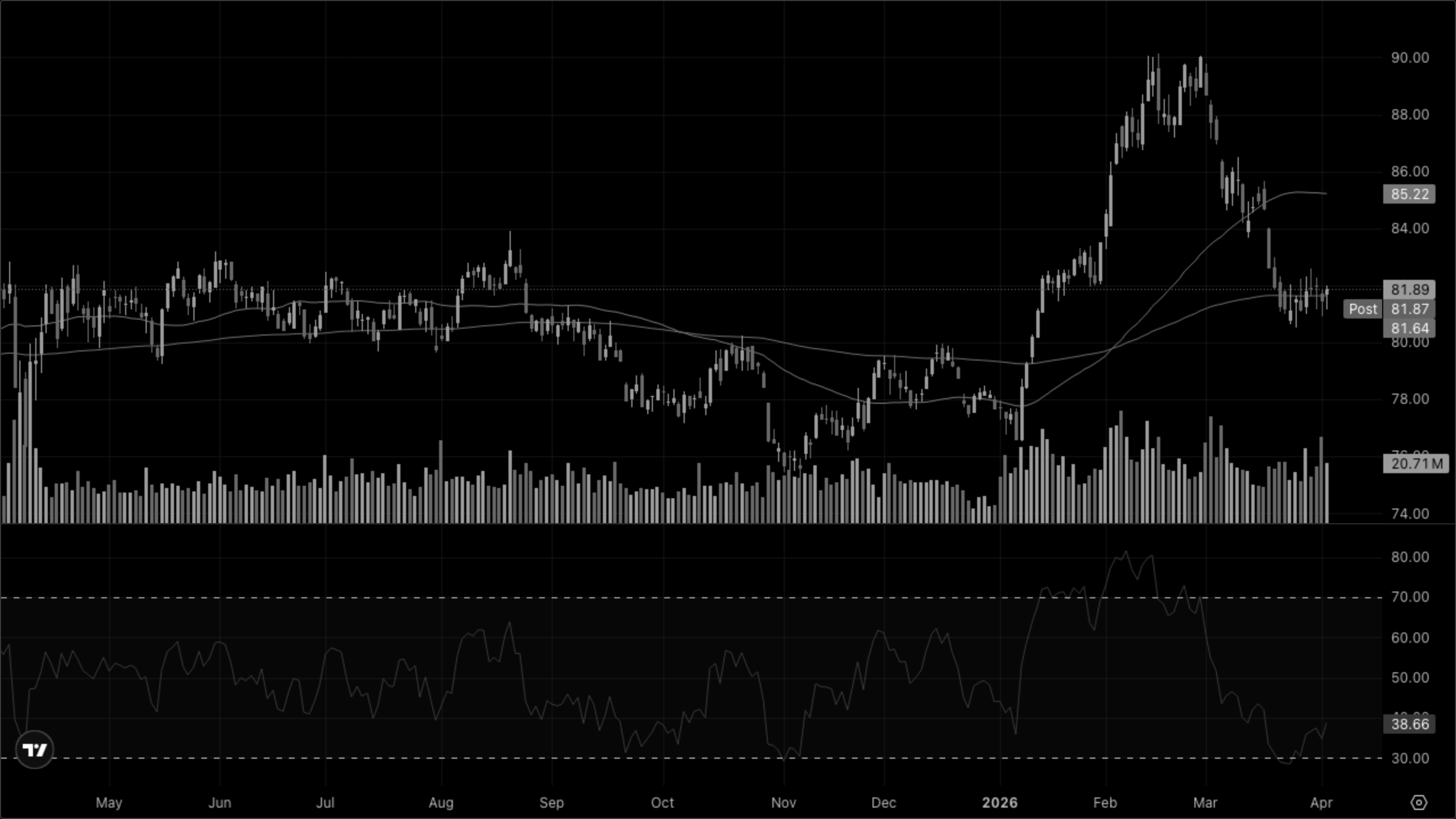

Stagflation — Contraction + Inflation

Defensives that hold up when growth stalls but prices stay hot

XLP — Staples

XLV — Health Care

XLU — Utilities

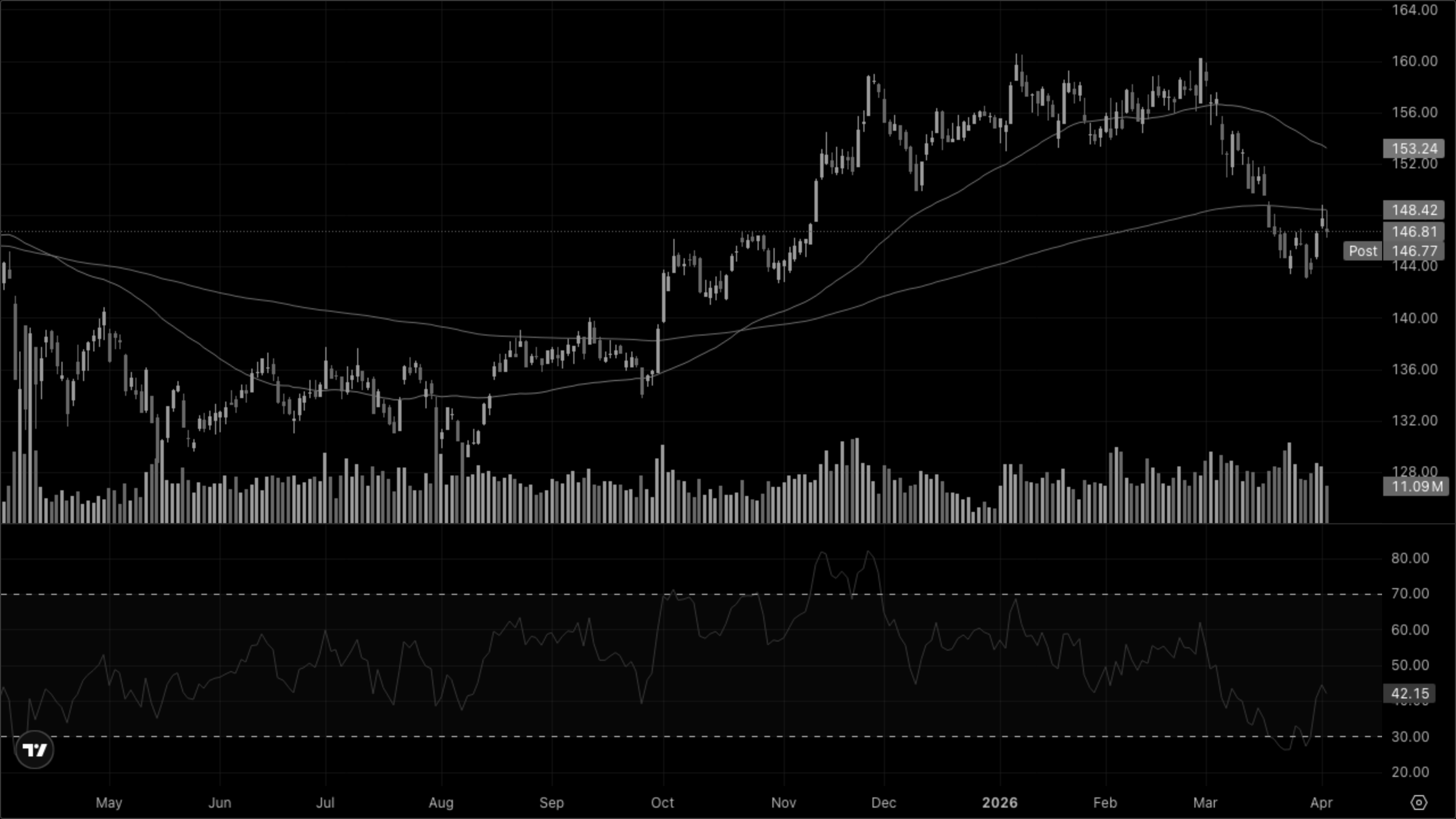

Deflation — Contraction + Disinflation

Rate-sensitive sectors that benefit from falling yields

XLRE — Real Estate

XLF — Financials

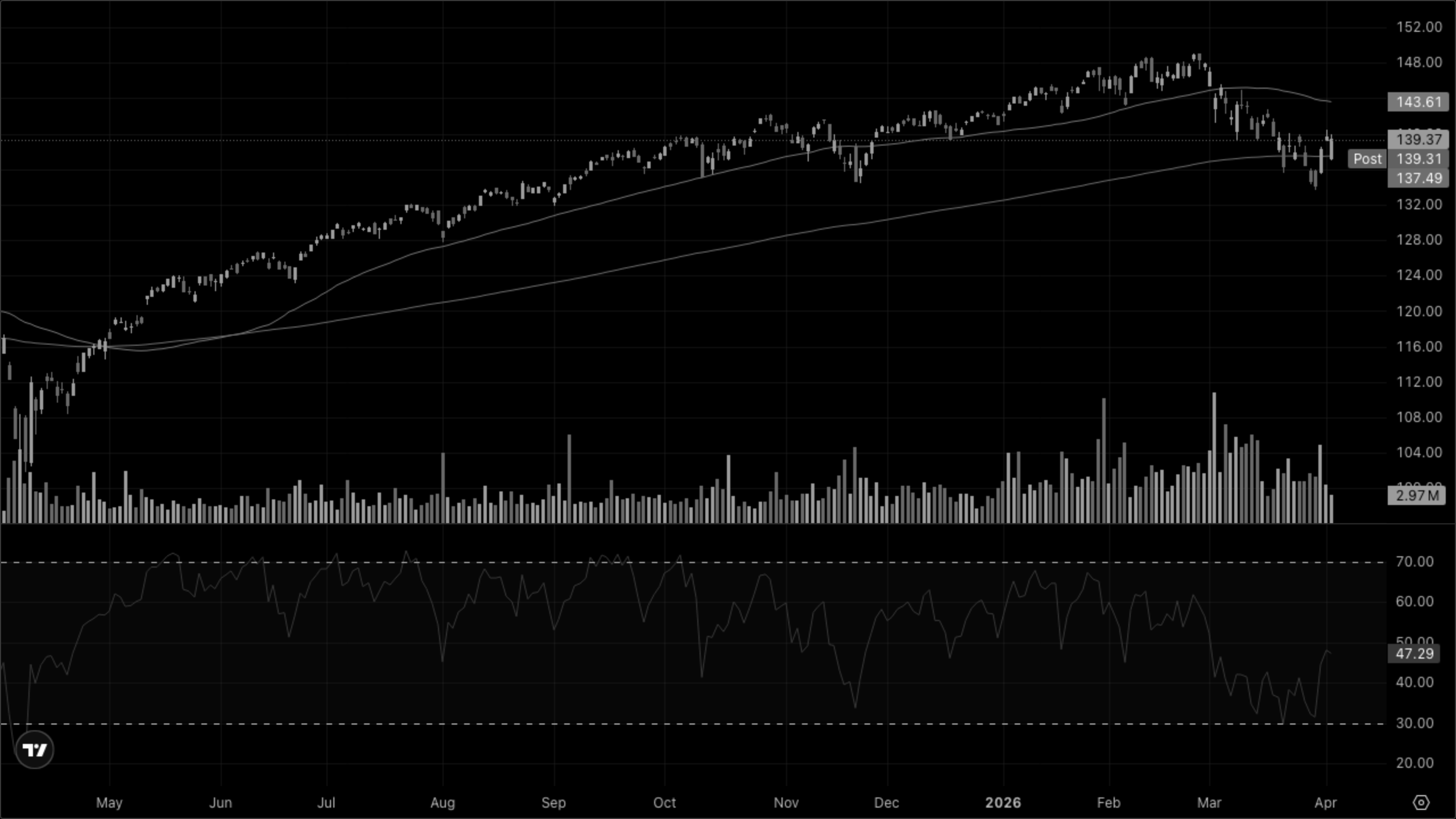

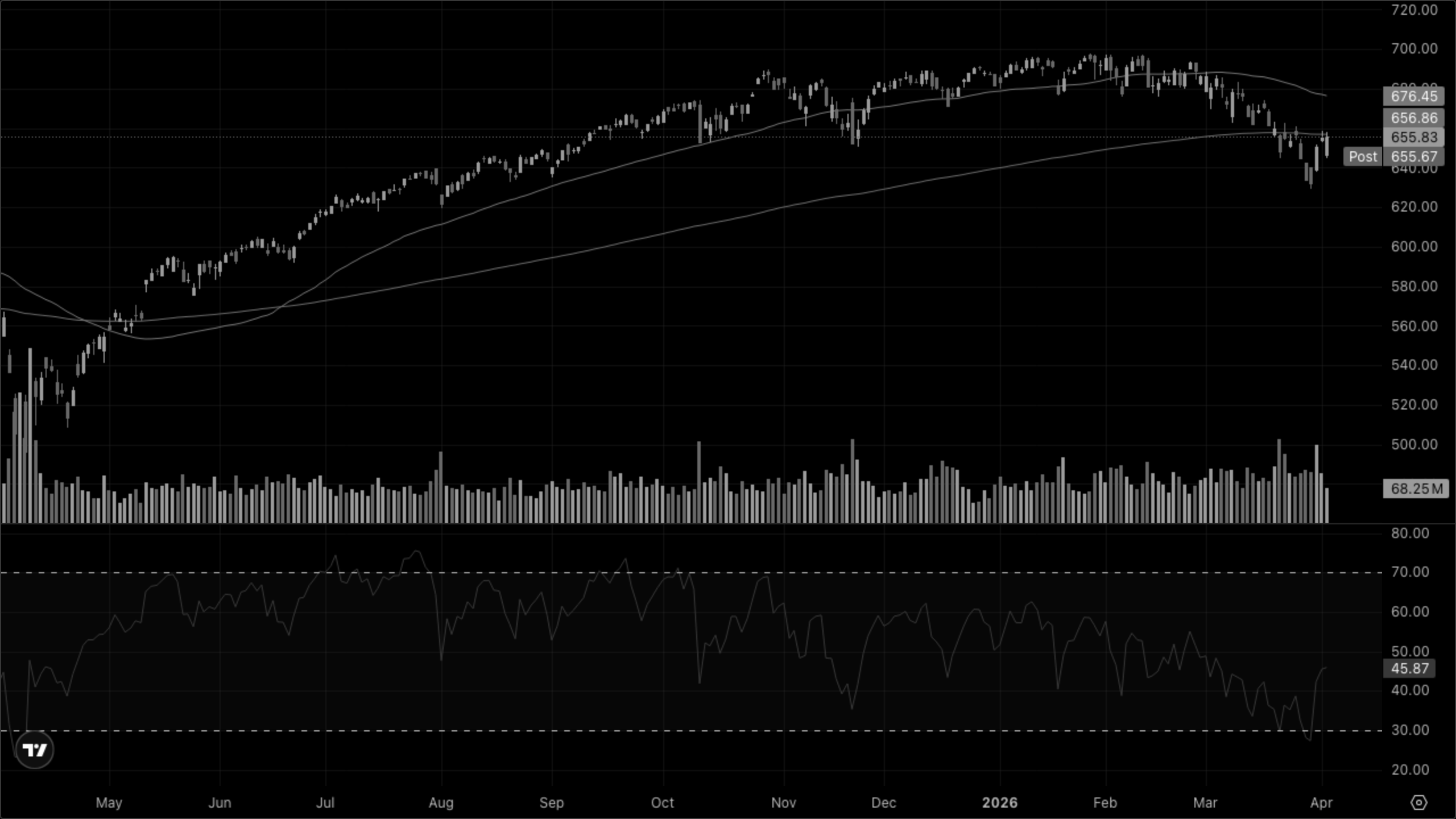

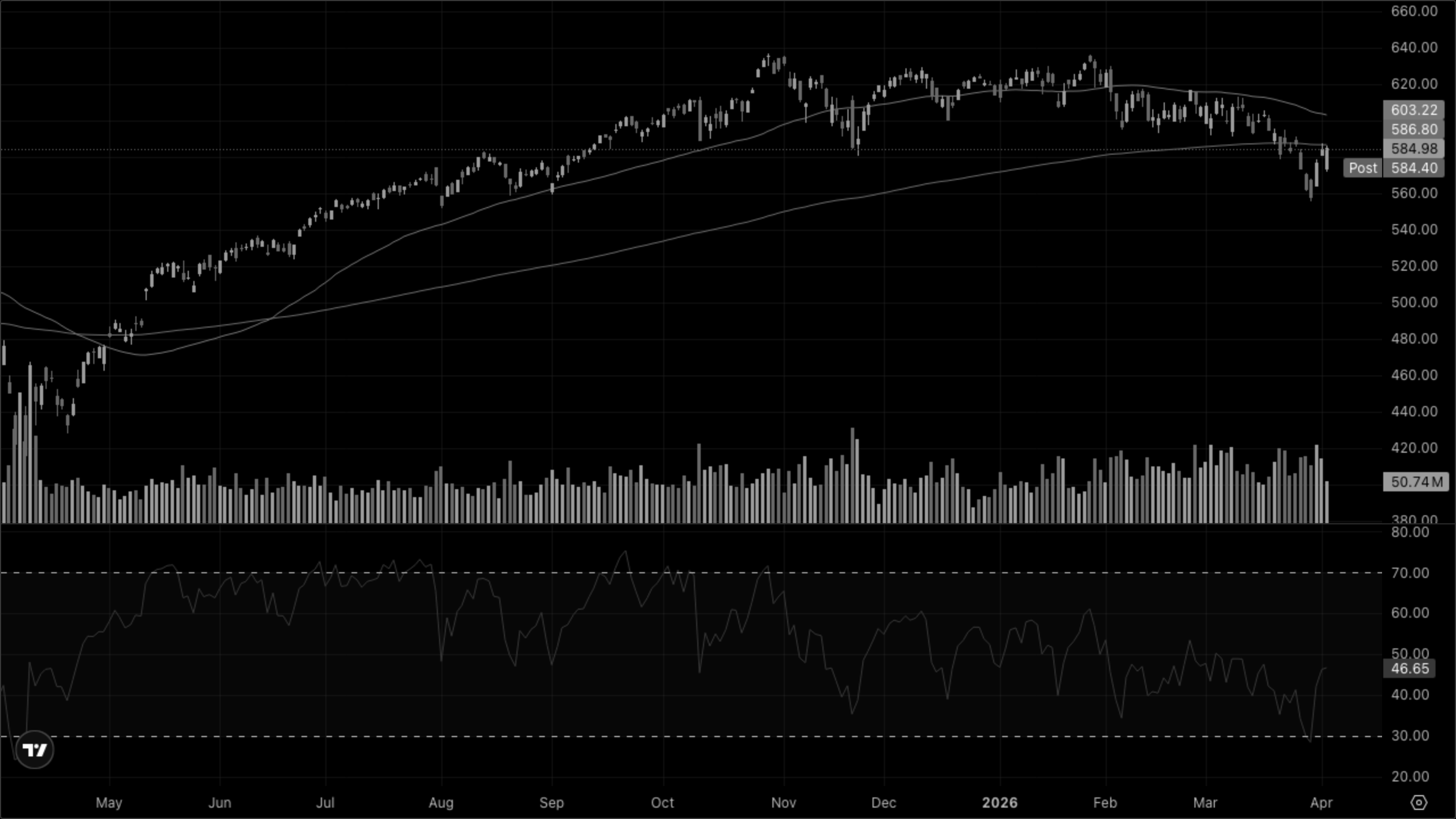

Today's sector leadership tells a mixed story. The Deflation quadrant's XLRE (+1.61%) is the day's clear winner, benefiting from falling yields — a signal the market is pricing potential rate relief if de-escalation materializes. Reflation's XLE (+0.47%) remains bid on still-elevated oil, while XLB and XLI are weak. The Goldilocks quadrant is split: XLK bounced +0.80% but XLY at -1.50% is the worst sector, confirming consumer stress. Stagflation sectors (XLP, XLV) are not leading today — a departure from the last two weeks. The rotation toward rate-sensitive sectors over defensives is the first hint that the market may be looking past the inflation shock, but one session doesn't make a trend.

Cross-asset narrative

Rates & curve

Yields fell across the curve: 5Y at 3.95 (-0.20%), 30Y at 4.88 (-0.49%). The long end leading the decline is notable — it suggests the term premium related to the energy shock is starting to compress on Hormuz de-escalation hopes. The IMF flagged today that the Fed has "little scope" for rate cuts this year, and markets are still pricing the possibility of a hike if oil stays elevated. The April 29 FOMC meeting is the next decision point.

Inflation pulse

Gold's sharp pullback (~2.78% to ~4,679) is the day's most interesting signal. If de-escalation is real, gold's safe-haven bid unwinds. But WTI remains above $105, which means the actual inflation pass-through hasn't changed — only the expectation of future supply normalization. Copper weak at 5.58 (-1.12%), keeping the copper/gold ratio depressed and growth-negative.

Risk appetite

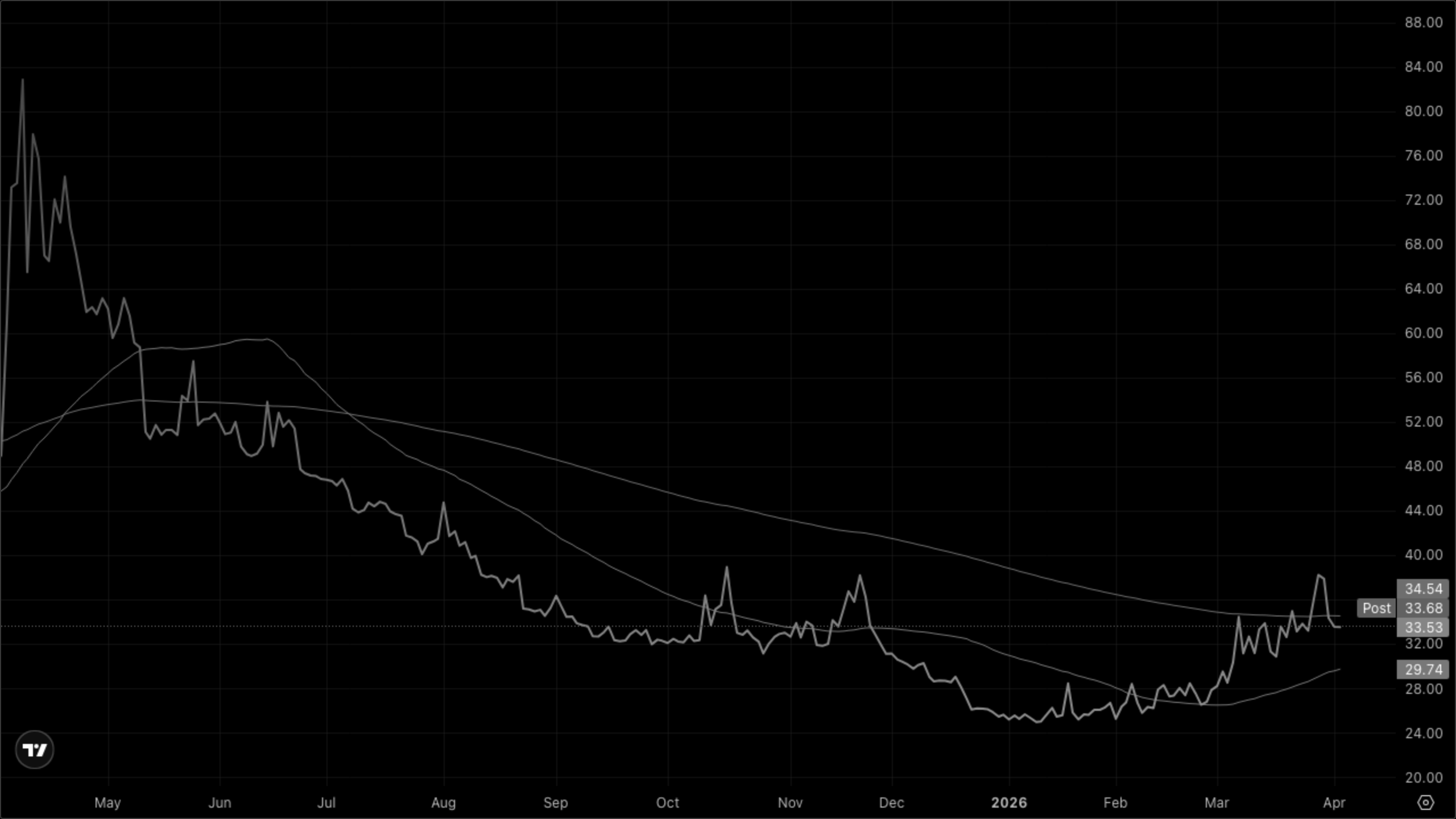

The intraday reversal from -1.5% to +0.11% on the S&P is a powerful breadth signal. VIXY at 33.53 is still elevated (vs. 24.06 in mid-March) but came off session highs of 35.98. The market is desperate for a de-escalation catalyst and today's Hormuz headlines provided one.

Equity regime

XLY at -1.50% vs. XLRE at +1.61% is the widest single-day sector spread in weeks. Consumer discretionary weakness with real estate strength is a classic late-cycle rotation toward rate sensitivity. XLK's bounce (+0.80%) was led by mega-cap names holding up better than the broad market.

The weight of evidence still points to Stagflation, but today's action — gold selling off, yields falling, XLRE leading — introduces a potential transition toward Deflation/rate-relief if the Hormuz de-escalation holds.